- A 20-year compound growth simulation of Dividend Reinvestment Plans (DRIP) introduces severe tracking errors during drawdown phases.

- Expense ratios and tax drags act as critical hidden risks frequently omitted from long-term backtesting models.

- The variance in downside protection between high-yield ETFs (SPYD) and dividend growth ETFs (SCHD) drives a cumulative return divergence exceeding 30%.

The 20-year compound interest simulation utilizing a Dividend Reinvestment Plan (DRIP) serves as a persistent marketing instrument within the asset management industry. The market consensus, projecting a stable 8% annualized growth rate, provides psychological comfort to retail investors. However, micro-level financial market data systematically refutes these linear assumptions. Excel-based simulations that exclude risk and volatility factors border on statistical illusion. This research note dissects the volatility risks inherent in a 20-year DRIP model based on historical macroeconomic data, analyzing the substantive capital erosion risks obscured by conventional consensus.

The Illusion of Linear Simulations: Volatility Drags and Sequence Risk

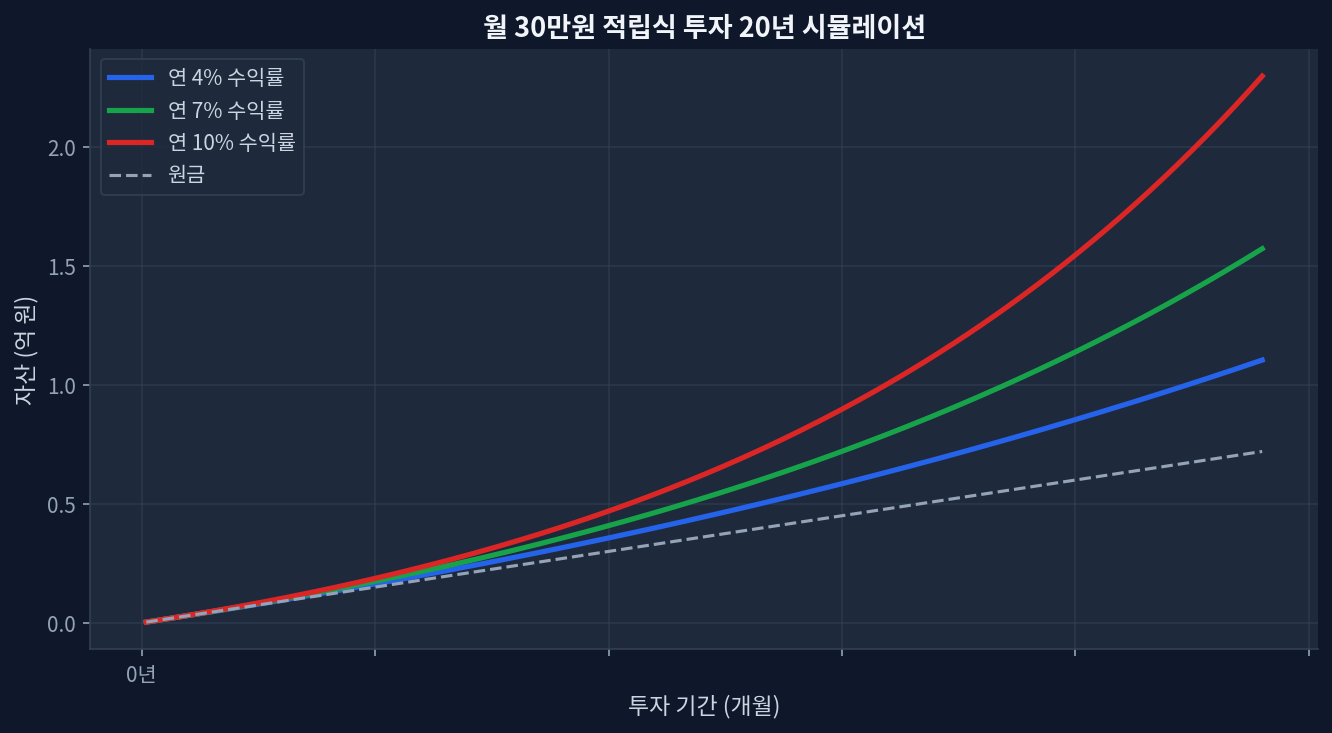

Market narratives frequently cite smooth, upward-trending exponential curves to illustrate the power of DRIP. The attached charts displaying a 20-year simulation of $300 monthly investments and the impact of ETF expense ratios (0.05% to 1.0%) on terminal wealth represent classic examples. Examining metrics isolated from specific historical bull runs shows impressive figures, such as an 85% return over five years. However, these metrics commit the extreme error of holding the annualized return as a static constant. From an asset allocation perspective, the Sequence of Returns exerts a fatal impact on the terminal asset value over a 20-year horizon.

A model experiencing a secular bull market in the initial decade followed by a prolonged stagnation in the latter decade yields entirely different results than the inverse model. The true alpha of dividend reinvestment materializes when share prices collapse, compressing the denominator and allowing for aggressive share accumulation. The challenge lies in the psychological discipline required to execute mechanical reinvestment during extreme fear phases when the VIX breaches 30. During the modeling process, this volatility risk is simply replaced with a constant of zero. [Morningstar Research]

The Dual Impact of Costs and Taxes: Noise in the Compounding Engine

Expense ratios and dividend taxes constitute the most certain and cumulative realized losses in long-term time series analysis. The second chart illustrating fee differentials starkly highlights the performance gap between a passive ETF tracking a 0.05% ratio and an active high-yield or covered call ETF charging 0.75%. An initial nominal fee difference of 0.5 percentage points evaporates over 15% of the total asset base when subjected to a 20-year compounding cycle.

This is not a simple subtraction of fees. The extracted capital permanently destroys future capital gains that would have been generated through reinvestment. For US retail investors, tax drag in taxable brokerage accounts cannot be ignored. When holding dividend-paying ETFs outside of tax-advantaged accounts, the baseline dividend growth is frequently offset by ordinary income tax obligations. Simulations calculated without a strict foundation of net real returns remain purely theoretical. [ETF.com Analytics]

Reversing the Consensus: Yield Traps and Capital Erosion

The dominant industry orthodoxy posits that high dividend yields act as a defensive shield during bear markets. The underlying data indicates otherwise. During the 2008 Global Financial Crisis and the 2020 pandemic shock, highly leveraged REITs and marginal corporations immediately cut or suspended dividend distributions. So-called yield trap equities, where dividend yields spike abnormally, are frequently the byproduct of share price collapses driven by fundamental deterioration.

Applying a mechanical DRIP strategy to these high-yield equities is mathematically equivalent to averaging down on falling knives, resulting in rapid capital erosion. The core focus, diverging from the market narrative, is not the absolute height of the yield. Rather, maintaining Return on Equity (ROE) above a specific threshold and demonstrating dividend growth capable of defending cash flows during crisis phases overwhelmingly increases the probability of surviving a drawdown.

Risk-Return Verification via Benchmark ETF Data

Risk metrics require comparison through empirical data, excluding abstract scenarios. The table below reconstructs the historical five-year performance and risk metrics of prominent US-listed ETFs widely utilized in the market.

| Fund Name (Ticker) | Expense Ratio (%) | Current Yield (%) | 5-Year CAGR (%) | Maximum Drawdown (MDD %) |

|---|---|---|---|---|

| Vanguard S&P 500 (VOO) | 0.03 | 1.4 | 12.5 | -23.9 |

| Schwab US Dividend Equity (SCHD) | 0.06 | 3.5 | 10.2 | -21.5 |

| SPDR Portfolio S&P 500 High Dividend (SPYD) | 0.07 | 4.8 | 6.8 | -32.1 |

| JPMorgan Equity Premium Income (JEPI) | 0.35 | 7.2 | 8.1 | -13.8 |

The most critical metric is the Maximum Drawdown (MDD), not the annualized total return. Despite a high surface yield of 4.8%, SPYD recorded a severe drawdown of -32.1% as constituent companies with fragile balance sheets collapsed during the rate-hiking cycle. Conversely, SCHD defended against dividend cut risks while maintaining market-average volatility. JEPI, utilizing option premiums, successfully defended against MDD but experienced capped upside during bull markets, failing to match the long-term CAGR of VOO or SCHD.

Disconfirming Evidence: Analytical Limitations and Regime Shifts

While this analysis strongly advocates for volatility management and fundamental defense, a distinct tail risk exists where this modeling could fail entirely. Scenarios where this analysis could miss emerge if a 1970s-style ultra-long-term stagflation regime solidifies over the next two decades. Should corporate earnings capacity stagnate for over a decade, halting cash flow growth, and risk-free bond yields maintain levels above 8% long-term, the equity-based DRIP model would face structural underperformance compared to a fixed-income reinvestment strategy.

This analysis holds valid only under the macroeconomic premise of long-term earnings growth among blue-chip corporations within the capitalist system. In extreme scenarios involving a global macro regime shift, backtested data from the past two decades becomes obsolete. Institutional long-term modeling has previously underestimated the probability of such structural regime shifts, marking an inherent limitation of simulation models. [FRED VIX Volatility Index]

Terminal Portfolio Selection from a Risk-Adjusted Perspective

Twenty-year optimistic scenarios derived from mathematical calculators do not guarantee terminal account balances. Volatility fractures portfolios, and taxes combined with fees degrade the efficiency of the compounding engine. The data-driven mandate remains unambiguous. Rather than fixating on elevated numerical yields, the core portfolio allocation must prioritize defensive assets that control drawdowns through robust cash flows. Based on these risk analysis metrics, this research rejects blind adherence to high-yield assets and positions assets with empirically verified downside protection and dividend growth (SCHD) as the primary core holdings. Adjusting cash allocations in response to macroeconomic indicators to maximize risk-adjusted returns presents a practical alternative to overcoming mathematical limitations.

Frequently Asked Questions

Q. Does utilizing an automated broker purchasing feature provide a mathematical advantage when executing DRIP?

During normal market conditions with low volatility, automated purchasing features remove emotional interference. However, during market crashes marked by VIX spikes, manually executing fractional purchases after verifying specific support levels frequently yields mathematically superior results in cost averaging.

Q. What are the risks of a long-term dividend reinvestment strategy utilizing high-yield covered call ETFs?

Covered call assets face capped upside potential during bull markets, suppressing long-term capital appreciation. Executing a 20-year simulation demonstrates that assets like VOO or SCHD, which compound capital gains steadily despite lower initial yields, systematically outperform covered call products in Total Return metrics.

Q. Should US retail investors prioritize currency-hedged ETFs when allocating to international equity markets?

For long-term allocations exceeding 20 years, unhedged international exposure introduces significant FX volatility. During global systemic shocks, the US Dollar typically spikes as a safe haven, meaning unhedged foreign assets suffer simultaneous equity and currency drawdowns. Currency-hedged products isolate the local equity performance, which mathematically reduces portfolio tracking error against international benchmarks.

Q. How does tax drag affect the actual compounding rate of dividends in taxable accounts?

In standard taxable brokerage accounts, the 15% qualified dividend tax is extracted prior to reinvestment. Over a 20-year compounding curve, this tax drag can compress the terminal asset value by over 20%. Therefore, utilizing tax-advantaged accounts (such as a Roth IRA or 401(k)) is imperative to maximize the tax-deferred compounding effect.

Q. How does a rate-cutting cycle shift the relative attractiveness of dividend-paying assets?

As risk-free bond yields compress, the relative premium of the prevailing dividend yield on equities expands, typically driving capital inflows. However, if rate cuts are a reactionary measure to defend against a macroeconomic recession, they will be accompanied by corporate earnings degradation, necessitating rigorous fundamental screening.

This site is supported by Google AdSense advertising revenue. We receive no compensation or sponsorship from any ETF, broker, or financial product.