- The statutory filing window for Korean comprehensive income tax runs from May 1 through May 31 of the following year, with weekends and public holidays rolling to the next business day. In 2026, May 31 falls on a Sunday, so filing and payment continue through June 1.

- Retirement account tax credits apply up to KRW 9 million, or about $6,500, at 15% for total compensation below KRW 55 million and 12% above that line. An IRP contribution of KRW 8.4 million, or about $6,100, can therefore generate a tax credit of KRW 1.26 million or KRW 1.008 million.

- When annual interest plus dividends exceed KRW 20 million, or about $14,500, the comprehensive taxation switch turns on. For US-listed ETFs such as VOO, SCHD, and DGRO, the account wrapper matters more than the ticker label.

- Failure-to-file penalties are 20%, underreporting penalties are 10%, and late-payment interest runs at 0.022% per day. Delay carries a measurable cost.

- Rolling ISA maturity proceeds into a retirement account can add 10% of the converted amount, up to KRW 3 million, or about $2,200, to retirement-account contribution creditable amounts.

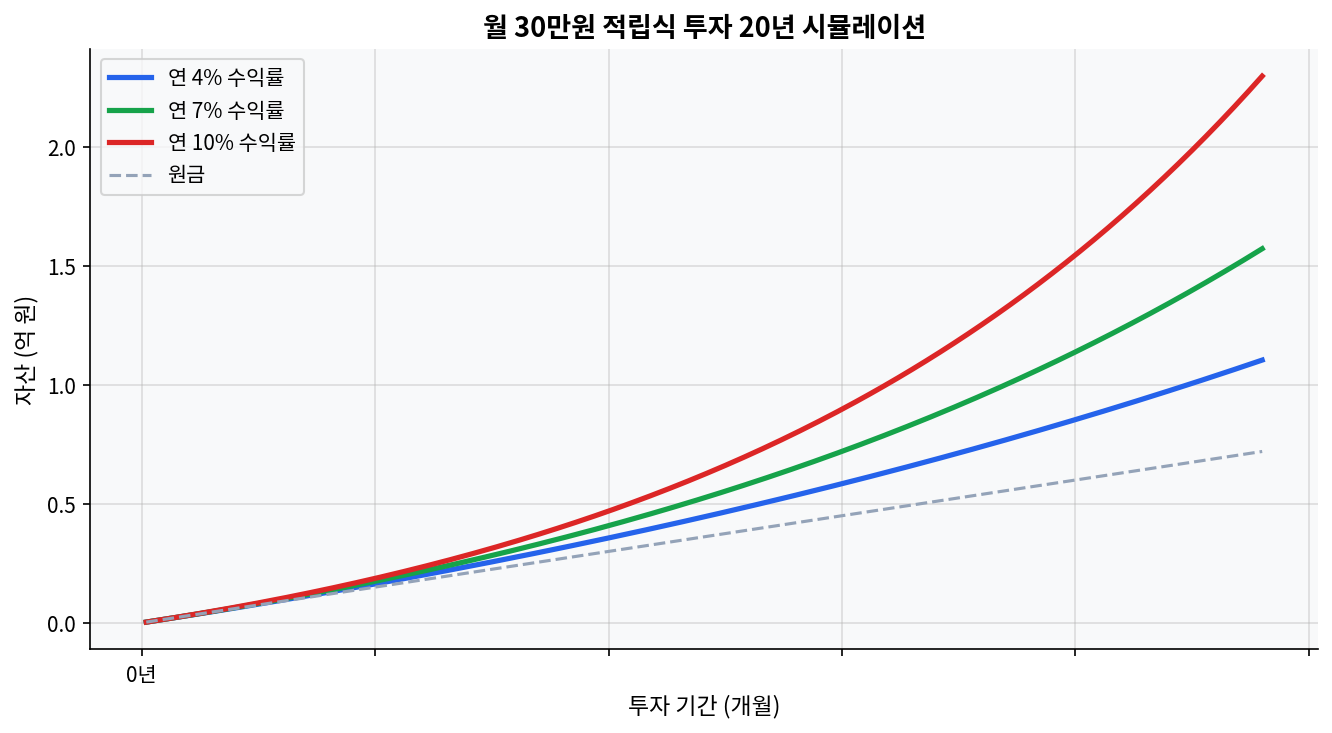

What the chart says first

The chart below shows how wide the gap becomes after 20 years when a $220 monthly contribution compounds at 4%, 7%, and 10%. In this range, compounding and contribution duration create larger numbers than tax optimization alone. Saving about $75 in tax may matter less than keeping the contribution schedule alive for one more year.

Under Korea’s National Tax Service framework, comprehensive income is the sum of interest, dividends, business income, wages, pension income, and other income. That is why VOO, SCHD, SPY, and other dividend or broad-market ETFs may look different on a broker screen but still land in the same filing logic once the income is aggregated.

The threshold that separates filers

Comprehensive income tax gets much harder the moment different income types are mixed together. A taxpayer with only wage income and a clean year-end settlement may face a simple May filing. Once foreign ETF dividends, domestic dividends, freelance income, rental income, or pension income are added, the number of filing checkpoints rises quickly. The filing and payment deadline is May 1 through May 31 of the following year, while taxpayers subject to the certified tax audit report file through June 30.

Missing the deadline triggers penalties.

Saturday or public holiday deadlines move to the next business day.

In 2026, May 31 falls on a Sunday, so the effective deadline moves to June 1.

Local income tax follows the same filing flow. Finishing the national tax filing first and then moving to the local tax portal is usually the least confusing route. When the workflow is split across systems, omissions tend to happen before refunds do.

Why the KRW 20 million dividend threshold matters

The moment annual interest and dividends exceed KRW 20 million, the tax structure changes. At that point, the comprehensive taxation question matters more than the headline yield of the product. The market often treats dividend ETFs as pure cash-flow assets, but from a comprehensive-income-tax perspective, the larger the dividend stack, the greater the chance of a rate jump.

Starting in 2026, a separate taxation regime for high-dividend corporate income was introduced. The election applies only from the 2027 filing season through the 2030 filing season. Market consensus still leans toward US dividend ETFs as the default tax answer, but Korean high-dividend equities can become more competitive after tax in certain brackets. This analysis can miss if the company does not satisfy the special regime tests or if dividend income stays well below KRW 20 million.

The real tax lever is account structure

The most practical way to reduce comprehensive income tax is account ordering, not product selection. A retirement savings account, IRP, ISA, and taxable brokerage account can produce similar-looking pre-tax results, but the after-tax math is different. Retirement accounts create an immediate tax-credit effect. ISA maturity rollovers can create an additional contribution credit. Taxable accounts, by contrast, feed dividends and interest directly into the financial-income aggregate, which makes threshold management harder.

| Vehicle | Core number | Comprehensive-income-tax angle | Watch point |

|---|---|---|---|

| Retirement savings account | Tax-credit base up to KRW 6 million, at 15% or 12% | The refund effect is immediate and easy to see | Early withdrawal can reverse the after-tax advantage |

| IRP | Combined retirement-account cap of KRW 9 million, at 15% or 12% | Strong impact in both year-end settlement and annual filing | Withdrawal restrictions are tight |

| ISA brokerage account | 10% of maturity rollover amount, up to KRW 3 million extra counted | Creates a tax-efficient redeployment path for maturity cash | Maturity timing and rollover timing must be managed |

| Taxable brokerage account | No tax credit | Direct exposure to the KRW 20 million interest and dividend threshold | Reporting omissions and threshold jumps become more likely |

Retirement-account tax credits apply up to KRW 9 million, or about $6,500, at 15% for total compensation below KRW 55 million and 12% above that line. The math is simple. If annual compensation is below KRW 55 million, an IRP contribution of KRW 8.4 million produces a tax credit of KRW 1.26 million. Above that line, the same contribution produces KRW 1.008 million. The same money has a different refund effect depending on income band.

The ISA is not a magic way to erase filing. It is a tool that reduces friction before filing. When part of the maturity proceeds is transferred into a retirement account, 10% of that amount is added to creditable retirement-account contributions. That is especially useful in the pre-retirement cash-flow transition window. If retirement savings account and IRP limits are already full, the incremental benefit is smaller.

The year-end settlement correction window

Medical expenses, donations, retirement-account contributions, and certain insurance premiums that were missed in year-end settlement can be corrected during the May comprehensive income tax filing. That matters more than many taxpayers realize. Year-end settlement is often treated as a final stop, but May functions as a correction window. Taxes are resolved by records, not by sentiment. Dividend statements, interest statements, retirement contribution certificates, and withholding records belong in one folder for the lowest-cost compliance habit.

Numbers make it clearer

At KRW 700,000 per month, the annual contribution is KRW 8.4 million, or about $6,100. Placing that amount in an IRP creates a direct cash benefit of KRW 1.008 million to KRW 1.26 million through the tax credit alone. By contrast, leaving the same KRW 8.4 million in a taxable account and using it to scale dividends increases the chance of moving closer to the KRW 20 million threshold. A high dividend rate is not automatically better; on an after-tax basis, it can trigger the tax switch earlier.

A new variable after 2026 is the separate taxation regime for high-dividend corporations. The market narrative still tends to treat US dividend ETFs as the default tax answer, but local high-dividend names can improve the after-tax profile when the special rules apply. The data supports that view, but shifting one assumption changes the read entirely: if the company fails the special regime tests or the dividend stack stays far below KRW 20 million, the old comprehensive-tax logic remains intact.

During drawdowns, broad-market peers such as VOO and SPY usually move together, while dividend-focused peers like SCHD and DGRO may soften only at the margin. That difference matters for portfolio behavior, but it does not erase filing friction once the account is taxable.

Mistakes and risks

The most common mistake is checking foreign ETF dividends only once on the broker screen and treating that as the full picture. Foreign withholding, domestic withholding, and dividend posting dates are split across systems, which makes omissions easy. Another mistake is assuming that filling the retirement-account bucket solves everything. Retirement savings accounts and IRP are powerful, but they do not clean up financial income, rental income, or other taxable items by themselves.

Failure-to-file penalties are 20%.

Underreporting penalties are 10%.

Late-payment interest is 0.022% per day.

Improper methods can push penalties higher.

Scenarios where this analysis could miss are clear. If the combined dividend and interest total stays well below KRW 20 million, retirement-savings and IRP limits are already full, and ISA maturity is still far away, then a simpler compliance approach is better than elaborate tax optimization. Once business income or rental income is added, the structure changes sharply.

Bottom Line

The data supports a simple order: fund the IRP up to the limit first, use the ISA rollover credit when it becomes available, and keep taxable-account interest and dividends under the KRW 20 million threshold when possible. That diverges from the common market narrative that the highest-yield ticker is always the best answer. Account wrapper and filing friction matter more than product branding. When financial income is small and deduction limits are already used up, accurate filing is the priority. This is educational information, not investment advice.

Frequently Asked Questions

When is the comprehensive income tax filing deadline?

The filing window runs from May 1 through May 31 of the following year. Taxpayers subject to the certified tax audit report file through June 30, and weekends or public holidays move the deadline to the next business day.

Are foreign ETF dividends included in comprehensive income tax?

Interest and dividends are aggregated as financial income. Once the annual total exceeds KRW 20 million, the comprehensive taxation question matters. US-listed ETFs such as VOO and SCHD are not exceptions.

What is the IRP tax-credit limit?

For total compensation below KRW 55 million, the combined retirement-account credit base is up to KRW 9 million at 15%. Above that line, the rate falls to 12%. IRP is part of that same framework.

What happens if financial income exceeds KRW 20 million?

Once the combined total of interest and dividends crosses KRW 20 million, comprehensive taxation risk rises. After-tax results are driven more by tax rates and account structure than by the product’s gross yield.

What penalties apply if filing is missed?

General failure-to-file penalties are 20%, underreporting penalties are 10%, and late-payment interest is 0.022% per day. Small delays can become expensive once they compound.

Official references: National Tax Service comprehensive income tax filing deadline, National Tax Service penalties, National Tax Service retirement-account tax credit, National Tax Service financial income guide, National Tax Service high-dividend separate taxation notice, and National Tax Service filing guide.

This content is for educational purposes only and is not an investment recommendation.

This post is for informational purposes only and does not constitute investment advice.