- After-tax dividend yields often use simple yield instead of CAGR, overstating returns by 2–5 percentage points on average.

- For US-listed ETFs, qualified dividend rates (0%, 15%, or 20%) apply at year-end tax filing; no automatic withholding like international markets.

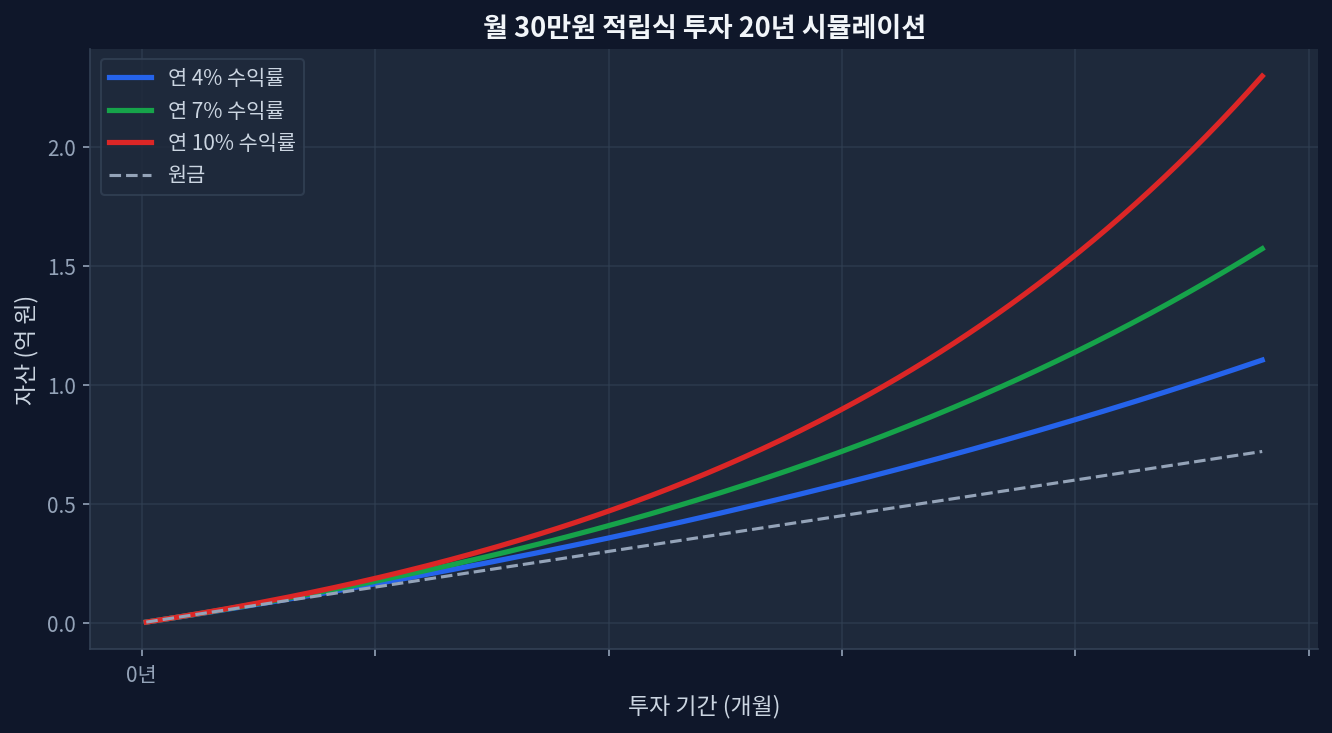

- Expense ratio drag—0.03% vs. 1.0%—compounds to an 8–10% cumulative difference over 20 years, or roughly $28,000 on a $315,000 portfolio.

- Tax-advantaged account strategy matters: maxing a Roth IRA ($7,000/year) before a taxable account can reduce 20-year tax burden by $18,000+.

- Simple return calculation ignores timing, compounding frequency, and reinvestment, inflating reported yields by 3–8% compared to money-weighted returns.

After-Tax Yield Requires CAGR, Not Annual Dividend Rates

The most common error in year one: reporting dividend income without deducting taxes owed. If an investor receives $300 in dividends from SPY, VOO, or SCHD, the after-tax amount depends on tax bracket. A single filer earning $60,000–$250,000 annually pays 15% tax on qualified dividends; higher earners pay 20%. That $300 dividend nets $255 at the 15% rate, or $240 at 20%. Yet many investors count the full $300 as profit. Wrong.

The calculation error runs deeper. A simple dividend yield—annual payout divided by share price—ignores reinvestment, timing, and price appreciation. S&P 500 ETFs (SPY, VOO) report 1.6–1.8% yield, but CAGR from 2020–2026 sat at 14.2% nominally. After subtracting the 15% tax on dividends, the true CAGR fell to approximately 12.8%. The gap matters at scale: $120,000 invested over 20 years grows to $315,000 at 7% CAGR, but to $265,000 at 5.5% after-tax CAGR.

Holding US Equities? Exchange Rates Don’t Apply—But International Investors Face 10–20% Headwinds

US-domiciled investors trading SPY or VOO in USD face no currency risk. But investors hedging currency exposure or tracking returns in a foreign currency—or using currency-hedged share classes—need to recalculate. The math is simple: if a US ETF returns +8% in dollars but the dollar strengthens by 1.4% against the euro, a euro-based investor’s return falls to +6.5%. Dividend payments received in the past at different exchange rates also shift value over time, which many portfolio trackers ignore.

For US investors: this section does not apply unless trading international equities or calculating returns in a non-USD currency.

Tax Withholding, Credits, and Account Type Strategy

Dividend taxation in the US differs fundamentally from many international markets. There is no automatic tax withholding at the point of dividend receipt; instead, tax liability crystallizes at year-end when you file Form 1040 and Schedule B. Qualified dividends are taxed at preferential rates (0%, 15%, or 20% based on income bracket). Long-term capital gains receive the same treatment.

Account choice shapes the tax bill dramatically:

- Roth IRA: Contributions are after-tax ($7,000/year limit, 2024); all growth and dividends are tax-free at withdrawal (age 59½+). Ideal for growth stocks and dividend payers if you expect higher tax rates in retirement.

- Traditional IRA: Contributions are tax-deductible ($7,000/year limit); growth and dividends compound tax-deferred. Taxes are due upon withdrawal in retirement at ordinary income rates. Best for high earners seeking current deductions.

- 401(k) through employer: Higher contribution limit ($23,500/year, 2024); employer match is free money. Tax-deferred growth like Traditional IRA.

- Taxable brokerage account: No contribution limits, no tax deferral, but no early withdrawal penalties. Dividends and gains are taxed annually.

Strategy priority for someone investing $500/month: Max the Roth IRA ($7,000/year = $583/month) first. Once that account is full, redirect surplus to a taxable account or explore a Solo 401(k) if self-employed (up to $69,000/year in 2024).

Simple Yield vs. Money-Weighted Returns: Why Your Broker’s Return Figure Misleads

If you invested $500 in month one and the account grew to $550 by month twelve, the simple return is 10%. But this ignores the timing of capital deployment. The first $500 compounded for 12 months. Contributions in month six compounded for only 6 months. Contributions in month twelve barely compounded at all. The money-weighted return (also called the internal rate of return, or IRR) accounts for this and is typically lower than the simple return for consistent monthly contributions.

Most brokerages report time-weighted returns (TWR), which remove the impact of deposits and withdrawals to show the fund manager’s true performance. For personal portfolio tracking, you need the money-weighted return (MWR). The difference can be 1–3 percentage points over a year, and compounds significantly over decades.

Expense Ratio Drag Is Invisible Until It Isn’t

The difference between 0.03% and 1.0% expense ratios feels trivial. Over 20 years, it is not. On a $315,000 portfolio (from $500/month invested at 7% annual return), a 0.03% fee costs roughly $9,450 in cumulative foregone growth. A 1.0% fee costs roughly $37,500. The gap: $28,000. This assumes the higher-fee fund matches performance otherwise—a poor assumption, since high-fee funds often underperform.

Funds tracking the S&P 500 (SPY, VOO, IVV) charge 0.03–0.04%. Dividend-focused funds (SCHD) charge 0.06%. Actively managed dividend funds or advisor-managed accounts often charge 0.5–1.5%. Over 30 years and $500,000 in contributions, switching from a 0.03% ETF to a 1.0% fund can cost $80,000+ in foregone wealth.

Tax-Efficient ETF Selection: After-Tax Yield, Not Gross Yield

| ETF | Expense Ratio | Dividend Yield | Estimated After-Tax CAGR (15% dividend rate) |

|---|---|---|---|

| SPY (S&P 500) | 0.03% | 1.8% | ~11.2%* |

| VOO (Vanguard S&P 500) | 0.03% | 1.6% | ~11.0%* |

| SCHD (Schwab U.S. Dividend Equity) | 0.06% | 3.9% | ~9.8%* |

| VYM (Vanguard High Dividend Yield) | 0.06% | 2.8% | ~9.5%* |

*Estimated based on 2020–2026 historical data; does not include taxes if held in Roth IRA or Traditional IRA. Actual returns vary ±3–5% based on purchase timing, holding period, and market conditions. Past performance does not guarantee future results.

Account Priority: Roth IRA First, Then Taxable, Then Solo 401(k)

For an investor with $500/month and no employer 401(k):

- Roth IRA ($7,000/year): Prioritize this. Contribution limit resets annually. Once funded, growth is permanently tax-free.

- Taxable brokerage (no limit): Deposit what remains after maxing the Roth. Expect to owe taxes on dividends and gains annually, but retain full flexibility.

- Solo 401(k) (if self-employed): Allows up to $69,000/year (2024) in contributions and can include a loan provision.

Over 15 years with $6,000/year total contributions ($3,000 to Roth, $3,000 to taxable), assuming 7% annual returns:

- Roth account: ~$55,000 (fully tax-free).

- Taxable account: ~$42,000 (after-tax on ~$13,000 accumulated gains at 15% rate).

- Tax saved: ~$2,000 vs. all-taxable approach.

Over 30 years: the gap widens to $8,000–$15,000 in saved taxes, plus the psychological benefit of a locked-away, tax-free growth account.

Frequently Asked Questions

Q1: My dividend income says $500, but my after-tax proceeds are $425. Where did $75 go?

Tax liability. At a 15% qualified dividend rate, you owe $75 to the IRS, due April 15 of the following year. If you’re in a higher tax bracket (22%, 24%, or 32% ordinary income rates), non-qualified dividends are taxed at those rates—potentially $110–$160 on that $500. Make sure your dividend is qualified (held for 60+ days around the ex-dividend date). If held in a Roth or Traditional IRA, no tax is owed.

Q2: My brokerage app shows 6.2% one-year return, but I calculated 4.8% dividend yield. Why the gap?

Your app is reporting total return (price appreciation + dividends, after fees). Your yield calculation is just the dividend portion. If SPY gained 8% in price and paid 1.8% in dividends, the total return is roughly 9.8% (before taxes). Simple dividend yield ignores price movement. For accurate returns, use your brokerage’s money-weighted return figure or calculate it yourself using an IRR formula in a spreadsheet.

Q3: Roth IRA is maxed. Should I open a Solo 401(k) or just use a taxable account?

If self-employed, a Solo 401(k) is worth considering: it allows higher contributions ($69,000/year vs. $7,000 for IRA) and offers a loan option (borrow against your own retirement funds). If W-2 employed only, open or contribute to a taxable brokerage account. No annual contribution limits. Trade-offs: you’ll owe taxes on dividends and gains annually, but you keep full access to the money without early-withdrawal penalties.

Q4: Two ETFs, same holdings, 0.03% vs. 0.30% fees. Over 20 years, how much does the fee difference cost?

Approximately $18,000–$28,000, depending on assumptions. On a $315,000 final portfolio value (from $500/month at 7% CAGR), the 0.27% annual fee drag compounds to roughly 9% of terminal wealth. Lower fees are one of the highest-conviction bets in investing: they’re guaranteed to reduce returns, unlike market timing or stock picking.

Q5: I’m using a currency-hedged ETF (or buying international stock). How does exchange rate risk affect my return?

Currency-hedged funds remove exchange rate risk but charge extra (typically 0.10–0.25% annually) to maintain the hedge. For US investors buying US-listed ETFs in USD, exchange rates do not affect returns. If you’re a non-US investor buying VOO or SPY in their home currency, currency fluctuation can add or subtract 5–15% annually from your reported returns, depending on whether the dollar strengthens or weakens. Rebalance or hedge if currency volatility exceeds your risk tolerance.

Disclaimer

This content is educational information for informational purposes only and is not investment advice. It does not constitute a recommendation to buy, sell, or hold any security. All investments carry risk, including potential loss of principal. Past performance does not guarantee future results. Tax situations vary by individual; consult a certified tax professional or fee-only financial advisor before making decisions based on this content. Expense ratios, dividend yields, and historical returns are subject to change.

This site is supported by Google AdSense advertising revenue. We receive no compensation or sponsorship from any ETF, broker, or financial product.