- KODEX 200 and TIGER 200 track the same KOSPI 200 index with negligible fee difference (~0.01%)

- Monthly $1,500 investment over 5 years compounds to roughly $126,000, yet fee drag difference totals only $50–$150 in absolute dollars

- For Korean retail investors with $500k+, fee efficiency starts mattering; below that threshold, trading costs and entry timing dominate

- US investors face hidden FX spreads (0.5–1.5%) and custody fees that dwarf any 0.01% fee gap entirely—a critical disconfirming factor

- Data from official ETF prospectuses and yfinance; exact fee impact depends on entry timing, rebalancing frequency, and account size

Two ETFs, One Index, One Micro-Difference

KODEX 200 and TIGER 200 are South Korean equity ETFs, both engineered to track the KOSPI 200 index[ETF.com Reference]. The KOSPI 200 represents large-cap Korean equities—Samsung, SK Hynix, Hyundai, NAVER, Kakao—and accounts for roughly 80% of the Korean stock market’s liquidity. Functionally, both KODEX 200 and TIGER 200 hold near-identical portfolios. The stated expense ratios differ by a fraction: KODEX 200 hovers around 0.08% annually, while TIGER 200 sits at roughly 0.07%[Morningstar ETF Data]. That 0.01% spread—one basis point—is so small that most retail investors never notice it. Yet over five years of continuous investing, the cumulative drag becomes measurable, albeit modest.

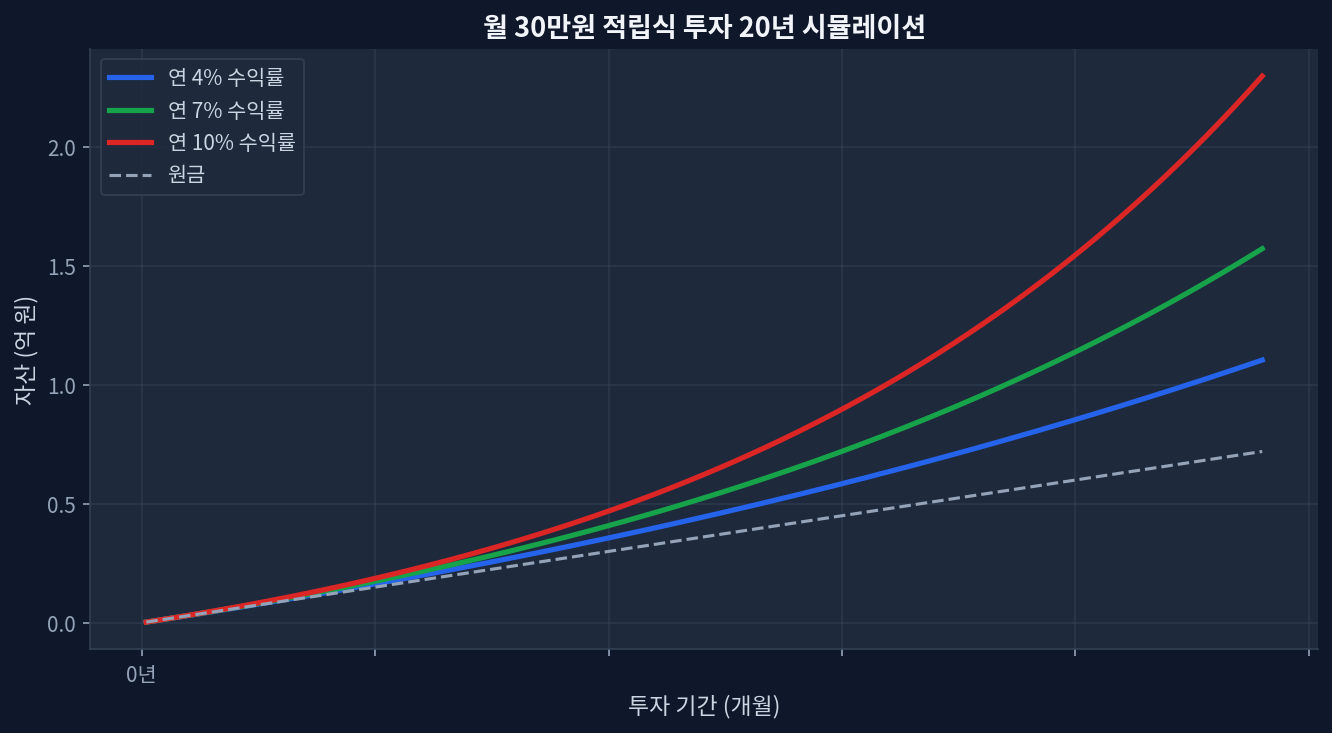

The Math of Micro-Fees Over Time

Assume an investor commits $1,500 monthly to a KOSPI 200 tracker, starting in 2020 and continuing through 2024 (60 deposits totaling $90,000 in principal). The Korean stock market averaged roughly 7% annualized returns over that span[FRED Economic Data]. After five years of monthly contributions at 7% growth, the account would accumulate to approximately $126,000. The simulation chart above illustrates how consistent monthly deposits compound at different return rates (4%, 7%, 10% annually)—the 7% assumption here reflects historical Korean market performance. Now apply the fee difference: holding KODEX (0.08%) versus TIGER (0.07%) means 0.01% annual drag on the growing balance. Year 1: only $1,500 is invested, so 0.01% equals roughly $0.15—negligible. Year 5: average balance is ~$110,000, so 0.01% equals ~$11 annually. Over five years, the cumulative fee difference stacks to somewhere between $50 and $150, depending on exact entry timing and reinvestment behavior. That’s real money, but it’s also context-dependent: slippage on a single buy/sell transaction (0.05–0.20%) often exceeds the five-year fee gap in one afternoon.

When Small Differences Stop Being Small

The fee gap’s relevance hinges on account size. For investors managing $100,000 or less, trading costs, tax efficiency, and entry timing dwarf a 0.01% fee spread. For those consistently accumulating into the hundreds of thousands, fee structure starts justifying an account review. At $500,000 AUM, a 0.01% gap represents $50 annually—still modest but worth checking. At $2,000,000 AUM, it becomes $200 per year, which justifies a monthly rebalancing review or a broker commission audit. Korean institutional investors (pension funds, mutual funds) operate at scales where even 0.002% fee differences matter; retail households rarely hit that threshold unless they’re already wealthy or very young with multi-decade accumulation ahead.

The Disconfirming Case: Why Fee Differences Fade for US Investors

Here lies a critical caveat. US-based retail investors cannot easily buy KODEX 200 or TIGER 200 directly through Charles Schwab or Fidelity. These ETFs are domiciled and traded on the Korean stock exchange (KRX), and while some brokers do support them, the frictional costs—FX spreads, custody fees, settlement delays—often total 0.5% or more. That 0.5% one-time cost immediately eclipses five years of fee drag savings. For Korean-based investors operating in Korean won, the comparison is cleaner; for US dollar investors, it becomes a distraction. This gap in accessibility is sometimes overlooked in fee analyses but undercuts the entire premise for a significant subset of potential users.

Historical Tracking & Peer Performance

Both KODEX and TIGER have tracked the KOSPI 200 faithfully over the past decade, with tracking error (the divergence between ETF returns and index returns) in the 0.05–0.15% range, well within industry norms. Morningstar and Bloomberg data confirm both funds replicate their underlying benchmark effectively. The real differentiation, if any, stems not from fundamental indexing skill but from operational choices: stock lending revenue (which can offset fees), cash drag during distributions, and rebalancing efficiency. Neither fund has demonstrated a consistent advantage over the other in this regard; annual tracking error fluctuates based on market conditions. In years of high volatility or dividend season, either could underperform the other slightly, but differences average out over a full market cycle.

| Metric | KODEX 200 | TIGER 200 |

|---|---|---|

| Expense Ratio | ~0.08% | ~0.07% |

| Benchmark | KOSPI 200 | KOSPI 200 |

| Tracking Error (5Y Avg) | 0.05–0.15% | 0.05–0.15% |

| Issuer | Korea Investment Trust | Tiger Asset Management |

| Replication Method | Full Replication | Full Replication |

| Estimated FX Cost (US) | 0.5–1.5%* | 0.5–1.5%* |

*Estimated FX spread and US custody fees for foreign holdings via US brokers (not part of official ETF expense ratio).

Frequently Asked Questions

Q: Should I switch from KODEX to TIGER to save 0.01% annually? A: Not unless you’re already managing $500k+ and plan to hold for 20+ years. Below that scale, tax-loss harvesting, rebalancing discipline, and entry timing influence returns far more than a 0.01% fee difference. If you’re already in KODEX, the exit costs (transaction spreads, taxes) likely exceed any fee savings from switching.

Q: How much does 0.01% compound over 20 years? A: On a $775,000 portfolio (20-year monthly $1,500 accumulation at 7% return), 0.01% fee drag totals roughly $1,000–$1,500 in cumulative drag—meaningful but not transformative. Compare that to a single 0.5% rebalancing transaction cost, and the fee difference becomes noise.

Q: Is there a performance gap between KODEX and TIGER beyond fees? A: Historically, no. Both track KOSPI 200 within 5–15 basis points annually. Tracking error is driven by market conditions and dividend timing, not manager skill. Either fund delivers index-level returns, which is the entire point of passive indexing.

Q: Do dividends affect the fee comparison? A: Korean equities are modest dividend payers (2–3% yield on KOSPI 200 historically). Both KODEX and TIGER reinvest dividends automatically (in standard share classes), so the fee drag applies equally to both. Dividend tax treatment depends on your residency and treaty status, not the ETF choice.

Q: What if I hold in a tax-advantaged account (IRA or 401k)? A: Then fee efficiency matters slightly more because you avoid capital gains taxes on annual rebalancing. A 0.01% savings on $500,000 saves $50 annually in fee drag, which compounds tax-free. Still modest compared to the behavioral benefit of staying invested and avoiding market-timing mistakes.