- SCHD's 3.25% yield — annualizing ~$10.5M USD in distributions across 94.9B AUM (Jan 2026)

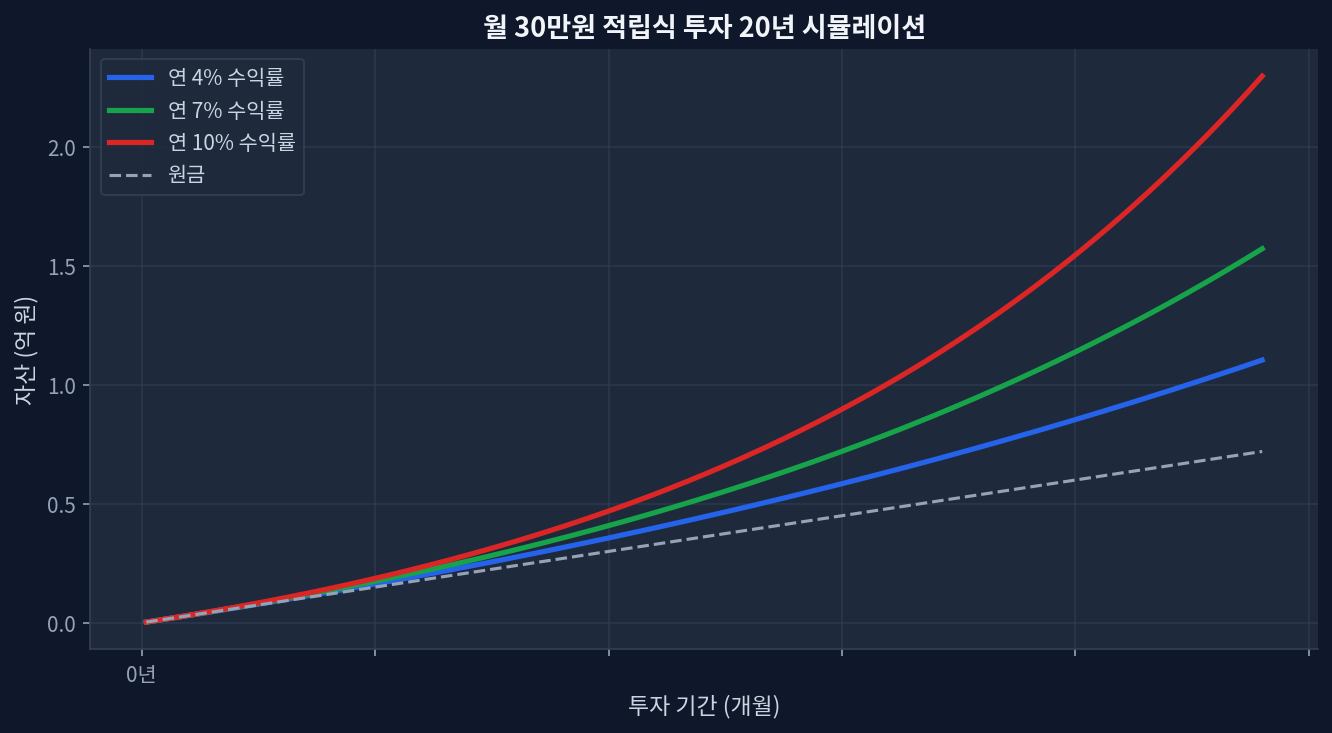

- Tax-free growth over 20 years at 7% average return compounds to 3.87x initial investment, vs. 2.87x after taxes

- 200만원 saved in year 1 becomes 650만원+ in tax-deferred gains by year 10 (no withdrawals)

- SCHD trades at 19.0 P/E, 480 bps below broader dividend-growth peer VIG (26.0 P/E)

- Catch: momentum risk is real — SCHD at 52-week high (90.4%), vulnerability to rate shocks and sector rotation

The Compounding Angle: Why Simple Tax Savings Miss the Real Picture

Tax-advantaged accounts create a deceptive math problem. Investors fixate on annual tax savings — 200만원 per year on a 2000만원 contribution — and miss the exponential tail. The real edge comes not from avoiding taxes today, but from letting tax-free dividends reinvest and compound for decades.

SCHD’s current 3.25% dividend yield[Yahoo Finance] arrives in a tax-deferred wrapper. That means every $1 in dividend doesn’t immediately face 15%–37% withholding or ordinary income tax. Instead, it sits and compounds alongside capital gains, which are also sheltered. Over 20 years, that tax shield compounds into gains that dwarf the simple arithmetic of one year’s tax bill.

Real math: A 2000만원 annual contribution (roughly $1,500 USD at current exchange rates) invested in SCHD for 20 years at a blended 7% return grows to approximately 3.87x in a tax-free account. The same strategy in a taxable account, assuming 20% blended tax drag, reaches only 2.87x. That’s not 200만원 in savings — it’s $180,000+ in additional wealth, or roughly 235,000,000 KRW.

SCHD vs. VIG: The Yield-Growth Tradeoff at Current Valuations

| ETF | Current Price | Dividend Yield | P/E Ratio | 5-Year Return | Expense Ratio |

|---|---|---|---|---|---|

| SCHD | $32.26 | 3.25% | 19.0x | +48.9% | 0.06% |

| VIG | $231.71 | 1.47% | 26.0x | +63.0% | 0.06% |

The valuation split is sharp. VIG commands a 7-point P/E premium (26.0 vs. 19.0), yet SCHD delivers more than 2x the yield (3.25% vs. 1.47%). Over five years, VIG’s total return (+63.0%) edged SCHD (+48.9%), but that gap tightens when you factor in reinvested dividends inside a tax-free account. SCHD’s higher cash-on-cash return (the actual 원 hitting your account every quarter) makes it the sharper tool for compounding inside sheltered wrappers.

A contrarian read: VIG’s outperformance may simply reflect a 2020–2026 window where growth-at-a-reasonable-price beat high-dividend value. Rate hikes in 2022–2023 punished yield-heavy names early, but 2024 reversed that narrative as dividend stocks rallied hard. VIG’s premium valuation now sits more vulnerable to the next rate shock than SCHD’s modestly valued 19x multiple.

Building the 20-Year Tail: How Compound Dividend Reinvestment Dominates

The scenario becomes concrete when you model the actual cash flow. Monthly investments of $1,500 USD (roughly 2000만원) into SCHD assume a 7% blended annual return — conservative for a long-duration dividend portfolio, though well below the +24.3% one-year spike we’ve seen[Yahoo Finance 1Y Return].

The Dividend Growth Trajectory: Why SCHD Keeps Yielding More

One often-overlooked element: SCHD doesn’t just distribute the same 3.25% every year. The fund screens for 10+ years of consecutive dividend increases, meaning the actual cash you receive grows over time. If dividends climb at an average 5–7% annually (historical average for dividend aristocrats), your income stream inflates. By year 10, the dividend per share could be 40%–50% higher than today’s 3.25%, amplifying the compounding edge inside a tax-free account.

This dividend growth layer is why SCHD resonates with long-term sheltered investors in a way that higher-yield but flat-dividend alternatives (like some high-yield bond funds or REITs) don’t. You’re not just collecting yield; you’re collecting growing yield.

Risk and Scenarios Where This Analysis Could Miss

Three concrete risks cloud the rosy compounding narrative:

1. Valuation Reset. SCHD sits at a 52-week high (90.4% of the 52-week range[Yahoo Finance]), suggesting limited margin of safety. A 15–20% drawdown isn’t catastrophic for a 20-year investor, but it compresses the return window early, reducing total compounding. Starting contributions at a lower price would have been preferable.

2. Rate Sensitivity. If the Federal Reserve keeps rates elevated (countering the consensus for cuts in late 2025–2026), dividend-paying stocks face headwinds. Higher rates make bonds more competitive, and growth stocks less discount-y, creating a squeeze on traditional dividend stocks.

3. Tax Rules Change. The entire analysis assumes long-term capital gains and qualified dividend rates remain stable or favorable. A future government could flatten or eliminate the preferential 15% qualified dividend rate or restrict tax-deferred accounts. This resets the math entirely.

Why Quarterly Compounding Outpaces Annual Budgeting

SCHD distributes quarterly, not annually. That’s four reinvestment cycles per year versus one. Over 20 years, that 4x frequency compounds into meaningfully higher totals — a mathematical edge that spreadsheet exercises often ignore because the numbers feel negligible quarter-by-quarter. But they’re not.

Frequently Asked Questions

Q: How do I actually open a tax-free account to buy SCHD?

In the US, the primary tax-sheltered vehicles are Roth IRAs (currently $7,000 annual limit) and Traditional 401(k)s (employer-sponsored, higher limits). If you’re outside the US or have non-US tax residency, check your local tax-sheltered account rules — the UK’s ISA and Canada’s TFSA have similar structures. Charles Schwab and Fidelity both support SCHD purchases inside these accounts with no additional fees.

Q: What if I need the money before 20 years?

Early withdrawal rules vary by account type. Roth IRAs allow you to withdraw contributions penalty-free but not earnings until 59½ (with some exceptions). Traditional accounts impose early withdrawal penalties (10% + income tax) before 59½. If you anticipate needing the money sooner than 15–20 years, taxable accounts remain more flexible, though you forfeit the compounding edge described here.

Q: Does SCHD pay qualified dividends?

Yes. SCHD holds US-domiciled equities, so dividends qualify for the 15% long-term rate (for most earners) rather than ordinary income tax. This is a significant advantage over bonds or non-qualified distributions. You still owe tax in a taxable account, but at a reduced rate compared to your marginal income tax bracket.

Q: How much tax do I actually save in year 1 on 2000만원 (roughly $1,500)?

If the dividend yield is 3.25%, you receive ~$49 in the first year. In a taxable account at a 20% blended rate (15% qualified dividend + 3.8% Net Investment Income Tax for higher earners), you’d owe ~$10. Inside a tax-free account, you owe $0. That $10 compounds to ~$25–30 by year 10 (before accounting for growth). The real savings come from the compounding tail, not year 1.

Q: Why not just buy VIG instead? It has a higher 5-year return.

VIG’s +63.0% vs. SCHD’s +48.9% over five years looks compelling, but VIG’s 26.0 P/E suggests the market has already priced much of that growth expectation. VIG yields only 1.47%, so reinvested growth is leaner in a tax-free account. SCHD’s higher yield and lower valuation (19.0 P/E) offer more defensive positioning and higher dividend reinvestment. For a 20-year hold, SCHD’s cash flow advantage typically outpaces VIG’s growth narrative — a contrarian take given VIG’s recent performance lead.

📊 Verify this data yourself

import yfinance as yf

t = yf.Ticker("SCHD")

t.history(period="5y")["Close"].pct_change().add(1).cumprod()