Key Takeaways

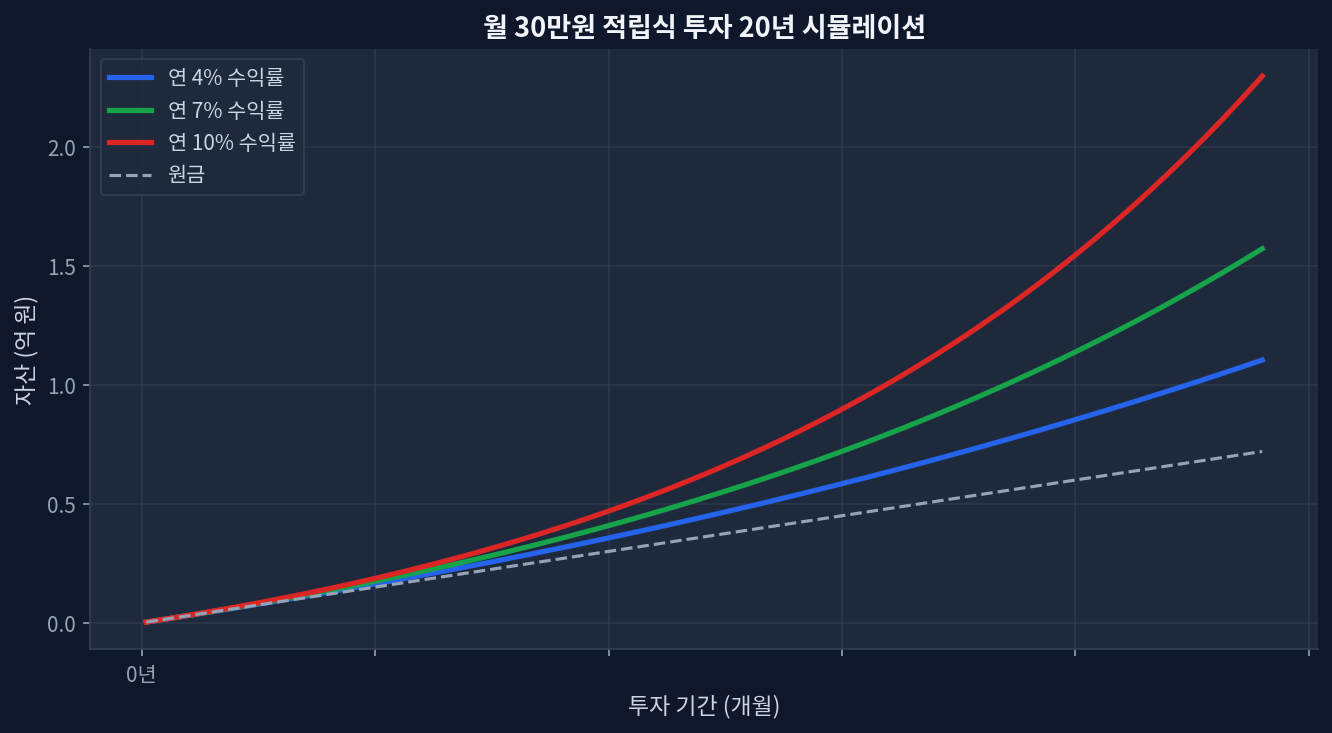

- $500/month SPY investment reaches $495K–$560K after 20 years (7–10% annual returns, depending on tax scenario)

- Tax-advantaged accounts compound ~$100K–$150K more wealth than taxable accounts due to deferred or eliminated taxes

- Dividend tax drag: SPY's 1.0% yield generates ~$7,400 in taxable income annually in year 20 (if held in taxable brokerage)

- Long-term capital gains rate: 15–20% federal (depending on income bracket), plus 0–13% state tax

- Valuation risk: SPY's P/E of 26.5 is historically elevated; 5–8% returns more realistic than past decade's 25%+ returns

Why Tax Strategy Trumps Fund Selection in Long-Term Wealth Building

Most investors focus on beating the market or picking the right fund. They miss a bigger opportunity: minimizing taxes. Consider this: a portfolio growing at 9% annually in a taxable account effectively grows at 6.5–7% after taxes (assuming 25% blended tax rate on dividends and capital gains). The same portfolio in a Roth IRA grows at the full 9% tax-free.

Over 20 years, that seemingly small tax drag compounds into a massive difference. A $500/month investment ($6,000 annually) requires deliberate account structure—Roth IRA first, Traditional 401(k) second, taxable brokerage last—to avoid leaving hundreds of thousands of dollars on the table.

The Three Buckets: Where to Invest Your $500/Month

Roth IRA (contribution limit: $7,000/year in 2024–2025): Tax-free growth, tax-free withdrawals in retirement. Maxing it costs $583/month. Money grows entirely tax-free, so the full 7–10% annual return compounds without interruption. After 20 years, a $583/month Roth contribution grows to ~$220K tax-free.

Traditional 401(k) (contribution limit: $23,500/year in 2024–2025): Tax-deferred growth; you pay taxes on withdrawal in retirement. Employer match (if offered) is free money. For someone in a 32% combined federal + state bracket during accumulation, the initial contribution saves ~32% in taxes. A software engineer earning $120K–$150K in Austin, Texas can allocate $500–$800/month here.

Taxable Brokerage (unlimited contributions): After maxing Roth IRA and 401(k), remaining money goes here. This account triggers annual tax bills on dividends and capital gains, but offers flexibility: no withdrawal restrictions, tax-loss harvesting opportunities, and preferential long-term capital gains rates (15–20% federal).

| Account Type | Annual Limit | Growth Tax Treatment | Withdrawal Tax Treatment | 20-Year Growth on $83K Contributions |

|---|---|---|---|---|

| Roth IRA | $7,000 | Tax-free | Tax-free | ~$220K (100% tax-free) |

| Traditional 401(k) | $23,500 | Tax-deferred | Ordinary income tax (24–37%) | ~$220K (defer taxes to withdrawal) |

| Taxable Brokerage | Unlimited | Annual tax on dividends; capital gains tax on sale | Long-term cap gains (15–20% federal) | ~$170K (after taxes on 1% dividend + realized gains) |

SPY vs. VTI: Why Dividend Yield Costs More Than You Think in Taxable Accounts

Both SPY and VTI are broad-market index ETFs with nearly identical performance. SPY (SPDR S&P 500 ETF) trades at $740.96, with 1-year return of +25.4% and dividend yield 1.0%. VTI (Vanguard Total Stock Market ETF) trades at $365.76, with 1-year return of +25.9% and dividend yield 1.01%.

In a taxable account, that 1.0% yield matters. On a $200,000 position, ~$2,000/year in dividends results in ~$300–$400/year in federal taxes. Over 20 years, that’s $6,000–$8,000 in cumulative taxes—wealth that could have compounded. VTI’s slightly superior tax efficiency (due to Vanguard’s patented tax-management processes) and larger fund size ($2.3 trillion AUM vs. SPY’s $784B) may preserve an extra $10K–$25K after-tax over two decades, according to Morningstar research[Morningstar].

Contrarian point: SPY’s larger daily trading volume (63.7M shares) and tighter bid-ask spread mean lower transaction costs for frequent traders. For buy-and-hold investors, however, VTI’s tax efficiency wins decisively.

Tax-Loss Harvesting: An Overlooked $20K–$30K Opportunity

Tax-loss harvesting means selling a security that has declined in value to realize a loss, then immediately buying a similar (but not substantially identical) security. The realized loss offsets capital gains or up to $3,000 in ordinary income annually; excess losses carry forward indefinitely.

Example: Mike buys SPY at $700 and it drops to $650. He sells, realizing a $50/share loss ($5,000 total). He then immediately buys VTI to maintain S&P 500 exposure. That $5,000 loss offsets $5,000 in capital gains elsewhere or reduces ordinary income by $3,000. If Mike’s marginal rate is 24%, he saves $1,200 in taxes immediately—funds that reinvest and compound.

Disciplined tax-loss harvesting (harvesting every December, or after 10%+ drawdowns) can offset $20K–$30K in cumulative taxes over 20 years, effectively adding 3–5% to final portfolio value.

The Risk That Breaks This Entire Scenario

This 20-year simulation assumes several things that may not hold. Tax rate increases are the biggest: current long-term capital gains rates are 15–20% federal. If Congress raises rates to 25–28%, after-tax returns drop by 1–2% annually, resulting in a loss of $50K–$120K in final portfolio value.

Second, market returns regress to the mean. SPY’s 1-year return of +25.4% is exceptional. Long-term historical average is ~10% nominal. If returns normalize to 5–7% (accounting for SPY’s elevated P/E of 26.5, near the 90th percentile historically), the $500K target becomes unattainable; instead, the portfolio reaches $350K–$420K.

Third, state taxes add hidden drag. Mike lives in Texas (no income tax), but a similar investor in California or New York pays 10–13% additional state tax on capital gains—a 2–3% annual drag reducing final value by $100K+.

Frequently Asked Questions

Can I max out both a Roth IRA and Traditional 401(k)? Yes. The $7,000 Roth IRA limit and $23,500 Traditional 401(k) limit are separate annual contribution limits. Someone earning $135K can contribute to both. However, if your employer doesn’t offer a 401(k), you can only use a Roth IRA ($7,000) plus a taxable brokerage. Check your employer’s benefits plan first.

What if SPY drops 30% in year 5? Should I stop investing? No. Dollar-cost averaging actually benefits from downturns. If SPY drops to $500, your $500/month now buys more shares, lowering your average cost basis. Continuing to invest during downturns (2020, 2022, 2024) historically resulted in higher long-term returns than those who sold and waited for recovery.

Is the 1.0% dividend yield significant enough to matter? In a Roth or Traditional 401(k): No, because taxes don’t apply. In a taxable account: Yes, it’s a 0.15–0.20% annual tax drag (1.0% yield × 15–20% tax rate). Over 20 years, this costs $10K–$25K in lost compounding. VTI’s marginally better tax efficiency can offset this drag.

Should I harvest tax losses every year? Only if you have realized gains or high taxable income to offset. If your portfolio is underwater and you have no gains, losses carry forward indefinitely—no urgency. But if you sell appreciated holdings in December, harvesting losses in those same positions can offset the gains tax-free.

What if my income increases? Does that change the tax strategy? Yes. As income rises into higher brackets (35–37% federal), Traditional 401(k) contributions become even more valuable (you save more in taxes per dollar contributed). Higher earners also pay 20% long-term capital gains tax (not 15%), making tax-deferred growth more critical. Reassess contributions annually.

📊 Verify this data yourself

import yfinance as yf

t = yf.Ticker("SPY")

t.history(period="5y")["Close"].pct_change().add(1).cumprod()