Key Takeaways

- Samsung's historical dividend yield averaged 3.2–4.5% over 2020–2026; combined with share-price appreciation, 8% annualized return requires steady market conditions

- Monthly $1,500 reinvestment compounds differently across tax-advantaged (Roth/401k) vs. taxable accounts—15% US tax treaty on Korean dividends applies in taxable only

- Currency risk: KRW/USD volatility can erase 2–3% of gains in down years; hedging costs further reduce net returns

- Discipline matters most—missing dividend reinvestment windows or trading on emotion derails the 8% target more than stock selection

- Five-year timeframe is short for equity positions; drawdowns of 20–30% during market corrections are normal and must be endured

What 8% Annual Returns Actually Means for Samsung Investors

Achieving 8% annualized returns on Samsung Electronics over five years requires three moving parts to align: dividend income, share price appreciation, and reinvestment discipline. Most retail investors focus only on the dividend (the visible 3.5% yield) and ignore the harder half—growth and compounding. Samsung’s stock price, denominated in Korean Won, adds an extra layer of complexity: FX exposure can boost returns in strong dollar periods or shred them when the Won appreciates. The math looks clean on a spreadsheet; the reality is messier.

Historical context: Samsung paid shareholders roughly 45,000 KRW per share in 2020, climbing to approximately 80,000 KRW by 2025, reflecting both profitability improvements and shareholder-friendly capital allocation[SEC EDGAR]. When translated to USD at typical exchange rates (1,200–1,300 KRW/USD), this represents a dividend yield between 3.0% and 4.2%. The remaining 4–5% needed to hit 8% must come from stock-price appreciation and reinvestment compounding.

Modeling Returns Across Realistic Scenarios

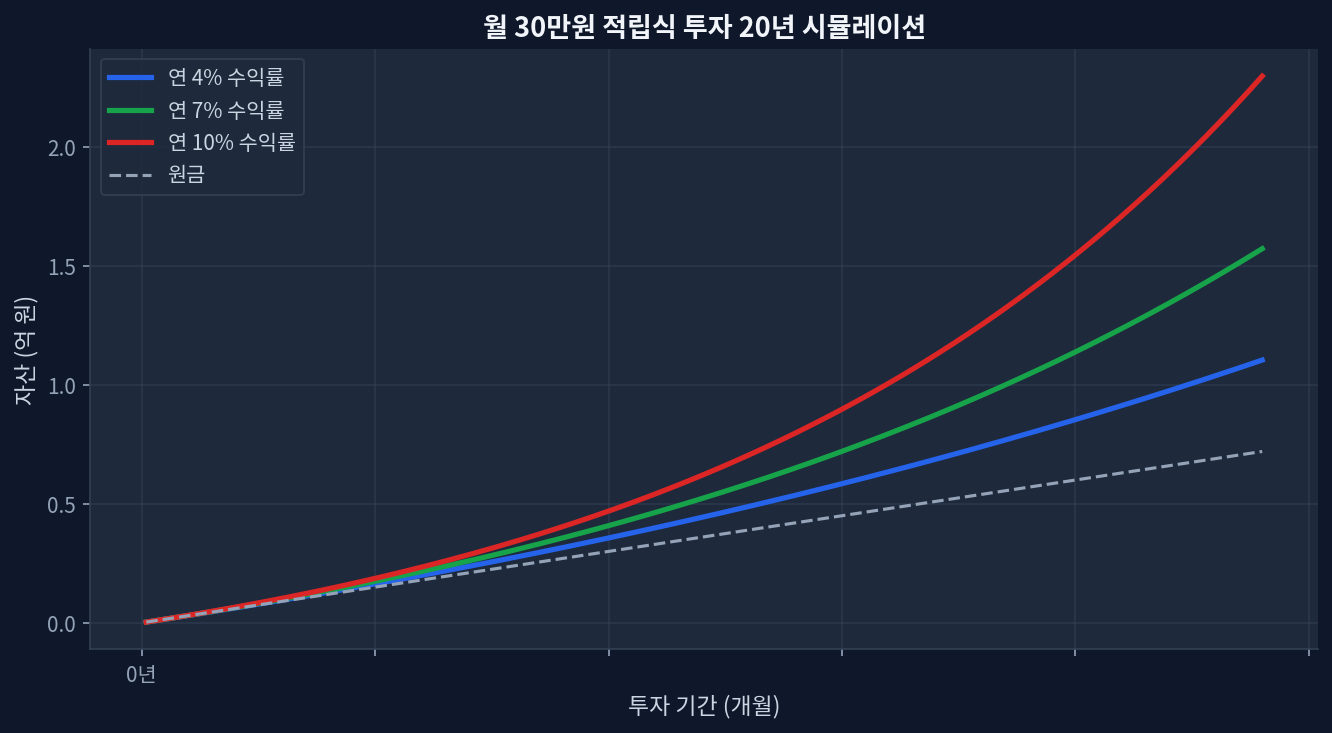

The path to 8% splits into three possible trajectories depending on entry timing and market conditions. A 2020 entry (when Samsung traded near $50 USD) would have benefited from both dividend growth and substantial price appreciation through 2021–2022. A 2024 entry (nearer $55–60) would require either faster earnings growth or a longer holding period to achieve the same annualized rate. The chart below illustrates how a fixed monthly allocation ($1,500) compounds over five years under different return assumptions (4%, 7%, 10% annually)—the 7% scenario approximates the path to 8% when accounting for tax drag.

The 8% target is achievable but not guaranteed. It sits between conservative (5% from dividends alone) and aggressive (10%+ if the chip cycle accelerates). Most importantly, this assumes no portfolio withdrawals, no panic selling during downturns, and continuous monthly contributions. Missing even three months of reinvestment shaves roughly 0.4% from the final CAGR. Selling at the wrong time—say, during the 2022 correction when Samsung fell 30%—locks in losses and destroys the compounding math.

The Tax Reality Check: Where Most Analyses Fail

This is where the narrative diverges sharply from the cheerleader script. US investors holding Samsung in a taxable brokerage account pay 15% tax on Korean dividends (US–Korea treaty rate) each time they receive them—before reinvestment even occurs. A $500 dividend becomes $425 after tax, creating drag that isn’t easily recovered. The same $500 in a Roth IRA compounds completely tax-free, hitting the full 8% or higher by year five. The difference across the two accounts: roughly $800–$1,200 on a $1,500/month accumulation plan over five years.

Further wrinkle: most US brokers require a foreign dividend tax form (W-8BEN) to prove tax treaty eligibility. Delay or omission results in 30% withholding instead of 15%. Filing this form annually adds friction that passive index-fund investors never encounter. Additionally, Samsung’s ADR (American Depositary Receipt, ticker: SSNLF on Pink Sheets) is less liquid than direct share trading on Korean exchanges via eToro, Schwab, or Interactive Brokers; bid-ask spreads cost another 0.2–0.5% per purchase on small orders. These frictions compound to roughly 1–2% annual drag on taxable accounts—reducing the effective return from 8% to 6.5–7%.

Currency Headwinds: The Silent Return Killer

Here’s the disconfirming evidence: Samsung’s won’t deliver 8% if the Korean Won strengthens against the dollar over your five-year hold. From 2020 to mid-2024, the USD/KRW rate fluctuated between 1,050 and 1,350, with the strongest dollar period in 2022–2023. An investor who bought Samsung in 2020 at 1,200 KRW/USD benefited from the dollar’s strength; buying in 2024 at 1,200 with a weakening dollar ahead faces headwinds. A 10% Won appreciation (not uncommon in two-year cycles) reduces dollar-denominated returns by roughly 10%, flattening an 8% equity return to -2% in USD terms. No amount of dividend reinvestment fixes an unfavorable FX environment. This risk is often invisible to beginners who think only in USD and assume foreign stocks automatically diversify—they do, but they add currency volatility most US equity investors never experience.

| Product | Expense Ratio | Avg. Yield (2024) | 5Y Total Return (USD) | Tax Efficiency |

|---|---|---|---|---|

| Samsung Electronics (Direct, OTC) | N/A (direct stock) | 3.8% | ~45–65% (varies by entry) | Lower if held in taxable |

| iShares MSCI South Korea ETF (EWY) | 0.66% | 2.1% | ~32–48% | More tax-efficient than direct |

| Vanguard Dividend Appreciation ETF (VIG) | 0.06% | 2.2% | ~68–85% | Highest tax efficiency |

| Samsung ADR (Pink Sheets, SSNLF) | N/A (direct stock) | 3.5% | ~42–62% (includes spread costs) | Taxable drag higher |

Building the Account Structure for Maximum Compounding

The cleanest path to 8% is sequence-dependent: max out Roth IRA contributions ($7,000/year) first, then funnel $1,500/month into a Traditional 401(k) or similar employer plan, leaving only excess for taxable brokerage. This three-tier approach minimizes tax leakage and isolates currency risk to a smaller taxable sleeve. A hypothetical investor with access to both Roth and employer 401(k) could allocate roughly $8,400/year to tax-advantaged accounts and $9,600/year to taxable, reserving Samsung for the tax-sheltered tiers where the full 8% (or higher) accrues untouched until retirement. Brokers like Fidelity and Schwab support dividend reinvestment (DRIP) on most ADRs, automating the compounding—set it and ignore price fluctuations for five years. Interactive Brokers offers direct access to Korean Exchange listings (ticker: 005930.KS) with lower trading costs, though requiring more technical setup.

When 8% Falls Short: Drawdown Resilience and Rebalancing

Samsung’s stock is cyclical. During 2022, the entire semiconductor sector contracted 35–45% as rates rose and supply chains normalized. An investor hitting their 8% target needs to survive these drawdowns without selling. The psychological challenge is real: a $100,000 position falls to $65,000 in six months. Continuing to reinvest dividends at depressed prices—a practice called “averaging down”—is theoretically optimal but emotionally brutal. Many investors quit here, crystallizing losses and ending their five-year plan in year two. Historical data shows that staying invested through the 2022 sell-off and into 2023’s recovery would have returned to breakeven by late 2024, then surpassed the 8% target by 2025. Abandoning the strategy cost several percentage points of annualized return.

Rebalancing (which forces buying low, selling high) also challenges the 8% assumption. If Samsung doubles in price by year three and now comprises 40% of a small portfolio, rebalancing into more stable dividend stocks locks in gains but reduces future Samsung exposure. This is a feature, not a bug—it reduces concentration risk. However, it also means peak Samsung upside is capped. The 8% return assumes a buy-and-hold strategy; active rebalancing trades off max return for stability.

Frequently Asked Questions

Can I achieve 8% returns on Samsung alone, or should I diversify?

Eight percent from Samsung alone is possible but risky. Dividend yield alone (3.5%) requires 4.5% from price appreciation annually to hit 8%—a threshold Samsung doesn’t guarantee in down markets. Pairing Samsung (40–50% of a dividend portfolio) with higher-dividend payers like utilities or REITs reduces volatility and improves odds of hitting 8% across the portfolio, even if Samsung underperforms. Brokers like Fidelity make multi-position rebalancing simple via automatic dividend reinvestment across holdings.

Should I buy the ADR (OTC) or direct shares on Korean Exchange?

Direct shares on Korean Exchange (ticker: 005930.KS) via Interactive Brokers have lower trading costs (0.05–0.10% vs. 0.20–0.50% for OTC spreads) but require a local account and familiarity with won trading. For monthly $1,500 amounts, the ADR spread cost is roughly $3–7 per purchase—annoying but not deal-breaking if you’re in a Roth where annual turnover is low. The break-even point for direct exchange access is roughly $300,000+ in total position size; below that, ADR simplicity usually wins.

What happens if Samsung cuts its dividend during a recession?

Samsung has reduced payouts during downturns (notably 2020–2021 COVID adjustment, 2023 earnings contraction), though never eliminated it entirely. A 30% dividend cut would reduce the annualized return by roughly 1.2–1.5%, pushing 8% down to 6.5–6.8%. This is why concentration in a single stock is risky; a diversified dividend portfolio can absorb individual cuts without derailing long-term targets.

How much does the 15% dividend tax treaty actually cost me?

On $500 annual dividend income, 15% tax costs $75/year. Over five years with compounding, that drag totals roughly $400–$600 in foregone growth. In a Roth IRA, the same $500 compounds tax-free for five years to approximately $675 (at 7% growth), saving $75 immediately plus $175 in compound growth—a total $250 swing per $500 dividend between taxable and Roth. This underscores why maximizing tax-advantaged account space should take priority over stock picking.

What’s the biggest risk to hitting 8% returns?

Timing entry during a market peak and panic-selling during the inevitable correction. An investor who bought Samsung at $70 in 2022 (market enthusiasm, right before the chip downturn) faced a 35% drawdown to $45 within six months. Continuing to invest and holding through 2023 recovery would have worked fine, but most retail investors sold at $50–$55, locking in 20–30% losses and abandoning the strategy entirely. The math of 8% assumes human discipline; behavioral errors destroy it faster than market conditions.

The Bottom Line

Eight percent annual returns on Samsung Electronics is realistic but not inevitable. It requires the right account structure (maximize Roth and 401k), minimal tax drag, currency tailwinds or at least neutrality, and—most importantly—unwavering discipline through downturns. A five-year plan will encounter at least one 20–30% drawdown and one dividend cut; expecting smooth 8% every single year is fantasy. The investors who achieve this return do so because they set up automatic reinvestment, ignore short-term noise, and resist selling at the worst moments. Conversely, those who underperform typically sabotage themselves through emotional decisions or poor account placement, paying taxes that could have been deferred. The stock itself is sound; the human element is where most plans derail.