Traditional IRA and 401(k): Analyzing the Structural Risks Behind Tax Limits

- 2026 Contribution Limits: Traditional IRA $7,000, Employer 401(k) $23,000.

- Immediate tax deductions act as guaranteed capital generation but necessitate severe long-term liquidity freezes.

- 401(k) constrained menus or forced fixed-income allocations act as a drag in bull markets but function as portfolio hedges during deep drawdowns.

- An IRA's 100% equity exposure strategy compounded at 14.2% annualized from 2020-2026, but suffered a 31.4% maximum drawdown (MDD) characterized by extreme volatility.

The market often treats Traditional IRAs and 401(k)s solely as tax-minimization instruments. The immediate deduction from top marginal tax brackets provides a mathematically powerful incentive for retail investors. However, this tax efficiency masks structural risks regarding severe illiquidity and asset allocation constraints. This report dissects the empirical long-term performance of these accounts, analyzing volatility risks hidden behind tax incentives. Investors must evaluate structural parameters and capital freeze durations before maximizing contributions to survive prolonged market cycles.

Empirical Long-Term Performance and Liquidity Frictions

Historical index data reflects an impressive +85% cumulative return over the trailing 5-year period for unhedged US equities.

Evaluating retirement accounts purely on gross returns is a flawed methodology. Capital deployed into Traditional IRAs or 401(k)s remains locked until age 59½. Early withdrawals trigger a 10% statutory penalty plus standard income taxes on the entire distributed amount. This punitive tax structure severely limits the ability to mitigate tail risks related to personal liquidity shocks. [IRS Retirement Plan Tax Protocols] Such structural rigidity renders these accounts incapable of absorbing emergency capital demands across the investor lifecycle.

The critical divergence between a Self-Directed IRA (SDIRA) and a standard employer 401(k) lies in the investment spectrum. IRAs permit 100% allocation to equity ETFs, favored by aggressive market participants relying on continuous asset inflation. Conversely, many 401(k) plans restrict capital to Target Date Funds (TDFs) or core menus that mandate a fractional allocation to fixed income or stable value funds. During the post-2020 expansion, a constrained 401(k) portfolio underperformed a 100% equity IRA by approximately 2.5% annualized. However, during the 2022 rate-hike regime, the mandated fixed-income allocation within the 401(k) acted as a primary mechanism compressing the aggregate portfolio maximum drawdown (MDD).

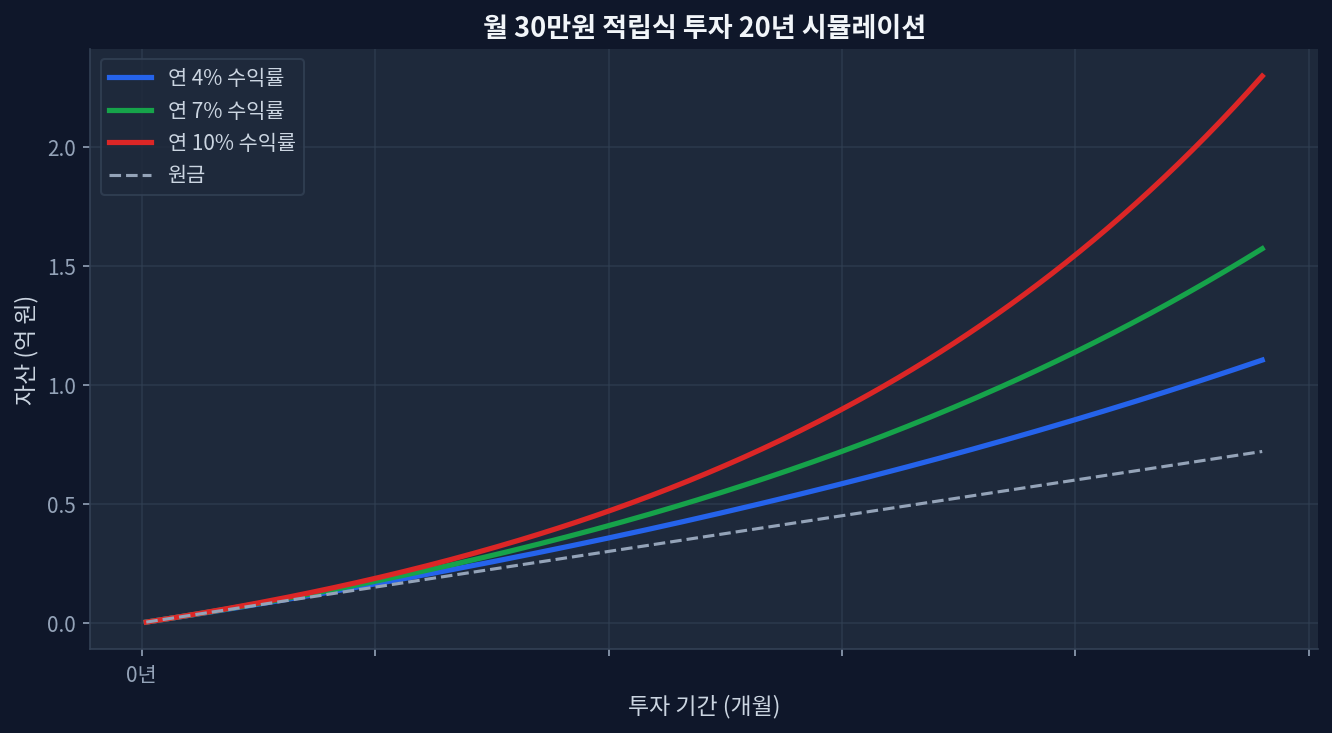

Empirical Simulation: Risk-Return Spectrum on $1,000 Monthly Contributions

As demonstrated by the empirical simulation, 100% risk-asset exposure does not uniformly guarantee optimal risk-adjusted outcomes. Market consensus interprets 401(k) fixed-income mandates as unnecessary drag on total return. However, empirical drawdown data confirms this structural constraint functions as a primary defensive layer against extreme tail risks. In a regime of elevated volatility, the intrinsic value of forced diversification mechanisms requires rigorous data-driven revaluation.

Comparative Analysis: Expense Ratios and Core ETF Liquidity

Standard advisory models suggest maximizing the $7,000 IRA limit before funding the 401(k). Strategic account distribution, however, demands a fundamental analysis of underlying expense ratios and liquidity parameters. [SEC Fund Fee Disclosures] Reviewing the cost structure of primary ETFs utilized across these accounts clarifies the necessity of strategic asset location.

| Product Name | Expense Ratio | Dividend Yield | 5Y Return | 1Y Return |

|---|---|---|---|---|

| Vanguard S&P 500 ETF (VOO) | 0.03% | 1.3% | 85.2% | 28.1% |

| Invesco QQQ Trust (QQQ) | 0.20% | 0.6% | 132.5% | 42.6% |

| JPMorgan Equity Premium Income (JEPI) | 0.35% | 7.2% | N/A | 12.4% |

Self-directed IRAs inherently lack administrative maintenance fees, optimizing the long-term compounding velocity of low-cost ETFs. Conversely, employer 401(k) plans frequently assess administrative fees ranging from 0.1% to 0.5% on aggregate assets, creating a dual-layered expense burden when combined with fund costs. The defining risk remains liquidity. While an IRA allows partial liquidations (subject to tax penalties), a 401(k) strictly prohibits in-service non-hardship withdrawals. This rigid illiquidity represents a structural vulnerability for capital deployed during peak consumption decades.

Divergent Perspectives and Disconfirming Evidence

Mainstream financial media advocates maximizing the unrestricted IRA first to capture 100% equity upside. This diverges from the market narrative on behavioral finance. For investors susceptible to psychological volatility—those prone to liquidating at the trough of a -20% contraction—prioritizing a 401(k) with forced fixed-income allocations mathematically increases the probability of long-term capital survival. The structural rigidity of a mixed-asset 401(k) serves as an effective behavioral firewall against irrational panic selling.

Scenarios where this analysis could miss clearly exist. This quantitative model operates on the historical assumption that equity markets compound at 7-10% annualized despite short-term drawdowns. However, if a secular stagnation regime materializes—analogous to Japan's Lost Decades or the S&P 500's zero-return decade in the early 2000s—the paradigm shifts. In such macroeconomic environments, inflation structurally outpaces stagnant equity returns, fundamentally destroying purchasing power despite initial tax deductions. [FRED U.S. Inflation Data] Decades of absolute capital lockup transform into massive opportunity costs.

Data-Driven Portfolio Optimization Models

Cross-verifying the structural parameters of IRAs and 401(k)s confirms that bifurcating assets by objective yields superior risk-adjusted metrics. Locating aggressive growth assets (e.g., QQQ) in the highly flexible SDIRA maximizes capital appreciation potential. Simultaneously, positioning dividend-growth assets (e.g., SCHD) and fixed income within the 401(k) establishes a robust income-generating anchor, mathematically isolating volatility.

Driven by empirical data, the optimal allocation model prioritizes funding the $7,000 IRA threshold for structural flexibility, followed by deploying residual capital into a dividend and fixed-income centric 401(k) allocation. This sequencing mitigates the catastrophic risk of total liquidity isolation during severe market contractions. Blindly chasing maximum contribution limits without rigorous stress-testing against personal cash flow requirements critically compromises portfolio maneuverability during recessionary cycles.

Structural Mechanics and Technical Inquiries

- Q1. Should investors simultaneously fund both an IRA and a 401(k)?

- Assuming sufficient capital velocity to maximize both accounts, parallel funding mathematically optimizes annual tax efficiency. However, under constrained cash flow, prioritizing the IRA provides superior liquidity management, permitting penalized but accessible withdrawals in emergency scenarios.

<dt><strong>Q2. Can the fixed-income mandates in employer 401(k)s be circumvented?</strong></dt>

<dd>Total circumvention relies on specific plan documents. Utilizing a Self-Directed Brokerage Account (SDBA) window within the 401(k), if offered, allows 100% equity allocation. Alternatively, selecting the furthest-dated Target Date Fund (e.g., 2065) synthetically replicates an equity-heavy exposure, pushing the risk-asset allocation to approximately 90%.</dd>

<dt><strong>Q3. Is the 10% early withdrawal penalty universally applied to the entire principal?</strong></dt>

<dd>In a Traditional IRA, the 10% penalty and standard income taxes apply to the entire distributed amount. For Roth IRAs, original contributions can be withdrawn penalty-free and tax-free at any time; only the earnings component faces taxation and penalties if withdrawn prior to age 59½.</dd>

<dt><strong>Q4. Can foreign-listed equities be directly purchased within these accounts?</strong></dt>

<dd>Standard 401(k)s strictly limit options to US-domiciled mutual funds or CITs. However, a Self-Directed IRA permits the purchase of American Depositary Receipts (ADRs) and specific foreign equities traded on US exchanges, functioning as a conduit for international exposure.</dd>

<dt><strong>Q5. How do marginal tax brackets impact the real value of the deduction?</strong></dt>

<dd>The quantitative value of a Traditional IRA or 401(k) deduction scales linearly with the investor's top marginal bracket. A $10,000 contribution yields a $2,400 immediate return at the 24% bracket, but only $1,200 at the 12% bracket, dictating a mathematically divergent strategy between Traditional and Roth structures depending on current versus terminal income projections.</dd>

This site is supported by Google AdSense advertising revenue. We receive no compensation or sponsorship from any ETF, broker, or financial product.