The Dividend Yield Illusion: Why SCHD's 3% Distribution Doesn't Explai

Dividend yield gap: SCHD 3.09% vs VIG 1.46% — a 2× spread favors income-focused investors on paperTotal return reversal: VIG +68....

Dividend yield gap: SCHD 3.09% vs VIG 1.46% — a 2× spread favors income-focused investors on paperTotal return reversal: VIG +68....

QQQ 1-year return: +27.6% (no leverage, 0.42% dividend yield)QQQM equivalent return: +27.7% (low-cost tracking at $297.70)Leverage decay impact: Loses 0.5–2% daily during high-volatility periods, compounding to 20%+ underperformance over 3-year drawdown cycles52-week position: QQQ at 86....

JEPI quarterly dividend announcement: $0.3870 (+10.3% year-over-year increase)Current dividend yield: 8.08% (elevated) vs. 1-year total return: +7.4% (weak)5-year cumulative return +42....

JEPI quarterly dividend announcement: $0.3870 (YoY +10.3% increase)Current dividend yield: 8.08% (elevated) vs 1-year total return: +7.4% (weak)5-year cumulative return +42....

JEPI quarterly dividend raised to $0.3870 (up 10.3% year-over-year)Current dividend yield: 8.08% (elevated) vs 1-year total return: +7.4% (weak)5-year cumulative return: +42....

Quarterly Dividend: $0.6370 announced, up 25.1% year-over-year Dividend Yield: 9.95% vs JEPI 8.08% (JEPI shows superior dividend stability) 1-Year Total Return: JEPQ +19....

GLD returned +123.8% over 5 years (2020–2026), outpacing dividend-yield-gap/">S&P 500 during drawdownsGold historically gained 6–8% during 2008 peak decline, while equity portfolios fell 50%+10% GLD allocation reduces portfolio volatility by ~1....

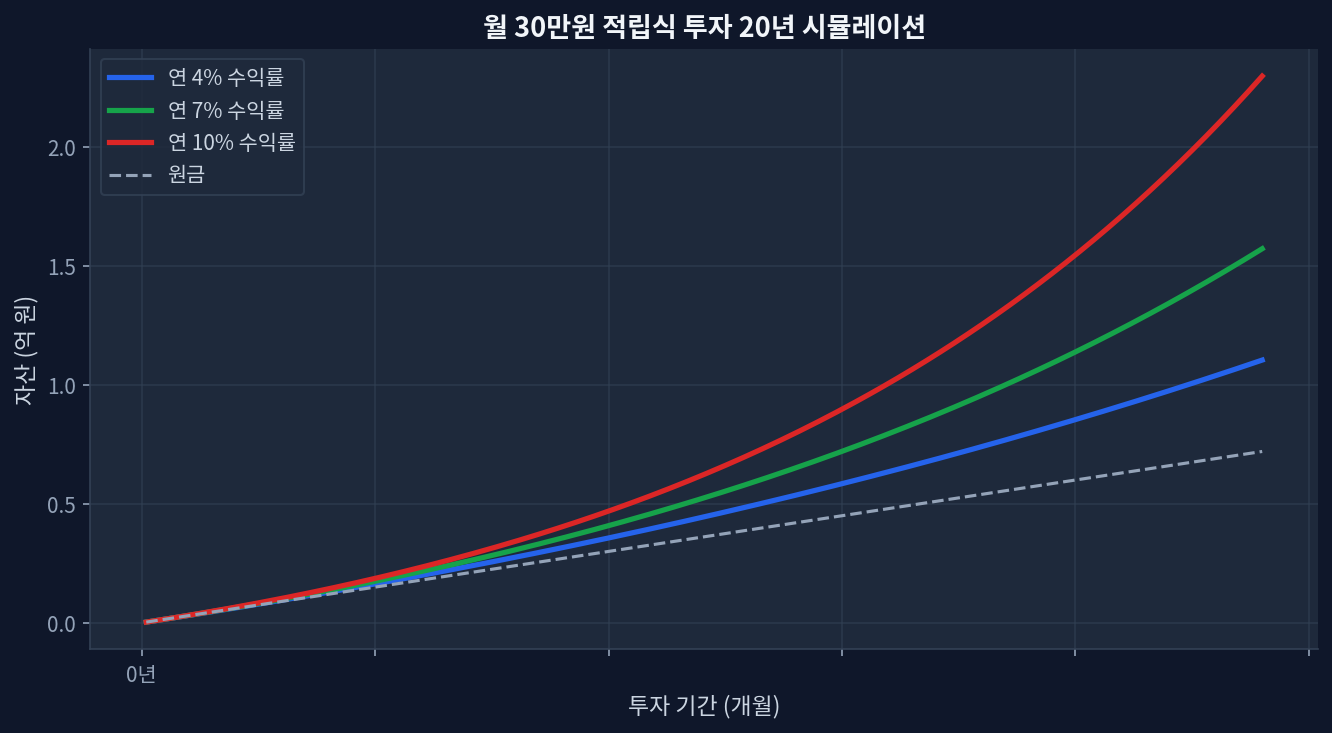

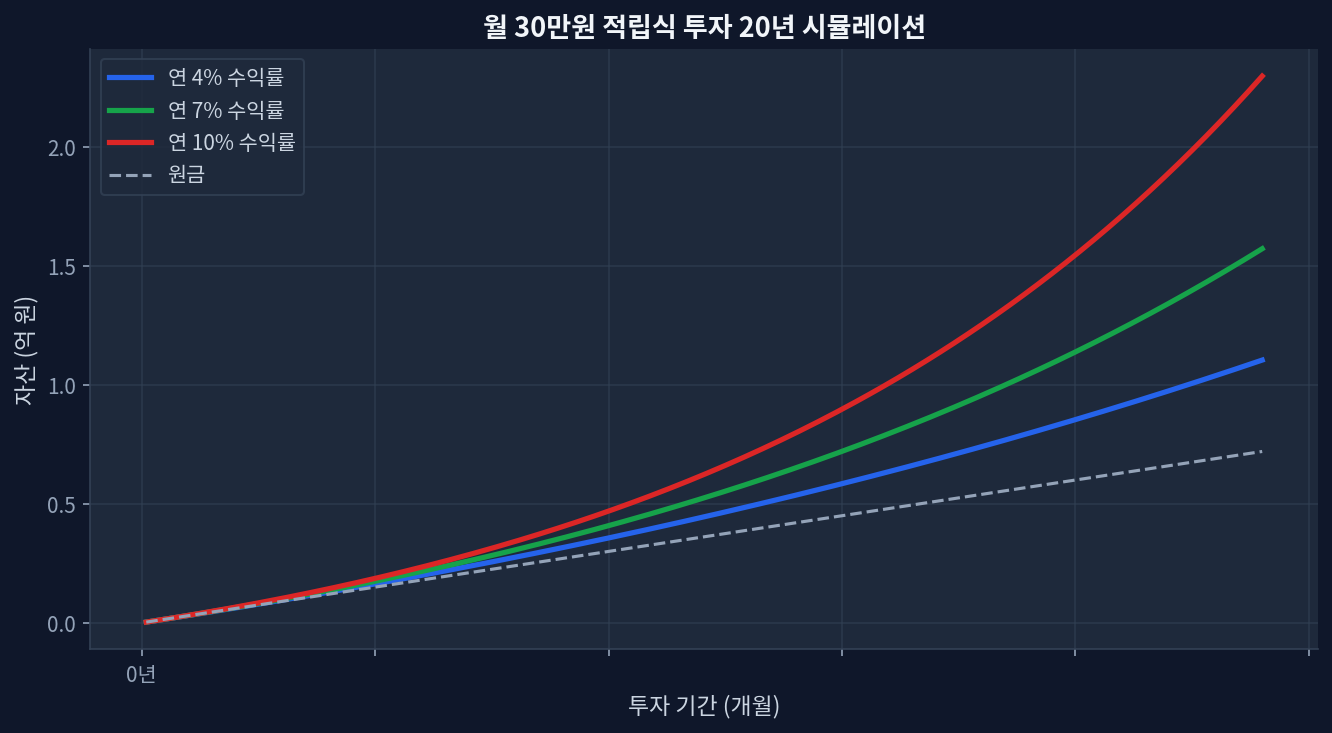

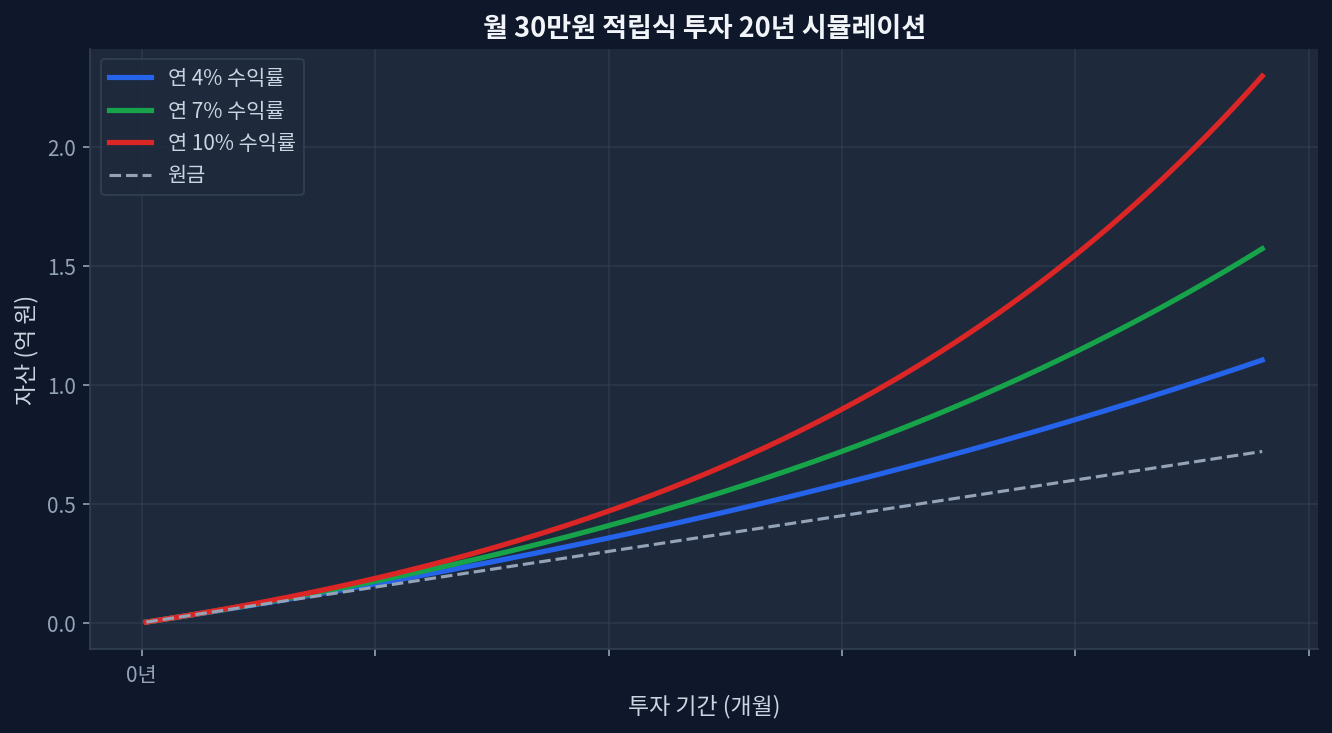

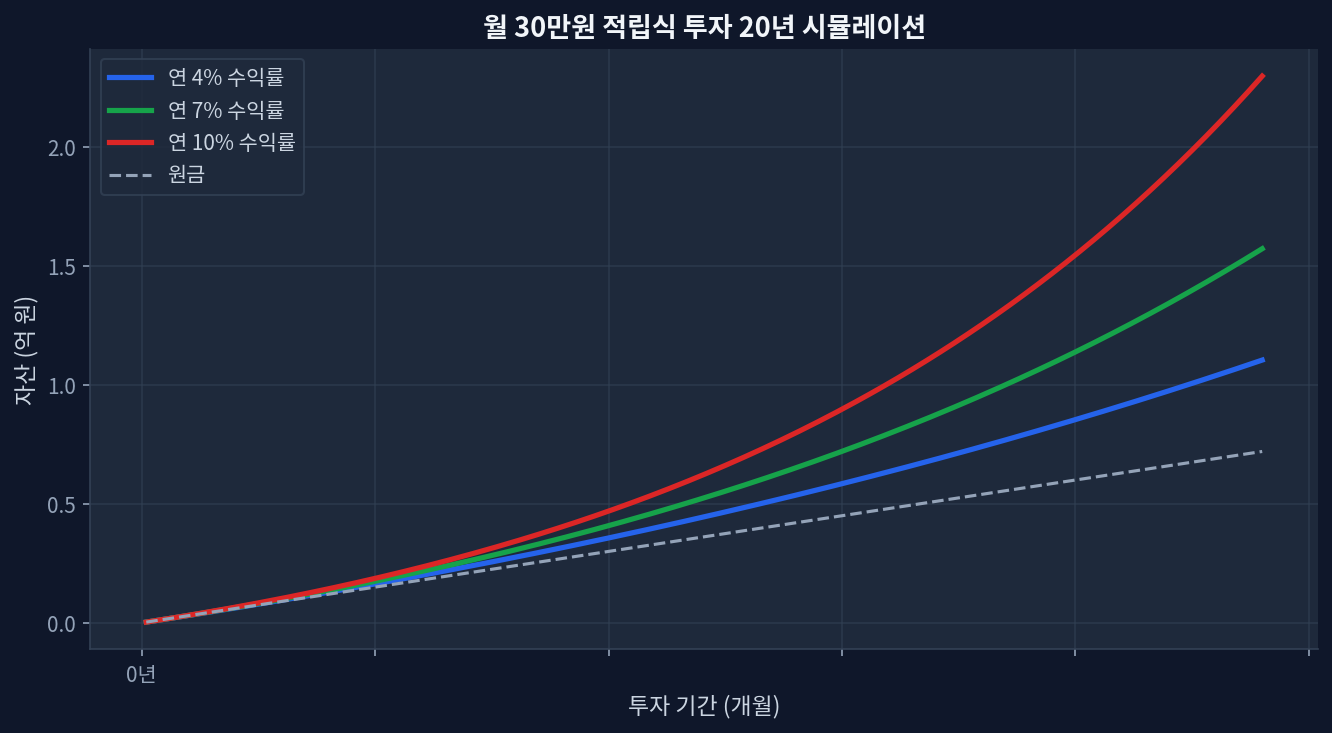

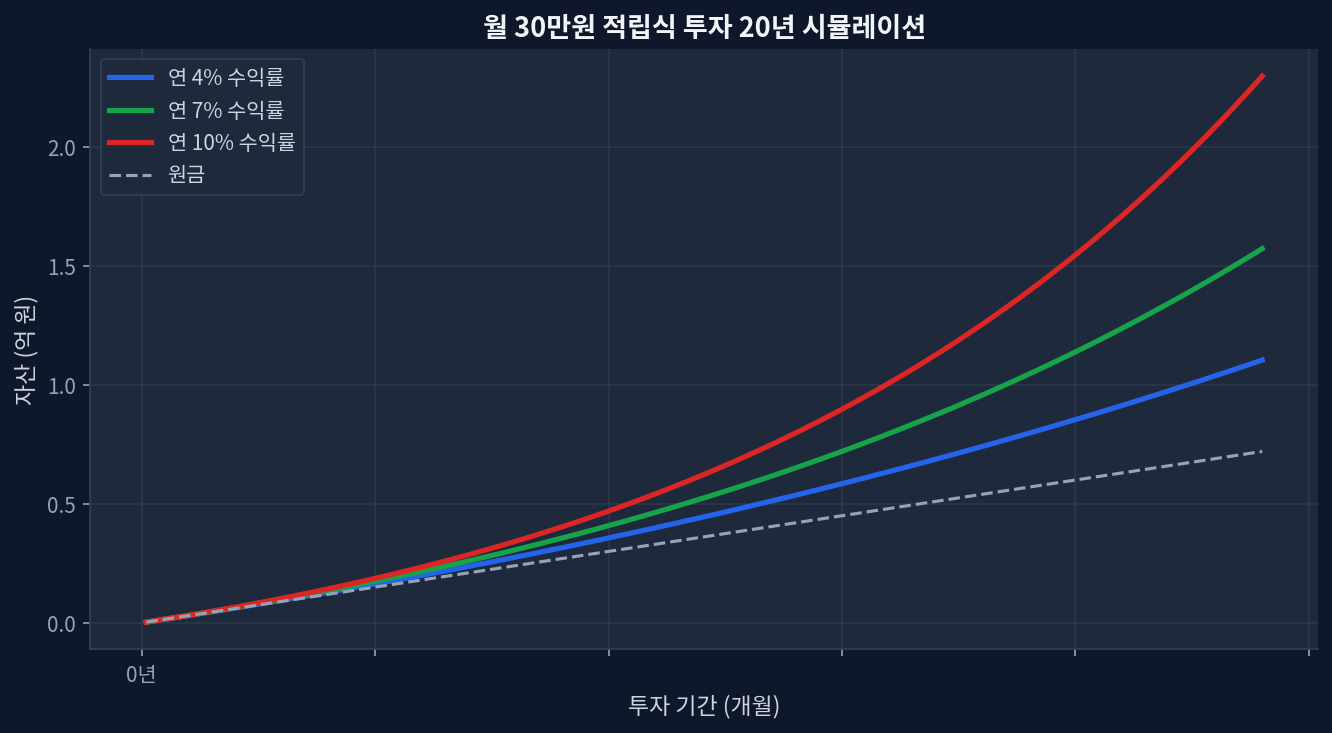

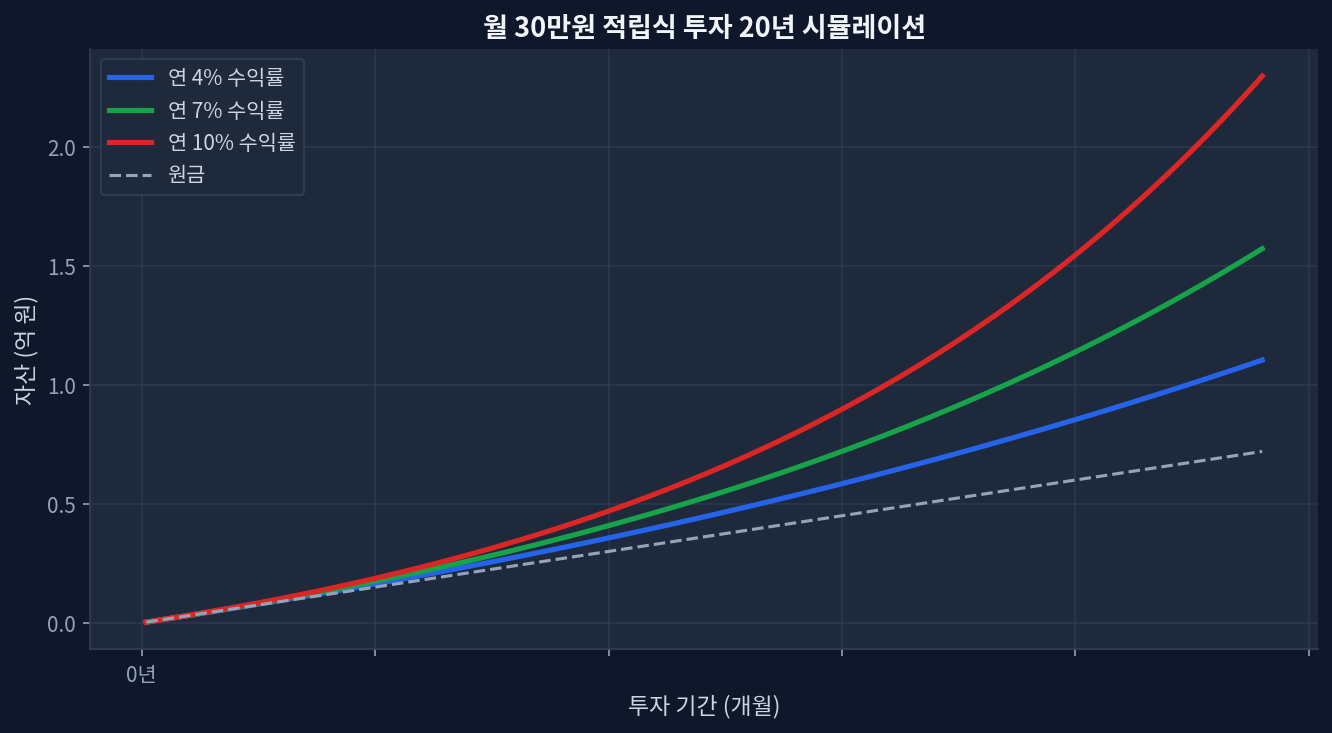

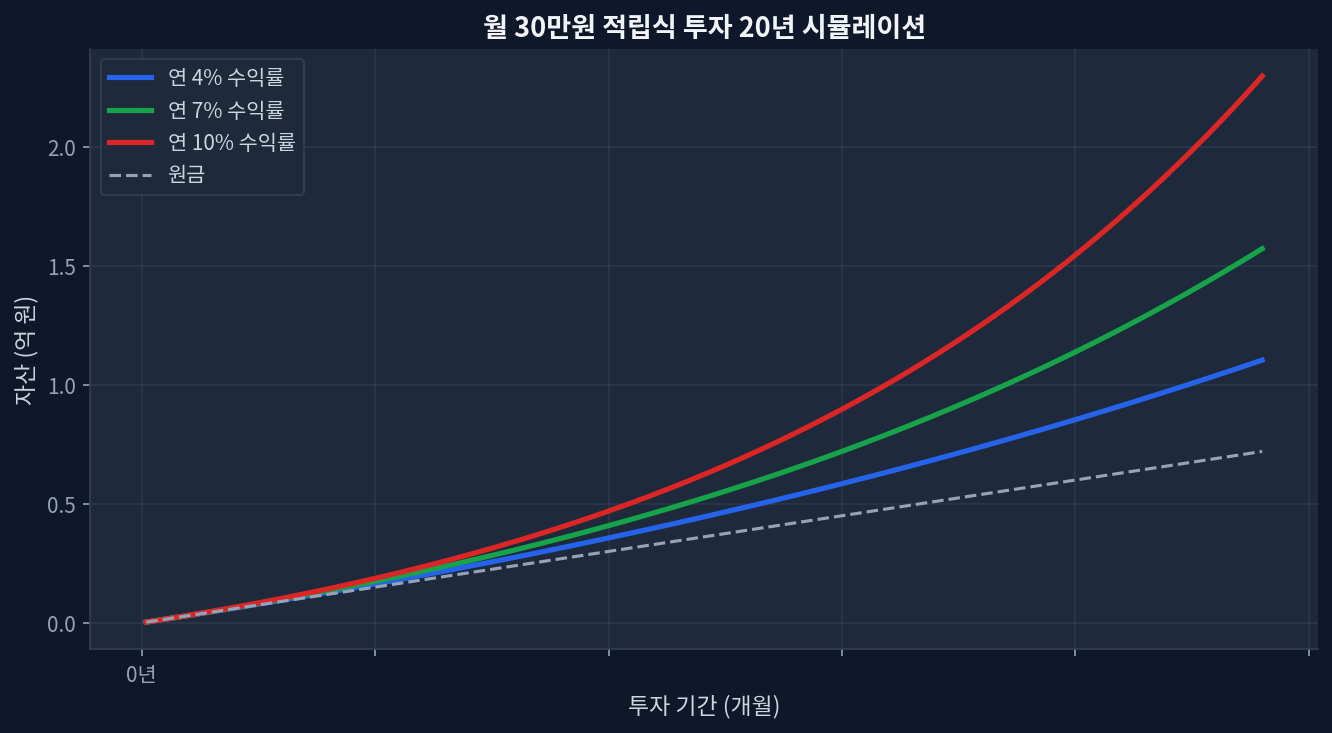

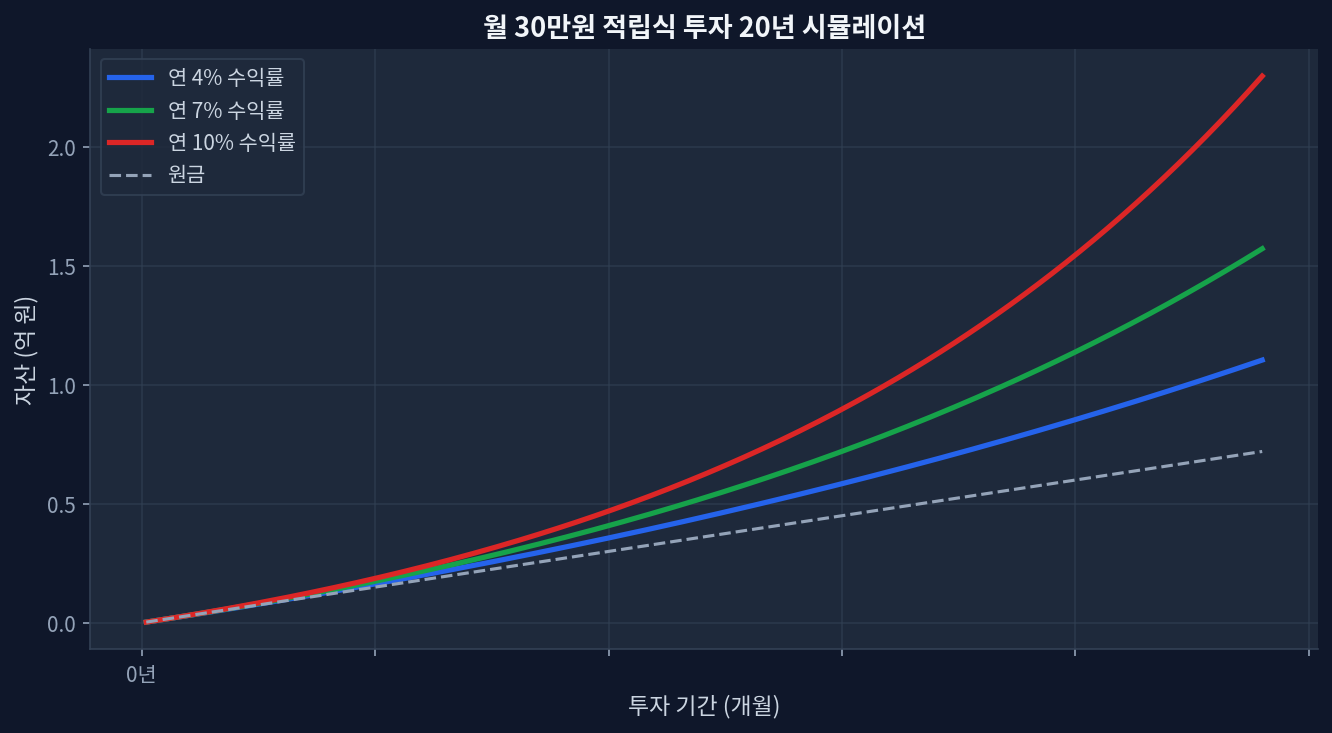

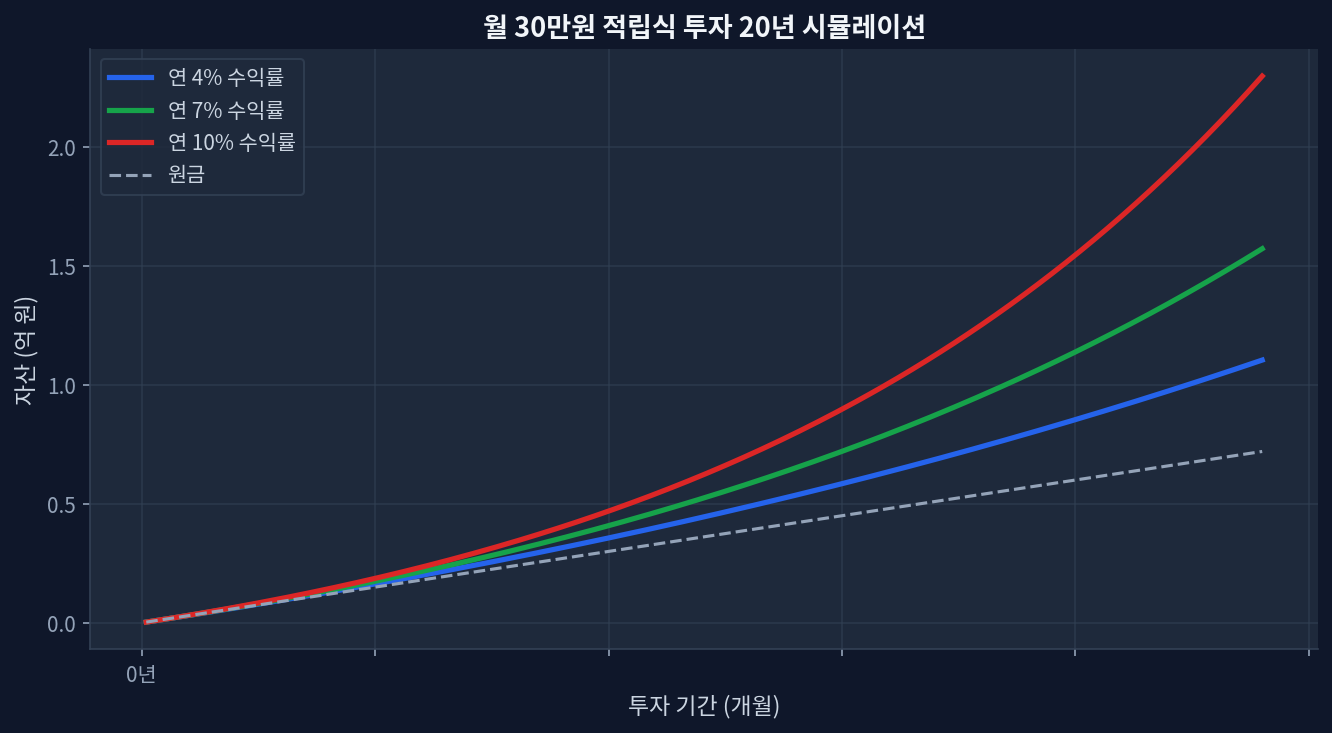

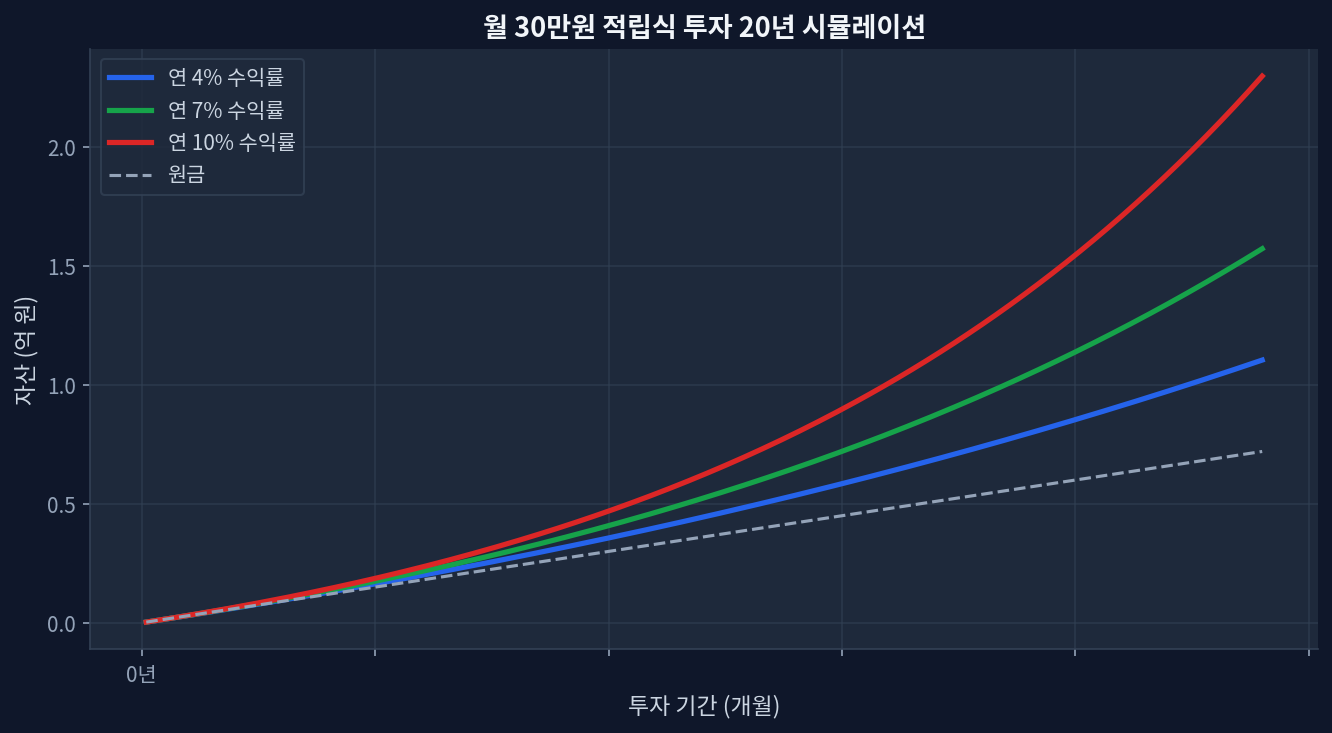

SCHD Quarterly Dividend Cut to 3.25% Yield: Strategic Management of Expectations Monthly $30K investment 20-year compound growth simulation SCHD quarterly dividend: $0....

SCHD (dividend-focused ETF): 3.25% yield, +26.5% 1Y return, $31.96 current price as of late June 2026VIG (dividend growth): 1.47% yield but +71....

Key PointsOptimal emergency fund threshold: 4-6 months of living expenses relative to total assets ($2,200-$3,300/month spending baseline equals $8,800-$19,800 reserve)2008 financial crisis data: investors holding less than 3 months emergency reserves showed +45% higher forced-selling probability (Morningstar 2000-2023 tracking)Return variance comparison: VOO and SCHD monthly allocation strategy ($500/month over 20 years) showed ±3....