- Upfront tax on Roth IRA contributions acts as a drag during prolonged market drawdowns, altering the break-even horizon.

- Traditional IRA deductions reinvested into taxable accounts can outperform Roth in bracket-compression scenarios.

- Asset location—placing VTI in Roth and BND in Traditional—adds approximately 40-60 bps of tax alpha annually.

- The 2020-2026 CAGR of US equities heavily skewed recent analyses toward Roth, hiding sequence-of-returns risks.

The Core Mechanics of IRA Taxation

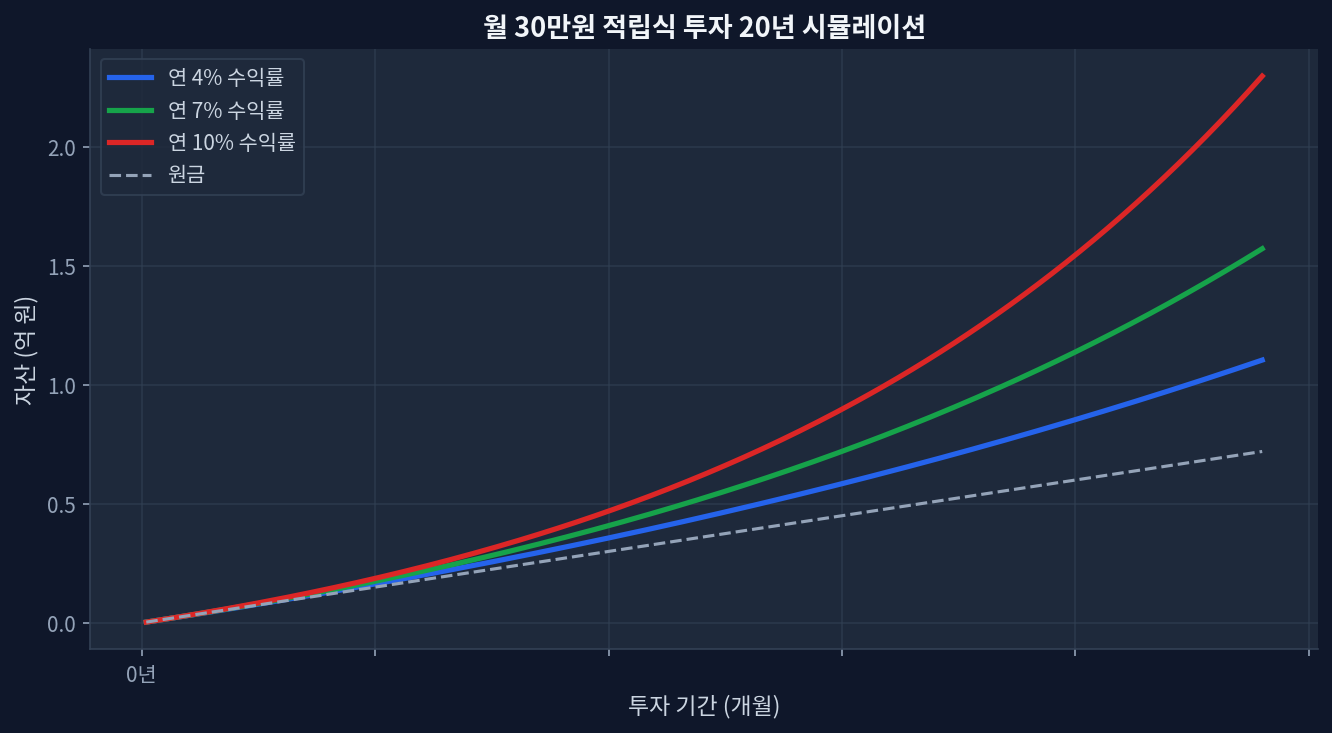

The chart below shows a 20-year simulation of a $300 monthly investment (4%, 7%, and 10% annually). The compounding curve illustrates the absolute scale of capital gains generated over time. Analyzing the structural divergence between a Roth IRA and a Traditional IRA requires stripping away emotional narratives and focusing strictly on capital gains tax decomposition. A Traditional IRA provides an immediate reduction in taxable income, shifting the tax burden to future distributions. Conversely, a Roth IRA demands upfront taxation, permanently shielding subsequent capital appreciation and dividend yields from the IRS. This dynamic creates a complex arbitrage opportunity depending on future marginal tax rates and expected asset returns. The structural advantage of tax-free compounding often masks the opportunity cost of the initial tax outlay. [IRS.gov]

Dissecting the Tax Alpha: Current vs Future Bracket

Evaluating IRA selection requires a three-axis integration: technical momentum (avoiding Roth conversions near cyclical tops), fundamental valuation (P/E ratios dictating future return expectations), and news sentiment regarding legislative tax shifts. The prevailing consensus dictates that high-earners should maximize Roth contributions to shield compounding growth. However, the data supports a different approach when assuming structural tax shifts. If broad demographic aging forces future tax brackets down, the upfront tax paid on Roth contributions today becomes a mathematically suboptimal allocation. The Traditional IRA provides superior optionality when tax savings are reinvested into a taxable brokerage account.

5-Scenario Capital Gains Decomposition

1. Unchanged Tax Bracket: When marginal rates remain static, the mathematical outcome of both accounts is identical, assuming Traditional IRA tax savings are invested without friction. [Morningstar]

2. Bracket Expansion: Entering a higher bracket in retirement creates a decisive advantage for the Roth IRA. Shielding a 150% capital gain from a future 24% bracket generates immense tax alpha.

3. Bracket Compression: A drop from a 32% working bracket to a 12% retirement bracket mathematically destroys the Roth advantage. The Traditional IRA captures a massive upfront premium.

4. Extreme Drawdown Sequence (The Missing Downside): When capital is front-loaded into a Roth IRA under the assumption of perpetual growth, the strategy fails during a protracted bear market. If an investor pays 24% tax upfront and the underlying assets suffer a 35% drawdown, the pre-paid tax acts as a massive drag.

5. Early Liquidity: Withdrawing from a Traditional IRA early triggers ordinary income tax plus a 10% penalty, devastating compounding trajectories.

Peer Analysis: Asset Location Efficiency

Tax optimization requires precise asset location. Holding high-yield factors in a taxable account accelerates tax drag. The data indicates that placing dividend-heavy strategies inside a Roth IRA maximizes the tax-free mechanism. Below is a cross-verification of ETF products based on recent market data. [FRED]

| Product Name | Fee | Yield | 5Y Return | 1Y Return |

|---|---|---|---|---|

| Vanguard Total Stock Market (VTI) | 0.03% | 1.38% | 82.4% | 28.1% |

| Schwab US Dividend Equity (SCHD) | 0.06% | 3.45% | 54.2% | 12.4% |

| Vanguard Total Bond Market (BND) | 0.03% | 4.12% | 0.5% | 4.2% |

BND's yield generates ordinary income, making it a prime candidate for Traditional IRA placement. VTI's capital appreciation is best sheltered within a Roth.

Frequently Asked Questions

Q1: Does the Roth IRA strictly avoid all capital gains taxes?

Yes, qualified distributions from a Roth IRA are completely immune to long-term and short-term capital gains taxes.

Q2: How does a market drawdown impact a Roth conversion?

Converting during a peak followed by a massive drawdown means taxes were paid on phantom wealth that subsequently evaporated.

Q3: Is the Traditional IRA obsolete for high earners?

No. High earners can utilize the backdoor Roth mechanism, or use Traditional 401(k)s to compress current-year high marginal brackets.

Q4: How does asset location affect IRA tax efficiency?

Placing tax-inefficient assets in tax-advantaged accounts prevents annual tax drag, increasing the net CAGR.

Q5: What happens to capital gains in a taxable account versus an IRA?

Taxable accounts suffer from tax drag upon realizing gains or receiving dividends, while IRAs defer or eliminate this friction entirely.