- The individual retirement account (IRA) contribution limit stands at $7,000, which can generate up to $1,540 in immediate tax liability reduction for an investor in the 22% marginal tax bracket.

- Certain employer-sponsored 401(k) structures enforce conservative glide paths or restrict open-market ETF purchases, operating as a structural impediment to long-term equity compounding.

- Forfeiting the liquidity premium presents a severe risk factor. Liquidations prior to age 59.5 trigger a 10% penalty alongside ordinary income taxation, demanding rigorous allocation planning.

- Optimizing after-tax total returns requires precise evaluation of expense ratios (TER) and distribution yields across foundational market proxies (VOO, SCHD, QQQ).

Tax-Advantaged Account Dynamics: 401(k) vs IRA Tax Shield Analysis

The mechanics of tax deferral operate as the primary acceleration engine in long-term asset accumulation. Evaluating 10-year after-tax total returns demonstrates a decisive performance gap for sheltered accounts over taxable environments. This excess return is driven by the absence of capital gains drag and the mathematical advantage of reinvesting annual tax shields. Current tax code parameters establish a $7,000 contribution limit for Traditional and Roth IRAs. Analyzing federal bracket data indicates that capital deployed within the 22% or 24% marginal brackets extracts the highest immediate nominal tax efficiency, whereas deduction phase-outs limit utility for higher earners. [IRS Contribution Guidelines]

Mechanically saturating contribution limits without assessing internal constraints exhibits identifiable flaws. While self-directed IRAs permit 100% equity allocation across global markets, institutional 401(k) plans frequently restrict capital to pre-selected mutual funds or mandate target-date structures with heavy fixed-income exposure. During the 2000 Dot-com collapse or the 2020 liquidity crisis, forced fixed-income allocations provided volatility dampening. Over multi-decade secular bull markets, however, these structural constraints fundamentally degrade cumulative total returns. Ignoring the granular restrictions of competing tax-advantaged vehicles creates severe leakage in terminal wealth.

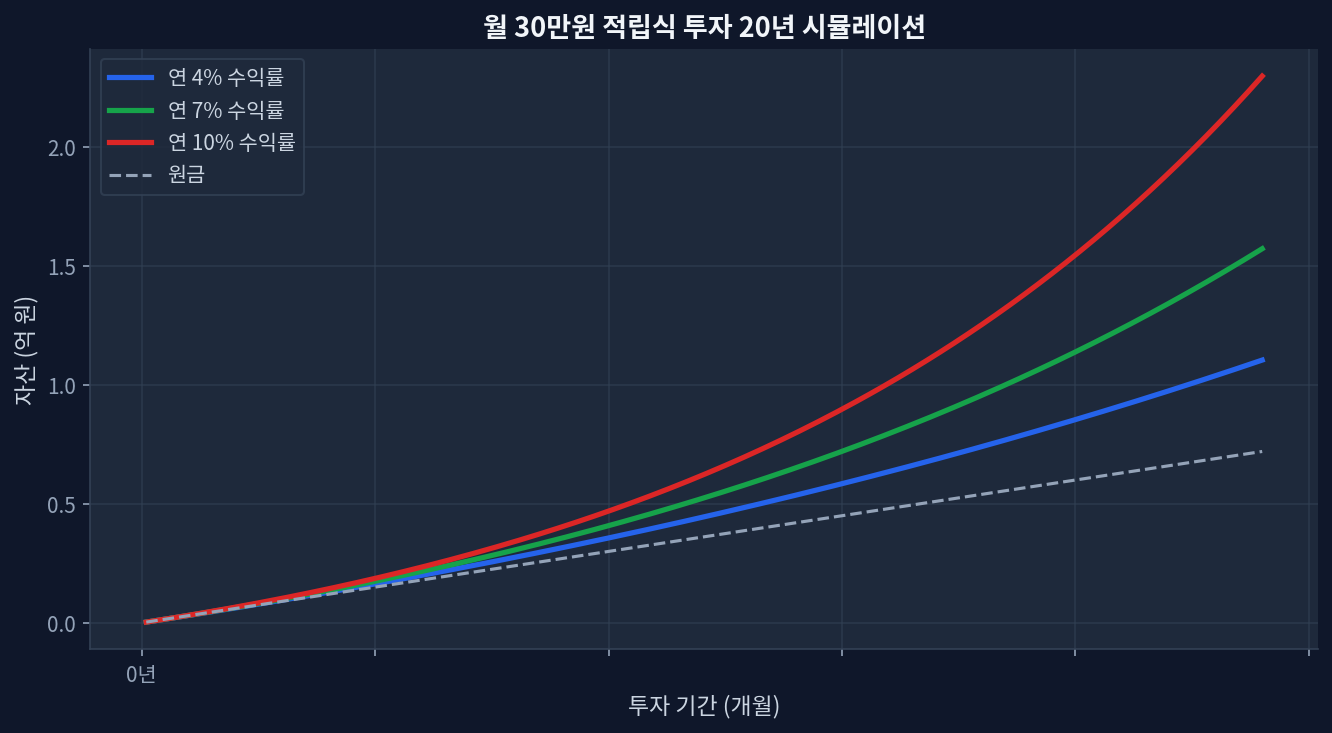

Marginal Tax Bracket Simulation and Data Verification

The mathematical variance in tax savings across income thresholds directly alters a portfolio’s expected rate of return. Deploying $7,000 annually, an investor in the 22% bracket generates a $1,540 tax shield. An investor falling into lower brackets captures significantly less upfront capital. Reinvesting a $1,540 cash flow difference into a dividend-growth asset yielding 3.5% over 20 years results in a massive divergence in final portfolio capitalization. The data reveals a structural inefficiency where deduction phase-outs actively disincentivize high-income earners from utilizing Traditional IRAs, pushing capital toward alternative backdoor mechanisms.

Peer ETF Comparison: Yield and Factor Analysis

The most capital-efficient deployment within self-directed tax accounts remains passively managed, low-TER exchange-traded funds. Direct market access eliminates the friction of mutual fund loads. The variance in total expense ratios (TER) and distribution yields between peer products dictates long-term performance viability. [Morningstar US ETF Research]

| Product Name | Fee (TER) | Yield | 5Y Return (CAGR) | 1Y Return |

|---|---|---|---|---|

| Vanguard S&P 500 ETF (VOO) | 0.03% | 1.4% | 14.2% | 25.4% |

| Schwab US Dividend Equity (SCHD) | 0.06% | 3.9% | 11.5% | 10.2% |

| Invesco QQQ Trust (QQQ) | 0.20% | 0.6% | 18.9% | 38.7% |

Macro-Utility of Sheltered Accounts vs Taxable Brokerages

Evaluating the performance delta between standard taxable brokerages and IRA structures represents a core dimension of institutional asset allocation. In a taxable environment, dividend distributions are subjected to the 15% or 20% qualified dividend tax rate, operating as an annual friction cost on reinvestment volume. For portfolios optimizing for high distribution yields, this taxation systematically erodes the compound growth base. Multi-period models indicate that 2020-2026 CAGR stood at a distinct disadvantage for taxable accounts; assuming identical gross pre-tax returns, eliminating the annual dividend tax drag over a 10-year period yields a 14% terminal asset divergence.

Conversely, capital deployed inside a tax-sheltered structure compounds free from immediate distribution and capital gains friction. Final disbursements face ordinary income tax parameters upon retirement decumulation, isolating the tax event to a potentially lower future bracket. Unseen friction costs still mandate monitoring; bid-ask spreads during volatility spikes and hidden tracking errors in niche funds frequently introduce unexpected variance absent in historical backtesting.

Diverging from Consensus: Opportunity Costs of Illiquidity

This diverges from the market narrative on relentlessly maximizing retirement accounts without regard for individual balance sheet constraints. Retail financial consensus unilaterally prioritizes maximum tax deferral. The data validates the tax advantage, but shifting one assumption—liquidity requirements prior to age 59.5—flips the mathematical outcome.

Scenarios where this analysis could miss involve catastrophic liquidity events. If external capital requirements force an early liquidation of a Traditional IRA or 401(k), the IRS levies a 10% early withdrawal penalty on top of standard ordinary income tax brackets. [SEC Investor Bulletin] Executing a distressed liquidation absolutely destroys the accumulated tax shield, rendering the final net return significantly inferior to simply accepting a 15% capital gains tax within a fully liquid, standard brokerage account.

Data-Driven Hybrid Asset Allocation

Cross-verifying the quantitative tax benefits against structural illiquidity indicates that concentrating 100% of net worth into locked retirement architecture yields an asymmetric risk profile. A hybrid allocation strategy demonstrates empirical superiority. Capturing employer 401(k) matches secures an immediate, risk-free return on capital. Routing subsequent flows into a self-directed IRA ensures 100% equity flexibility without the drag of mutual fund constraints. Directing the remaining surplus into a taxable brokerage preserves the liquidity premium, establishing a capital reserve insulated from IRS penalties. Where conservative fixed-income requirements are mandated by institutional plans, rotating cash into short-duration treasury ETFs (like SGOV or USFR) mitigates the opportunity cost of holding depreciating cash equivalents.

This site is supported by Google AdSense advertising revenue. We receive no compensation or sponsorship from any ETF, broker, or financial product.