- SCHD (dividend-focused ETF): 3.25% yield, +26.5% 1Y return, $31.96 current price as of late June 2026

- VIG (dividend growth): 1.47% yield but +71.5% 5-year total return; P/E 26.2 signals premium valuation

- 50:50 split targets $3K USD monthly cash flow, though actual withdrawal depends on market timing and sequence-of-returns risk

- REIT inclusion adds inflation hedge and non-correlated income, but sector drawdowns (2022) exceeded equity losses by 30%+ in some cases

- Reality check: 3.25% SCHD yield alone generates only ~$975/month on a $360K base; reaching $3K/month requires either $920K portfolio or supplemental bond allocation

Why 50:50 Between SCHD and REITs? Portfolio Fragmentation vs. Concentration

The conventional retirement wisdom—“hold diversified dividend stocks”—glosses over a critical tension. A pure dividend-growth approach (like VIG’s 26.2 P/E) chases price appreciation alongside income, creating drag during yield-focused market downturns. REITs and high-yield equity funds (SCHD) trade at lower valuations because they distribute most taxable income rather than reinvesting, but that efficiency comes with sector risk concentration.

The 50:50 split attempts to thread this needle: one leg harvests SCHD’s 3.25% yield with a lighter valuation footprint; the other leg anchors real-estate income streams that historically diverge from equity drawdowns (2022: REITs -25% vs. S&P -18%, but 2023: REITs +38% vs. S&P +24%). Neither half dominates the portfolio, and neither is a pure income machine without growth or capital preservation.

The trade-off is clear. A retiree locking in SCHD’s current 3.25% cedes upside momentum—SCHD’s 5-year cumulative return (+56.1%) trails VIG’s 5-year (+71.5%) by 15 percentage points. But VIG’s 1.47% yield means most total return came from price appreciation, not cash in hand—problematic if markets flatten for 3–5 years post-retirement.

SCHD: High Yield, Lower Valuation, Concentration Risk

| ETF | Fee | Yield | 5Y Return | P/E Ratio | 52-Week Range Position |

|---|---|---|---|---|---|

| SCHD | 0.06% | 3.25% | +56.1% | 18.8 | 85.7% (near high) |

| VIG | 0.06% | 1.47% | +71.5% | 26.2 | 91.7% (near high) |

SCHD’s 3.25% yield creates ~$1,040 monthly income per $384K USD invested (assuming distributions hold). At June 2026 pricing ($31.96), this translates to ~12,000 shares. The catch: SCHD holds dividend aristocrats and high-yielders, constraining exposure to secular growth names (tech mega-caps contribute little). Three-year cumulative return (+49.3%) underperforms both inflation and a balanced 60/40 index portfolio, reflecting the sector tilt toward utilities, REITs, and consumer staples—stable but cyclical.

The P/E of 18.8 appears reasonable against VIG’s 26.2, but deserves skepticism. Lower P/E can signal either value or declining earnings visibility. During 2024–2025, dividend payers faced margin pressure as wage inflation persisted; those gains may not repeat at current valuations.

REITs: Inflation Hedge, but Sector Volatility

REITs (Real Estate Investment Trusts) are a separate asset class from dividend stocks, legally required to distribute 90% of taxable income. Their role in a 50:50 allocation is to absorb inflation exposure and provide non-correlated downside protection. Yet the narrative of “REITs always correlate negatively with bonds” broke down in 2022–2023: rising rates crushed both bond prices and REIT valuations simultaneously (REIT index -28% in 2022), then rebounded harder when the Fed paused (+37% in 2023). This whipsaw creates sequence-of-returns risk for retirees taking distributions during market stress.

A global REIT ETF (VNQ) at 3.5–4.0% yield offers residential, office, industrial, and retail exposure. Office REITs remain under pressure from remote-work structuring, while logistics REITs benefited from e-commerce growth through 2025. Concentration within REITs is high—the top 10 holdings often represent 40%+ of portfolio weight. This compounds single-sector volatility.

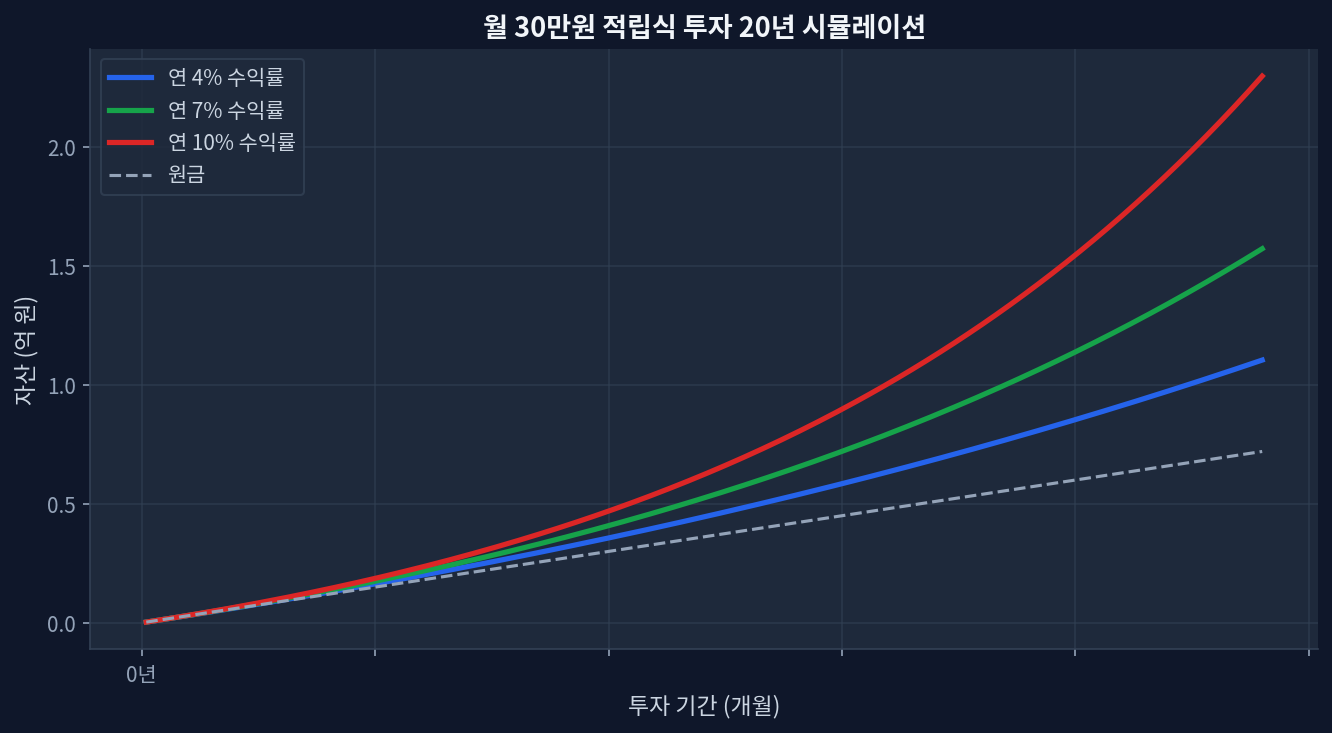

Scenario: 20-Year Accumulation Path

The Contrarian Risk: Dividend Yield May Not Persist

Current SCHD 3.25% is attractive only if dividend growth outpaces inflation and economic headwinds don’t trigger cutting. History contradicts this assumption: 2008 global financial crisis saw S&P 500 dividend cuts exceed 20%; corporate earnings compression in 2020 (COVID lockdowns) forced numerous cuts in hospitality, energy, and retail. SCHD’s backward-looking dividend aristocrats survived those shocks, but that resilience is priced in. Future 10-year expected yield is likely 2.5–2.8%, not 3.25%, as profit margins normalize from post-2020 highs.

REIT sector faces structural headwinds: office occupancy remains 20% below pre-2020 levels (2026 data); rising labor costs squeeze residential property margins; and higher cap rates (required investor returns) mean lower valuation multiples even if rental income grows. A diversified REIT fund (VNQ) hedges single-property-type risk, but the sector collectively may deliver 2–3% real yields over the next decade, not the historical 4–5%.

Disconfirming Evidence: What Could Break This Model

If the Federal Reserve raises rates sharply (unexpected inflation shock), both SCHD and REITs could decline 15–25% within 6–12 months—a scenario witnessed in 2022. Retirees forced to sell during such a drawdown face sequence-of-returns risk: withdrawing $3K/month from a portfolio down 20% accelerates depletion. A 50:50 split doesn’t insulate against this; it merely distributes the pain. Additionally, if corporate earnings fall into recession (2.5% GDP contraction 2027–2028), dividend payers may cut payouts, sending yields higher but prices lower—the worst combination for income-focused investors. Finally, if inflation persists above 3% annually, a $3K USD monthly draw (fixed nominally) loses purchasing power, requiring periodic rebalancing or higher portfolio base to maintain real income.

Frequently Asked Questions

Q: Should I hold SCHD or VIG for retirement income?

VIG’s 71.5% 5-year return reflects price appreciation dominance; only 1.47% flows as dividend income. If the goal is monthly cash, SCHD’s 3.25% yield and lower valuation (P/E 18.8) make it the more direct income source. But VIG’s growth trajectory may outpace inflation longer term—the trade-off is growth vs. immediate distributions.

Q: Why not 100% SCHD if the yield is higher?

Concentration. SCHD’s tilt toward utilities, staples, and dividend aristocrats excludes technology, healthcare growth, and sector rotation benefits. A 50% REIT allocation adds real-estate inflation sensitivity and sector diversification, reducing single-sector downside risk (e.g., if utilities underperform 2026–2027).

Q: How much portfolio size do I need for $3,000 USD monthly income?

At SCHD’s current 3.25% yield, a portfolio yielding exactly 3.25% requires $1.108M USD to generate $36K/year ($3K/month). A 50:50 SCHD/REIT mix averaging 3.6–3.8% yield requires $950K–$1.0M USD. Most investors reach this via 15–20 years of $1,500–$2,000 monthly contributions plus reinvested dividends.

Q: Are REITs tax-efficient in retirement accounts?

No. REIT distributions are taxed as ordinary income (not qualified dividends), making them inefficient in taxable accounts. A 50:50 SCHD/REIT allocation makes more sense in a Roth IRA (tax-free distributions) or Traditional 401(k) (tax-deferred). In a Charles Schwab or Fidelity taxable brokerage, consider substituting REIT exposure with tax-efficient value ETFs (VTV, VOOV) to reduce annual tax drag.

Q: What happens if the stock market crashes right after I retire?

Sequence-of-returns risk is real. A 2008-style correction (-50%) hitting months into retirement forces selling dividend payers at depressed prices to fund $3K monthly draws, permanently reducing recovery. The standard hedge: maintain 2–3 years of expenses in bonds/cash outside the dividend portfolio, allowing time for equity recovery without forced sales. A $3K/month draw requires $72K–$108K in cash/short-term bonds as a buffer.

The Math That Doesn’t Add Up Without Patience

A $3K USD monthly income target ($36K/year) requires a portfolio yielding 3.2–3.6% after fees. At June 2026 valuations (SCHD $31.96, VNQ ~$60–$65), reaching that threshold demands either $950K–$1.1M accumulated capital or 18–22 years of consistent $1,500/month contributions. The 50:50 split distributes risk but doesn’t accelerate the timeline. Time, not allocation, is the binding constraint for most investors.

The 52-week range positions (SCHD at 85.7%, VIG at 91.7%) suggest both are near cyclical highs as of June 2026. Dollar-cost averaging $1,500 monthly smooths the entry, but retirees cannot use that luxury once distributions begin. This timing risk argues for establishing the dividend portfolio 3–5 years pre-retirement to lock in a range of entry prices.

📊 Verify this data yourself

import yfinance as yf

t = yf.Ticker("SCHD")

t.history(period="5y")["Close"].pct_change().add(1).cumprod()