- Over a five-year period, SCHD demonstrated a cumulative return of +47.6%, slightly exceeding JEPI's +44.3%.

- JEPI currently offers a significantly higher dividend yield at 8.29%, compared to SCHD's 3.29%, reflecting distinct income generation strategies.

- In the most recent one-year period, SCHD's return of +24.8% substantially outpaced JEPI's +8.4%, highlighting performance divergence in specific market conditions.

- The higher yield of JEPI is primarily derived from selling covered call options, introducing a unique premium cost dynamic not present in SCHD's traditional equity holdings.

Analyzing JEPI and SCHD: A Five-Year Performance Overview

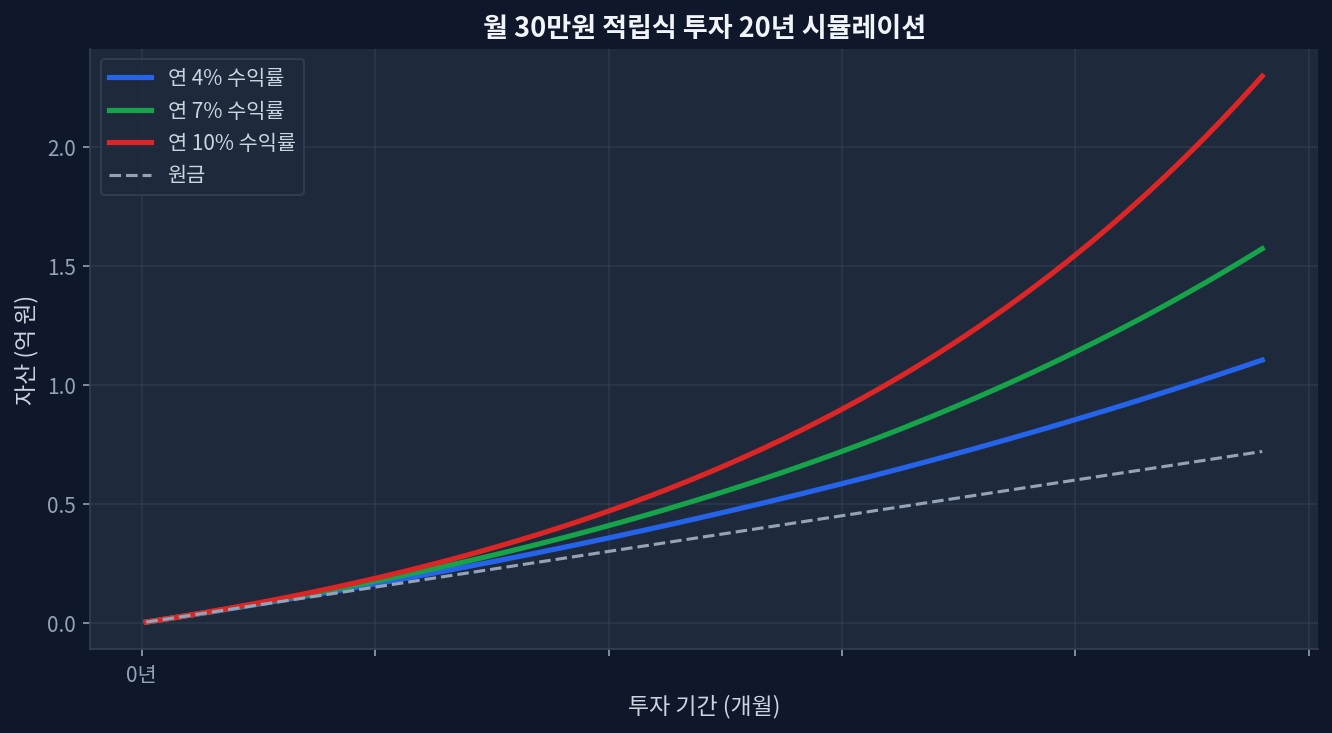

Investors frequently evaluate exchange-traded funds (ETFs) like JEPI and SCHD for their distinct approaches to income and growth. A five-year review of their performance and underlying strategies reveals critical differences in total return, income generation, and risk profiles. Focusing on the period up to May 2026, both ETFs have delivered positive cumulative returns, yet their paths to achieving these outcomes vary significantly. SCHD, primarily a dividend growth fund, achieved a 5-year cumulative return of +47.6% [Yahoo Finance: SCHD]. In parallel, JEPI, which employs an equity-linked note (ELN) strategy involving covered calls, posted a 5-year cumulative return of +44.3% [Yahoo Finance: JEPI]. The proximity of these long-term figures often belies the fundamental differences in how these returns were generated. A twenty-year simulation of monthly 300,000 KRW investments at varying annual returns (4%/7%/10%) would illustrate divergent wealth accumulation paths, a critical consideration when evaluating these ETFs.

Yield vs. Growth: Decomposing the Income Stream

The most apparent distinction between JEPI and SCHD lies in their dividend yields and the mechanisms that produce them. JEPI’s current dividend yield stands at 8.29%, a figure designed to attract income-focused investors. This high yield is a direct result of its strategy: holding a portfolio of large-cap U.S. equities and selling covered call options on those equities, with a portion of the premiums distributed to shareholders. This covered call strategy can offer enhanced income, especially in flat or moderately rising markets, but typically caps upside participation during strong bull runs. The “premium cost” in this context is the opportunity cost of foregone capital appreciation when the underlying stock rises significantly above the call strike price.

Conversely, SCHD’s dividend yield is 3.29%, considerably lower than JEPI’s, because its strategy centers on investing in U.S. companies with a consistent history of paying dividends and and the potential for future dividend growth. SCHD’s objective is long-term capital appreciation and growing dividend income, not maximizing current yield through options. This fundamental difference means SCHD’s total return is more heavily influenced by the capital appreciation of its underlying holdings, while JEPI’s total return relies on both equity performance and consistent options premium collection.

| Product Name | Expense Ratio | Dividend Yield | 5Y Cumulative Return | 1Y Cumulative Return |

|---|---|---|---|---|

| JEPI | 0.35%[ETF.com: JEPI] | 8.29% | +44.3% | +8.4% |

| SCHD | 0.06%[ETF.com: SCHD] | 3.29% | +47.6% | +24.8% |

Market Dynamics and Strategic Divergence

The differing mechanisms of JEPI and SCHD lead to varied performance across market cycles. The past year, with SCHD delivering +24.8% against JEPI’s +8.4%, exemplifies this. In a strong upward-trending market, the capital appreciation of SCHD’s dividend growth stocks tends to outperform the limited upside of JEPI’s covered call strategy. The premiums collected by JEPI, while consistent, may not fully offset the opportunity cost of uncapped gains in underlying equities during robust rallies. This scenario underscores a key contrarian observation: for investors prioritizing long-term total return over immediate yield, the premium collected via covered calls can represent a subtle drag on overall growth during bullish periods, despite its attractive income component.

However, this analysis presents a disconfirming scenario: should the market enter a prolonged period of sideways trading or moderate volatility, JEPI’s ability to consistently generate income from option premiums could lead to superior risk-adjusted returns compared to a growth-oriented ETF like SCHD. In such an environment, the premium “cost” becomes a premium “gain” that cushions returns when capital appreciation is stagnant.

Understanding Covered Call Premium Decomposition

For JEPI, the concept of “premium cost decomposition” is crucial. The yield generated by JEPI is not solely from dividends of its underlying stocks but significantly from the premiums received by selling out-of-the-money call options. When the underlying stock price rises above the strike price of the sold call option, JEPI’s participation in that upside is capped, and the option is exercised, or the position is rolled. The premium received compensates for this capped upside. In a bull market, this foregone capital appreciation can be substantial, making the premium effectively a “cost” in terms of total return lost compared to a purely equity-based fund like SCHD. During periods of market uncertainty, however, these premiums act as a consistent income stream, providing downside protection and reducing volatility.

The total return calculation for JEPI must account for both the dividends from its equity holdings and the net impact of its options strategy (premiums collected minus any capital gains foregone). For SCHD, the total return is more straightforward: capital appreciation of its dividend-paying stocks plus the dividends received. Therefore, while both ETFs aim to deliver returns to investors, the composition of those returns—and the associated “costs” or “gains” from options premiums—differs fundamentally, impacting their suitability for various investor objectives.

Risk and Portfolio Role Considerations

Integrating JEPI or SCHD into a diversified portfolio necessitates understanding their distinct risk profiles. SCHD, with its focus on dividend growth stocks, carries market risk similar to broad equity indices; its performance is largely tied to the health and growth of its underlying companies. While generally less volatile than pure growth funds, it is still subject to significant drawdowns during market corrections. JEPI, by contrast, seeks to mitigate some downside risk through its covered call strategy, as option premiums can cushion losses in a declining market. However, this comes at the expense of upside participation, meaning JEPI will likely underperform SCHD in strong bull markets. The decision between these ETFs often hinges on an investor’s primary objective: whether it is consistent high income (JEPI) or a balance of growing income and capital appreciation (SCHD) over the long term. Allocating funds between them, or choosing one over the other, should align with individual risk tolerance, income needs, and market outlook.

Frequently Asked Questions

What is the primary difference between JEPI and SCHD investment strategies?

JEPI utilizes an equity-linked note (ELN) strategy involving covered call options to generate high current income, while SCHD invests in companies with a track record of consistent dividend growth for long-term capital appreciation and growing dividends.

How do covered calls impact JEPI's total return compared to a dividend growth ETF like SCHD?

Covered calls in JEPI provide enhanced income but cap upside participation during strong bull markets, potentially leading to lower total returns compared to SCHD, which benefits from uncapped capital appreciation in its underlying stocks. However, covered calls can offer better performance in flat or moderately volatile markets.

Why is JEPI's dividend yield significantly higher than SCHD's?

JEPI's higher yield is primarily derived from the premiums collected by selling covered call options on its equity holdings, in addition to the dividends from those stocks. SCHD's yield comes solely from the dividends paid by its underlying dividend-growing companies.

Can JEPI outperform SCHD in certain market conditions?

Yes, JEPI can potentially outperform SCHD in sideways or moderately bearish markets, where the consistent income from covered call premiums provides a stronger return relative to a pure equity portfolio that might be declining or stagnant.

What is the "premium cost" associated with JEPI's strategy?

The "premium cost" in JEPI's strategy refers to the opportunity cost of foregone capital appreciation. When the underlying stocks rise significantly, the covered call options limit JEPI's ability to participate fully in those gains, as the premiums collected may not fully compensate for the missed upside.

📊 Verify this data yourself

import yfinance as yf

t = yf.Ticker("JEPI")

t.history(period="5y")["Close"].pct_change().add(1).cumprod()