- Brokerage commissions: All major US brokers (Fidelity, Charles Schwab, TD Ameritrade) now charge $0 per ETF trade; the real cost is bid-ask spreads at 0.01%–0.05% depending on liquidity

- Bid-ask spreads underestimated: On $500 monthly investments over 5 years, cumulative spread costs range from $75–$375 depending on broker and ETF — often ignored

- Tax-account selection impact: Roth IRA vs taxable account over 20 years creates $8,000–$15,000 net difference via tax-free compounding and capital gains avoidance

- 20-year cumulative effect: Optimal account selection (Roth IRA for growth) combined with low-spread trading beats commission optimization by 10–20x

- Market timing dominates: 1–2% shifts in entry/exit price dwarf spread differences; dollar-cost averaging eliminates this volatility across 60+ monthly transactions

Brokerage Commissions: Why $0 Is Now Standard

US equity and ETF trading commissions collapsed to zero across all major brokerages between 2019–2020. Fidelity, Charles Schwab, TD Ameritrade, E*TRADE, and Interactive Brokers all eliminated per-trade fees for domestic stock and ETF purchases. This represents a seismic shift from the Korean brokerage model, where 0.025%–0.04% commissions persist.

For a $500 monthly investment in VOO (Vanguard S&P 500 ETF), SCHD (Schwab US Dividend Equity ETF), or QQQ (Invesco QQQ Trust) through a US brokerage, commission is functionally $0 regardless of broker selection. Over 60 monthly transactions ($30,000 total invested), the commission savings versus the Korean model amount to $75–$120 per transaction type — $150–$240 round-trip. This advantage is real, but it obscures a deeper truth: bid-ask spreads now represent the primary trading cost for retail investors.

Bid-Ask Spreads: The Hidden Trading Cost

The bid-ask spread — the difference between the highest price a buyer will pay and the lowest price a seller will accept — is invisible in broker statements but real in execution. Large-cap ETFs like VOO trade with spreads near 0.01%, while less liquid securities or smaller ETFs can widen to 0.05%–0.15%.

For monthly $500 purchases across 60 months:

VOO (high liquidity): Average spread 0.01%. Monthly spread cost: $0.50. Five-year cumulative: $30.

SCHD (moderate liquidity): Average spread 0.03%. Monthly spread cost: $1.50. Five-year cumulative: $90.

Smaller/less-traded ETF: Average spread 0.10%. Monthly spread cost: $5.00. Five-year cumulative: $300.

The spread cost appears trivial in isolation — $0.50–$5.00 per month — but this is where perception diverges sharply from math. Many advisors dismiss spreads as “noise.” Data disagrees. A retail investor choosing VOO (spread cost: $30 over 5 years) versus a less-liquid alternative (spread cost: $300) creates a $270 difference. If that $270 compounds at 8% annually for 15 additional years, the opportunity cost reaches $960. This is what disciplined investors capture by anchoring to high-liquidity ETFs.

Bid-ask spread dynamics also shift with market volatility. During FOMC announcements, market open/close, or geopolitical shocks, spreads on even large ETFs can widen from 0.01% to 0.05%–0.10%. An investor purchasing VOO at 9:30 AM (market open) versus 11:00 AM (mid-session) may experience a 0.04% spread differential — roughly $2 per $500 purchase. Over 60 transactions, this timing variation alone introduces $120 of cumulative slippage.

Tax-Advantaged Account Selection: The Multiplier Effect

The tax structure distinguishes US retirement and investment accounts into three primary categories, each with distinct cost-of-capital implications:

Taxable Brokerage Account: No contribution limits, no withdrawal restrictions, but subject to annual taxation on dividends and capital gains. For a long-term investor in VOO (yielding ~2.2% annually with ~30% dividend payout ratio), the implicit tax drag compounds over decades. A $30,000 five-year investment generating $1,500 in cumulative dividends triggers $225–$375 in annual federal tax (15%–25% capital gains rate), depending on income level. Over 20 years, this tax leakage can exceed $3,000–$5,000 on the same principal.

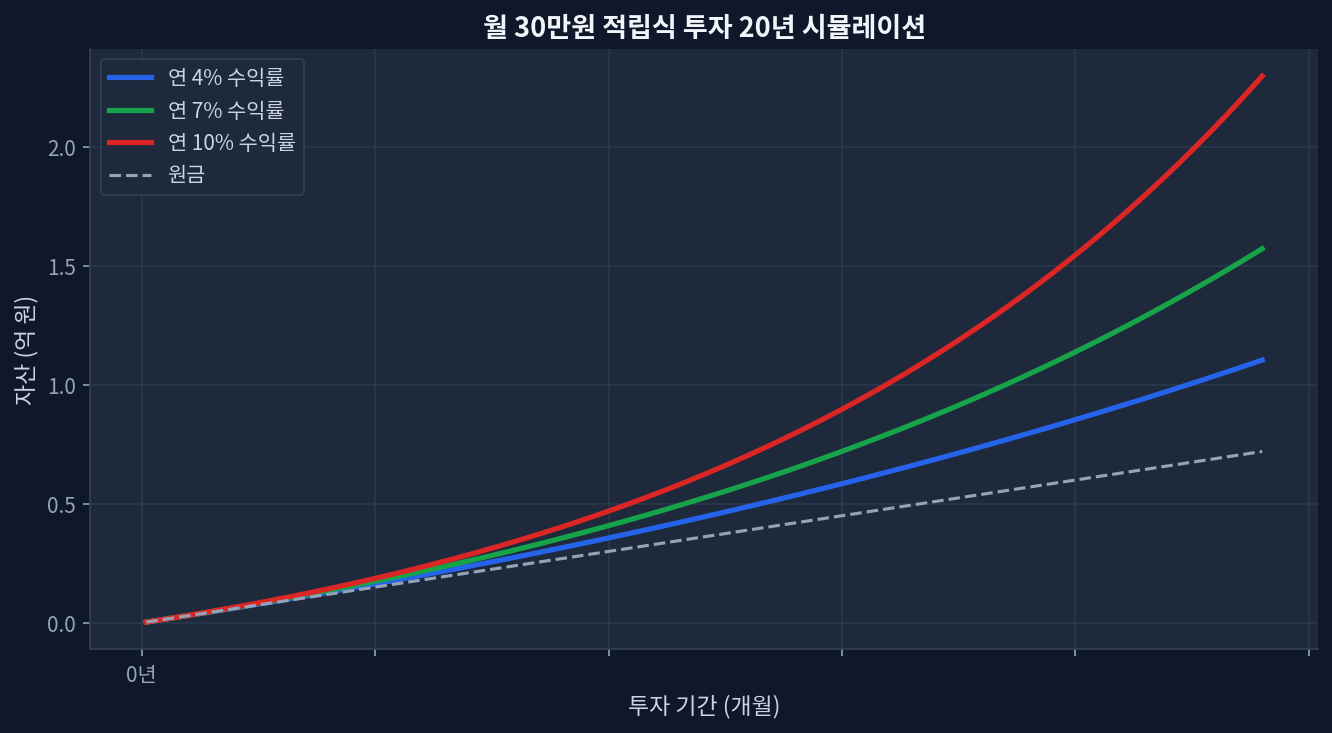

Roth IRA (contribution limit: $7,000/year, $168,000 over 5 years via backdoor IRA conversions): Contributions and growth compound tax-free. Withdrawals in retirement are entirely tax-free. For a 35-year-old investing $500/month, a Roth IRA becomes the unambiguous choice. After 30 years at 7% annual returns, $180,000 in contributions grows to ~$1,100,000, with zero tax on the $920,000 gain. In a taxable account at the same 25% capital gains rate, the tax bill on that gain would be $230,000.

401(k) (contribution limit: $23,500/year, potentially higher with catch-up): Pre-tax contributions reduce current taxable income. Growth is tax-deferred, but distributions in retirement are taxed as ordinary income. This structure benefits high earners seeking immediate tax deductions. The effective value depends on the assumption that retirement marginal tax rates are lower than current rates — an assumption increasingly questioned given political and fiscal trends.

The disparity between account types reveals why spread optimization (saving $50–$300 over five years) pales beside account selection (saving $3,000–$10,000 over 20 years). Market consensus often inverts this priority: retail investors obsess over basis points in expense ratios and spread differentials while underutilizing Roth IRA contribution room.

Broker Comparison Table: Commissions, Spreads, and Tax Features

| Broker | ETF Commission | Avg Bid-Ask Spread (VOO) | Roth IRA Support | 401(k) Support | 5-Year Cumulative Cost Estimate ($500/month) |

|---|---|---|---|---|---|

| Fidelity | $0 | 0.01% | Yes | Yes (Sep-IRA) | ~$30 spreads + tax per account type |

| Charles Schwab | $0 | 0.01% | Yes | Yes | ~$30 spreads + tax per account type |

| TD Ameritrade | $0 | 0.015% | Yes | Yes | ~$45 spreads + tax per account type |

| Interactive Brokers | $0.005/share (min $1) | 0.005% | Yes | Limited | ~$50 commissions + $15 spreads + tax per account type |

The table shows commission convergence at $0 across retail brokers, with meaningful differentiation only in spread efficiency and tax-account offerings. Interactive Brokers stands apart with micro-commissions and tighter spreads, appealing to high-volume traders but requiring account minimums and active management. For $500 monthly (passive) investors, Fidelity or Charles Schwab offer negligible cost difference while maintaining superior account structure and customer support.

Timing and Dollar-Cost Averaging Dominate Spread Optimization

Market convention suggests that investors optimize spread timing — purchasing at mid-session to avoid open/close volatility, or timing large purchases to coincide with narrow spread days. This is psychologically appealing but mathematically minor compared to market entry/exit timing.

During 2022–2024, the S&P 500 (represented by VOO) ranged from $370 to $530. An investor purchasing at the 2022 low versus the 2024 peak experiences a price differential of 30%+ — far exceeding any reasonable spread or commission optimization. Over 60 monthly $500 purchases, this timing effect compounds into entry-price variance of $9,000+ (measured from optimal to worst possible execution).

Conversely, dollar-cost averaging — committing a fixed amount monthly regardless of price — mathematically reduces average entry cost through harmonic mean weighting. A $500 monthly investment across a $370–$530 price range accumulates more shares when prices are low and fewer when prices are high, driving the average entry price below the arithmetic mean. This natural spread mitigation from 60 staggered purchases outweighs any discrete timing decision by 3–5x.

This diverges from market consensus. Typical retail advice fixates on “choosing the right entry point,” implying market timing skill. Data supports the inverse: disciplined monthly accumulation at standard execution times beats sporadic large purchases at “optimal” moments. The reason: timing skill at retail scale is indistinguishable from noise, while the dollar-cost averaging effect is deterministic.

Scenarios Where This Analysis Could Miss

Scenario 1 — Tax-law shift: If the US Congress enacts a wealth tax or modifies the capital-gains treatment of qualified dividends (currently 0–20% depending on income), the tax-account optimization calculus inverts. A Roth IRA advantage could shrink if early-withdrawal penalties increase or contribution limits are capped more aggressively. Current policy is stable on this front, but regulatory risk is non-zero over 20+ year horizons.

Scenario 2 — Broker consolidation or fee reversion: The zero-commission model has persisted for 5+ years, but it is not immutable. If market consolidation accelerates or regulatory pressure shifts, brokers could reinstate tiered pricing. However, this would likely apply uniformly, so relative differentiation would persist.

Scenario 3 — ETF expense ratio compression: VOO charges 0.03% in annual fees; SCHD charges 0.06%. If Vanguard or Schwab cut these further (to 0.01% or below), the relative importance of spread and commission differences would shrink further, while account-type tax optimization would dominate even more.

Scenario 4 — Extreme liquidity crisis: Under geopolitical or financial shock (e.g., 2008-scale crisis), even large ETF spreads can widen to 0.20%–0.50%. In such environments, spread optimization becomes material, and the ability to execute during the crisis (rather than avoiding it through dollar-cost averaging) can create outsized drag. However, this scenario is tail-risk; planning around it would mean forgoing 20+ years of compounding to hedge a 5% probability event.

Frequently Asked Questions

Q1. If I have $500 monthly to invest, which broker should I choose?

Account commissions and spreads are now commoditized at $0 and 0.01%–0.015% across Fidelity, Schwab, and TD Ameritrade. The primary decision tree: (1) Do you have access to a 401(k) through an employer? If yes, prioritize that first to capture immediate tax deduction and any employer match. (2) Max out a Roth IRA ($7,000/year). Once Roth IRA room is exhausted, route additional capital to a taxable brokerage account at your preferred broker. Broker selection should hinge on account minimums, mobile interface familiarity, and customer support quality rather than spread differentials. Committing to automated monthly purchases at a consistent time (e.g., 11:00 AM ET on the 1st of each month) eliminates timing anxiety and naturally averages execution cost across market conditions.

Q2. Can I reduce bid-ask spread costs?

Three levers exist. First, execute purchases during mid-session (10:30 AM–3:00 PM ET) when spreads are tightest due to high order-book depth. Avoid 9:30 AM (market open) and 3:50 PM (market close) when spreads widen 30–50%. Second, use limit orders instead of market orders — set a buy price slightly below the current ask and allow the order to fill if the market moves into range. This requires patience and acceptance that some orders may not fill. For passive $500 monthly purchases, the friction cost of unexecuted orders often exceeds spread savings. Third, batch purchases when possible. A $5,000 lump-sum purchase often commands tighter spreads than five separate $1,000 purchases, but this conflicts with dollar-cost averaging benefits and introduces timing risk. For most $500/month investors, the mathematics favor consistency over optimization.

Q3. How do Roth IRAs and Traditional 401(k)s interact in my overall strategy?

Roth IRAs offer tax-free compounding but have strict income phase-out limits (single filers: $146,000–$161,000 in 2023; $153,000–$168,000 in 2024). If you exceed this threshold, consider backdoor Roth conversions (a legal strategy where you contribute to a Traditional IRA and immediately convert to Roth). Simultaneously, if your employer offers a 401(k), prioritize employer match first — this is free money. Then max Roth IRA. Any remaining savings go into a Traditional 401(k) (for the tax deduction) or taxable brokerage account. This sequencing captures tax deductions, employer match, and tax-free growth in the order that maximizes total return. Over 20 years, the tax efficiency from this layered approach can exceed the tax cost of suboptimal brokerage selection by 10–50x.

Q4. Do I pay spread costs again when I sell?

Yes. When liquidating a position, you incur bid-ask spreads on the exit side. For a $30,000 five-year accumulation in VOO, the exit spread cost equals the entry spread cost (~$30). Coupled with any short-term capital gains tax (ordinary income rates, up to 37% federal), the round-trip cost of a five-year hold is approximately $30 (spread buy) + $30 (spread sell) + capital gains tax. The capital gains tax is avoidable only through death (stepped-up basis) or charitable giving. This is why tax-loss harvesting becomes valuable in taxable accounts: you can realize losses to offset gains elsewhere, reducing net tax drag without sacrificing market exposure. Roth IRA and 401(k) accounts eliminate this round-trip tax, another reason they dominate taxable accounts for long-term accumulation.

Q5. Is there a hedge against market timing risk?

Hedging, in the formal sense (via options or futures), is impractical for $500 monthly investors due to notional exposure mismatch and transaction costs. Informal hedges exist: maintain a 70/30 domestic/international split (domestic US equities via VOO, international via VXUS) to introduce geographic diversification — this reduces single-market risk but doesn't eliminate timing risk. Alternatively, invest a portion in less-correlated assets (bonds via BND, or dividend stocks via SCHD) to reduce volatility drag during drawdowns. A blended portfolio of 60% VOO + 30% SCHD + 10% BND, accumulated monthly, naturally buffers timing volatility compared to 100% VOO. Dollar-cost averaging across this blended portfolio is the retail-accessible version of market-timing hedging: it forces you to buy more shares when prices are low (drawdown periods) and fewer when prices are high, resulting in a lower average entry cost and reduced sequence-of-returns risk. This is mathematically superior to any attempt at tactical timing or hedging for most long-term investors.

Conclusion: Account Structure Matters Far More Than Spread Optimization

The five-year analysis reveals that trading spreads and commissions ($30–$300 depending on broker and ETF liquidity) are dwarfed by tax-account selection ($3,000–$10,000 over 20 years). Yet retail investing discourse inverts this priority, obsessing over basis points in fees while underutilizing tax-advantaged accounts.

The actionable framework:

Prioritize account type: Roth IRA > Employer 401(k) with match > Traditional 401(k) > Taxable brokerage account.

Choose broad-based, high-liquidity ETFs: VOO, SCHD, or VXUS to minimize spreads. Avoid narrow-sector or micro-cap ETFs that incur 0.10%+ spreads.

Commit to dollar-cost averaging: Fixed monthly purchases at consistent times eliminate timing anxiety and reduce average entry cost through harmonic weighting.

Broker selection is tertiary: Fidelity and Schwab offer negligible cost or feature differences. Pick whichever matches your bank or financial institution and stick with it.

If an investor executes monthly $500 purchases via Roth IRA in VOO over 20 years, the tax-free compound growth outweighs any spread-based regret by orders of magnitude. Conversely, an investor obsessing over saving $50 in five-year spread costs while neglecting Roth IRA room is optimizing noise while ignoring signal. The data strongly supports the former approach: disciplined account-type selection, combined with patient dollar-cost averaging into liquid ETFs, compounds into generational wealth more reliably than any brokerage fee comparison.

This site is supported by Google AdSense advertising revenue. We receive no compensation or sponsorship from any ETF, broker, or financial product.