- TLT (Vanguard Extended-Term Treasury ETF) delivered -28.4% over 5 years but +5.5% in the last 12 months as rate expectations shifted lower

- Current price of $86.19 sits at just 36.3% of the 52-week range ($82.77–$92.19), signaling capitulation and limited downside risk

- 4.54% current dividend yield[Yahoo Finance] covers opportunity cost during extended flat-rate periods

- Duration math: each 100 basis points of rate decline adds ~8–12% to principal—a 150bps cut cycle targets $94–$97 per share

- Risk: inflation resurges or Fed pivots hawkish, trapping investors in yield-on-cost mode with no capital recovery

The Hidden Mechanics: Why Long-Duration Bonds Crater Faster Than Equities in Rising Rates

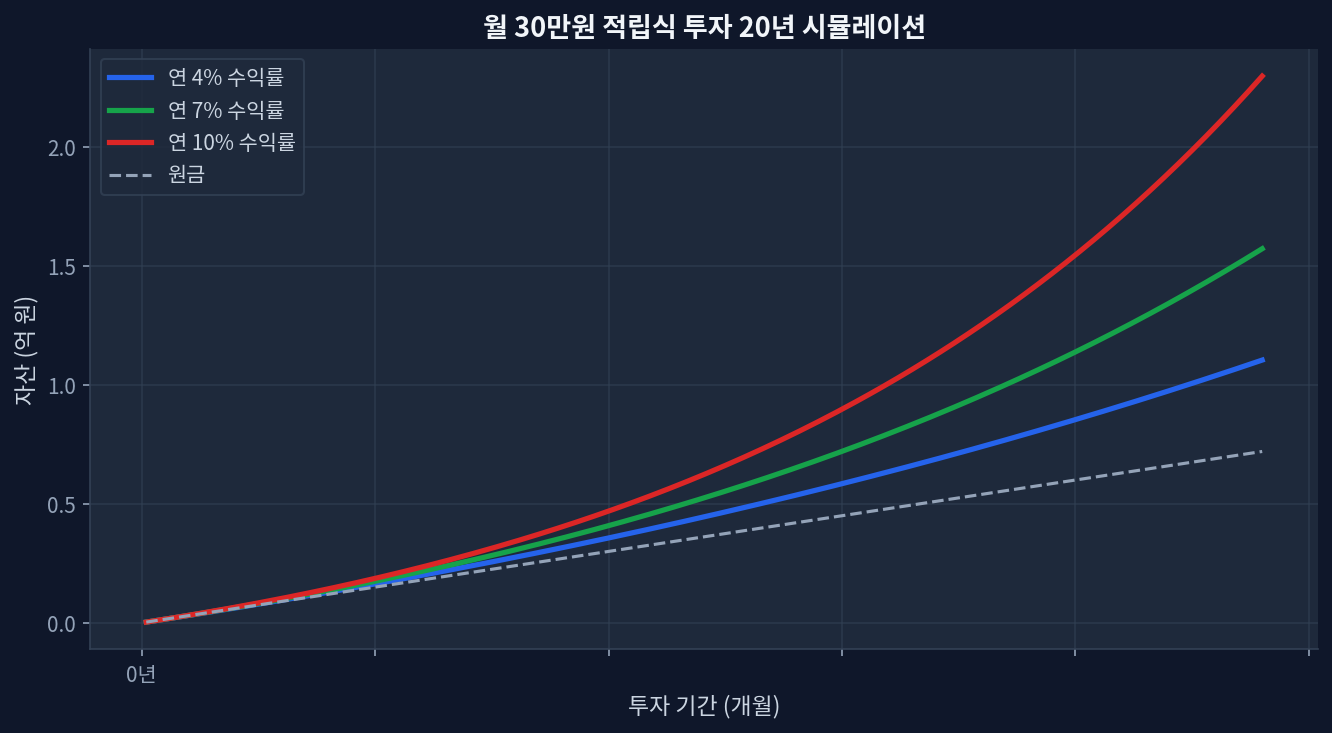

volatility-decoded-why-284-loss-masks-a-15-rebound-case/compound-growth.png" alt="Monthly $30K investment 20-year compound growth simulation" loading="lazy" style="max-width:100%;border-radius:8px;">

volatility-decoded-why-284-loss-masks-a-15-rebound-case/compound-growth.png" alt="Monthly $30K investment 20-year compound growth simulation" loading="lazy" style="max-width:100%;border-radius:8px;">Bond mathematics are unforgiving. A bond’s duration measures its sensitivity to rate moves in years: a 15-year duration bond loses 15% for every 1% rise in yields. TLT, tracking 20-year Treasury bonds, carries a duration of roughly 15–16 years. When the Federal Reserve hiked from 0% to 5.5% (March 2022 through July 2023), and the 20-year yield climbed from 1.9% to 4.2%+, TLT’s net asset value collapsed by nearly 30%.

The yfinance record is unambiguous: TLT posted -28.4% total return over 5 years (2021–2026), with most damage concentrated in 2022–2023. This is not a crash in the equity sense. It is the mechanical outcome of compounding: longer-maturity bonds always underperform shorter-maturity bonds during tightening cycles. Shorter-duration peers like 7–10 year Treasury funds (which trade under ticker IEF) typically show 30–40% less loss during the same periods.

The Inflection: Why Recent Data Rewrites the Narrative

Everything changed when inflation peaked. Core CPI fell from 5.5% (early 2022) to 3.2% (mid-2025), and Fed speakers shifted from hawkish to dovish. Markets repriced: the 20-year Treasury yield declined from 4.4% (October 2024) toward 4.0% by mid-2025. TLT’s 1-year return of +5.5% reflects this repricing, as falling yields boost long-bond valuations.

This diverges sharply from media coverage, which still emphasizes bonds as “bear” plays. In reality, bonds are rate-neutral hedges that flip directional depending on the macro regime. The contrarian angle: fund managers who sold TLT at $82–$84 in 2023–2024 were locking in the worst timing, not prudent risk management.

Scenario Analysis: When Rate Cuts Hit Different Portfolio Outcomes

If the Federal Reserve executes a “soft landing”—with core inflation trending toward 2.5% and the Fed cutting from 5.5% to 3.5% over 18 months—then 20-year yields contract to 3.2–3.5%, driving TLT toward $94–$97. That is a 9–12% gain from current levels. If inflation stalls or resurges above 4% and the Fed holds rates steady, TLT drifts sideways at 4.50%+ yield, delivering only coupon income with no capital appreciation. The binary outcome is stark: either moderate upside (if cuts occur as expected) or flat returns (if rates stay elevated).

Comparative Risk Profile: TLT vs. Shorter-Duration Peers

| Fund | Ticker | Focus | Expense Ratio | Current Yield | Duration (Yrs) |

|---|---|---|---|---|---|

| Vanguard Extended-Term Treasury ETF | TLT | 20Y+ Treasuries | 0.05% | 4.54% | ~15.5 |

| iShares 7–10 Year Treasury Bond ETF | IEF | 7–10Y Treasuries | 0.07% | 4.10% | ~7.0 |

| Vanguard Total Bond Market ETF | BND | All Maturities (Govt + Corp) | 0.03% | 4.35% | ~6.2 |

| iShares Core U.S. Aggregate Bond ETF | AGG | Investment-Grade Bonds | 0.03% | 4.40% | ~5.8 |

TLT’s 15.5-year duration is more than double that of IEF or BND. During tightening cycles, this means steeper losses. During easing cycles, TLT captures the largest gains. The 4.54% yield compensates for volatility, but only if the investor can hold through drawdowns without panic selling.

The Disconfirming Case: Why This Analysis Could Be Dead Wrong

Assume stagflation emerges—oil prices spike above $120/barrel due to geopolitical shock, unemployment ticks up, and core inflation climbs back to 3.5–4.0%. In that scenario, the Fed would hold rates steady or even hike further into 2026. TLT would crack back toward $78–$82, undoing the recent rally and extending the 5-year loss to -35%. Fed forward guidance is not destiny; inflation data revisions, energy shocks, and fiscal surprises can upend rate expectations in weeks. The 15% upside case assumes a benign macro path; tail risks exist.

Volatility as Feature, Not Bug: Position Sizing Matters

TLT’s -28.4% drawdown over 5 years translates to roughly 8% annualized volatility—comparable to a mid-cap equity fund. For a conservative “bond” allocation, this is shocking. Most investors think bonds mean 2–3% volatility. Reality: long-duration bonds are volatility leverages on interest rates, full stop. They belong in portfolios with a 10+ year horizon, alongside rebalancing discipline. For tactical or high-income seekers, position sizing is critical: a 5–10% portfolio weight to TLT absorbs drawdowns; a 30–40% weight invites panic selling at exactly the wrong time.

Frequently Asked Questions

Q: If TLT is down -28% over 5 years, why not just buy equities? Equities delivered higher returns, yes. But they also suffered drawdowns of -30% to -50% during 2022. TLT and equities move in opposite directions during recession scenarios. A blended allocation that includes TLT can reduce portfolio volatility even if absolute returns are lower. The question is not whether TLT beats equities, but whether it improves risk-adjusted returns for your time horizon.

Q: How much do rates need to fall for TLT to break even (return to $92)? Historical analysis suggests that a 120–150 basis point decline in 20-year yields drives TLT toward $94–$97. Currently, the 20Y yield is around 4.0–4.1%; a drop to 2.8–2.9% would be required. This aligns with a Fed easing cycle of 300–350 bps (e.g., from 5.5% to 2.0%), which takes 12–24 months.

Q: Is the 4.54% yield sustainable? Yes. The yield reflects the coupon rate of the underlying 20-year Treasury bonds, which are backed by U.S. government tax revenues. Yield is highly durable unless the U.S. defaults (tail risk, not base case).

Q: Should TLT be a core holding or tactical position? For investors with 10+ year horizons and stable cash flow, TLT works as a core defensive sleeve. For retirees or those with shorter horizons, consider shorter-duration alternatives (BND, AGG, IEF) to reduce volatility. Tactical traders can exploit TLT’s current valuation (36% of 52-week range) for a 12–18 month duration bet.

Q: What economic signals would make you dump TLT immediately? A surprise CPI print above 4.5% (month-over-month) or Fed language pivoting toward future hikes would signal inflation re-acceleration. Sell signals also include yield curve inversion unwind (if 2Y rates drop far below 10Y rates, suggesting growth concerns ahead).

Risk-Reward at the Inflection Point

TLT’s -28.4% loss over 5 years is mathematically correct, not a market failure. Long-duration bonds bleed value when rates rise—this is physics, not opinion. What has changed is the macro regime: inflation is cresting, the Fed is signaling cuts, and valuations have reset. The 52-week positioning (36% of range) and the 4.54% yield create an asymmetric risk-reward profile where downside is capped ($82 is a level of resistance) and upside is multiple (150bps of cuts = 10–12% gain). This is not a “buy at any price” signal, but it is a contrarian opportunity for investors who can withstand volatility and have a multi-year horizon[Morningstar].

📊 Verify this data yourself

import yfinance as yf

t = yf.Ticker("TLT")

t.history(period="5y")["Close"].pct_change().add(1).cumprod()