- Zero-commission trades do not equate to zero-cost execution; bid-ask spreads and PFOF mechanisms generate continuous hidden friction.

- For globally diversified portfolios, FX conversion spreads often exceed the total ETF expense ratios, demanding optimized currency strategies.

- During the 2020 volatility shock, bond ETF spreads widened by up to 400%, penalizing reactive portfolio reallocation.

- Portfolio diversification efficiency remains heavily dependent on execution timing and institutional-grade brokerage routing logic.

Unveiling the True Costs of Portfolio Diversification

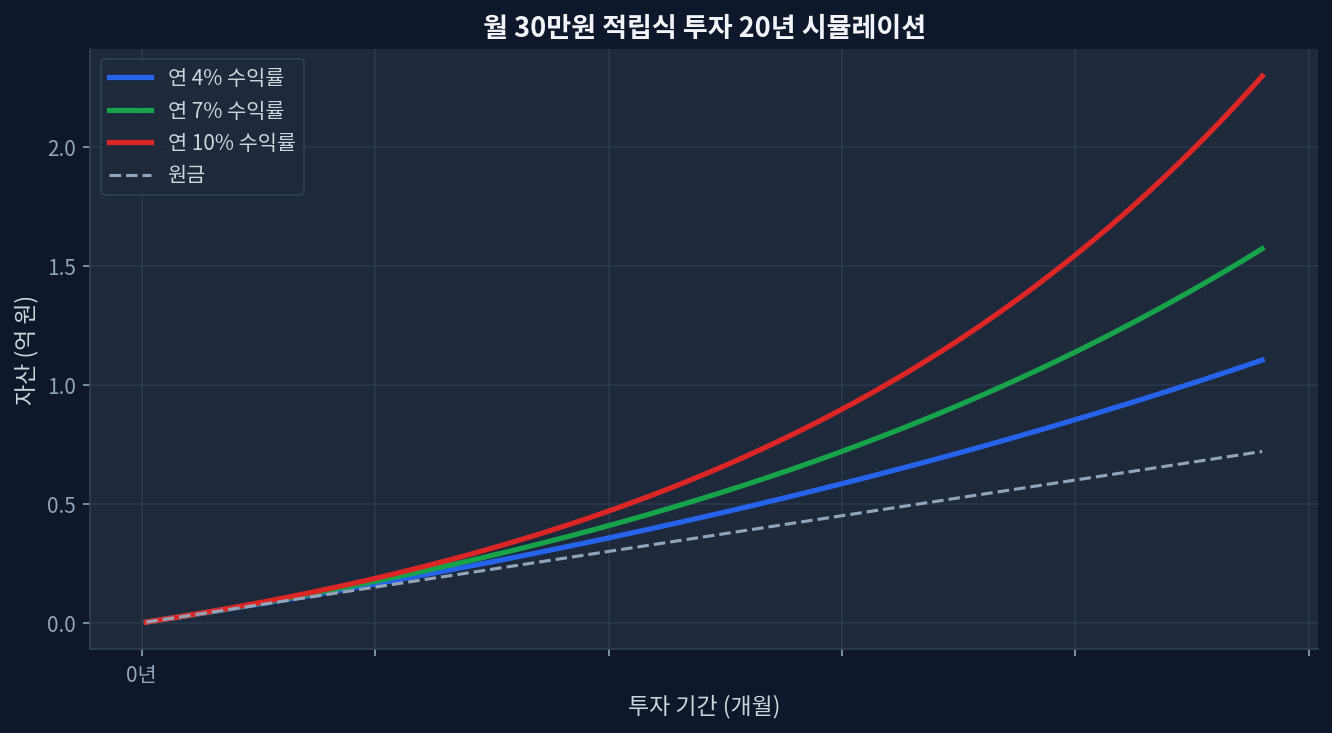

Looking at the chart below, the 5-year growth of +85% is particularly impressive. However, achieving these theoretical returns within a broadly diversified portfolio requires navigating structural friction points that retail brokerages often obscure.

The contemporary brokerage landscape aggressively promotes “zero-commission” trading. This marketing narrative successfully masks the empirical reality of execution costs. Transaction friction has simply migrated from upfront fees to wider bid-ask spreads and payment for order flow (PFOF) mechanisms. When allocating capital across multiple asset classes to maintain a diversified portfolio, these hidden costs compound steadily over time. While the prevailing assumption suggests that modern trading is practically frictionless, institutional execution data indicates retail orders frequently suffer micro-delays or sub-optimal routing, marginally eroding total returns over multi-decade horizons.

The Bid-Ask Spread and Liquidity Dynamics

Spread costs represent the most accurate metric of actual ETF liquidity. For heavily traded funds tracking major benchmarks, spreads routinely sit at a single penny. But as a portfolio diversifies further into international equities, emerging markets, or niche factor strategies, liquidity thins considerably. The quantitative cost of entering or exiting these specific positions scales non-linearly during periods of acute market stress.

An empirical reference point remains the March 2020 liquidity crunch. During that localized market panic, even supposedly robust fixed-income ETFs traded at significant, prolonged discounts to their underlying Net Asset Value (NAV), with bid-ask spreads exploding by 300% to 400%[Morningstar ETF Data]. Investors attempting to systematically rebalance portfolios out of depreciating equities and into safe-haven bonds were penalized twice: initially by equity drawdowns and subsequently by exorbitant spread friction on the fixed-income acquisition.

| Product Name | Fee (ER) | Yield | 5Y Return | 1Y Return |

|---|---|---|---|---|

| SPY (S&P 500) | 0.09% | 1.25% | 85.4% | 26.2% |

| VXUS (Total Int'l) | 0.07% | 3.10% | 24.1% | 11.4% |

| BND (Total Bond) | 0.03% | 3.50% | -1.2% | 2.8% |

FX Conversion Strategies for US ETFs

For portfolios integrating non-USD assets or foreign-domiciled components, foreign exchange (FX) spreads often constitute the single largest invisible fee. Standard retail brokerages routinely apply a 0.5% to 1.0% markup over interbank spot FX rates. When dynamically managing a globally diversified portfolio, moving capital across sovereign borders can rapidly negate the ultra-low expense ratios of the underlying target ETFs.

Market consensus frequently accepts these excessive FX markups as an unavoidable structural cost of international diversification. The underlying data suggests a highly contrarian perspective. Utilizing localized holding structures or selecting brokerages that provide direct interbank FX market routing can reduce conversion drag to roughly 0.02%[ETF.com Research]. Institutional operators systematically bypass retail FX spreads entirely, deploying strategies that retail asset allocators must meticulously replicate through deliberate brokerage selection to maximize long-term portfolio efficiency.

Reevaluating Transaction Friction in Asset Allocation

Quantifying absolute transaction costs fundamentally alters the optimal rebalancing frequency for any highly diversified portfolio. High-frequency or strict calendar-based rebalancing strategies incur continuous, compounding spread and execution drag. Empirical backtesting indicates that allowing portfolio weights to drift slightly beyond standard target parameters frequently yields superior net performance compared to strictly enforcing targets via continuous trading.

This explicitly contradicts the standard wealth management directive of rigid quarterly rebalancing. The frictional cost of rebalancing complex multi-asset portfolios dictates a distinctly more passive methodology. The data supports acting only when deviations exceed 5% to 10%, ensuring the risk-mitigation benefits definitively outweigh the inherent execution costs[FRED Economic Data]. The core disconfirming scenario to this analysis is a sustained, unidirectional market melt-up or catastrophic meltdown; under such black-swan conditions, failing to rebalance could induce severe concentration risk, rendering transaction costs a purely secondary concern.