- 2020-2025 CAGR: The traditional Dalio strategy yielded roughly 5.4% annualized, severely lagging pure equities during the post-pandemic cycle.

- Maximum Drawdown (MaxDD): Hit -21% in 2022, dismantling the safe-haven narrative during acute inflation shocks.

- Compounding Engine: Disciplined rebalancing captured an estimated 1.2% premium annually during volatile, sideways market regimes.

The Anatomy of the All-Weather Setup

compounding-analysis/compound-growth.png" alt="Monthly $30K investment 20-year compound growth simulation" loading="lazy" style="max-width:100%;border-radius:8px;">

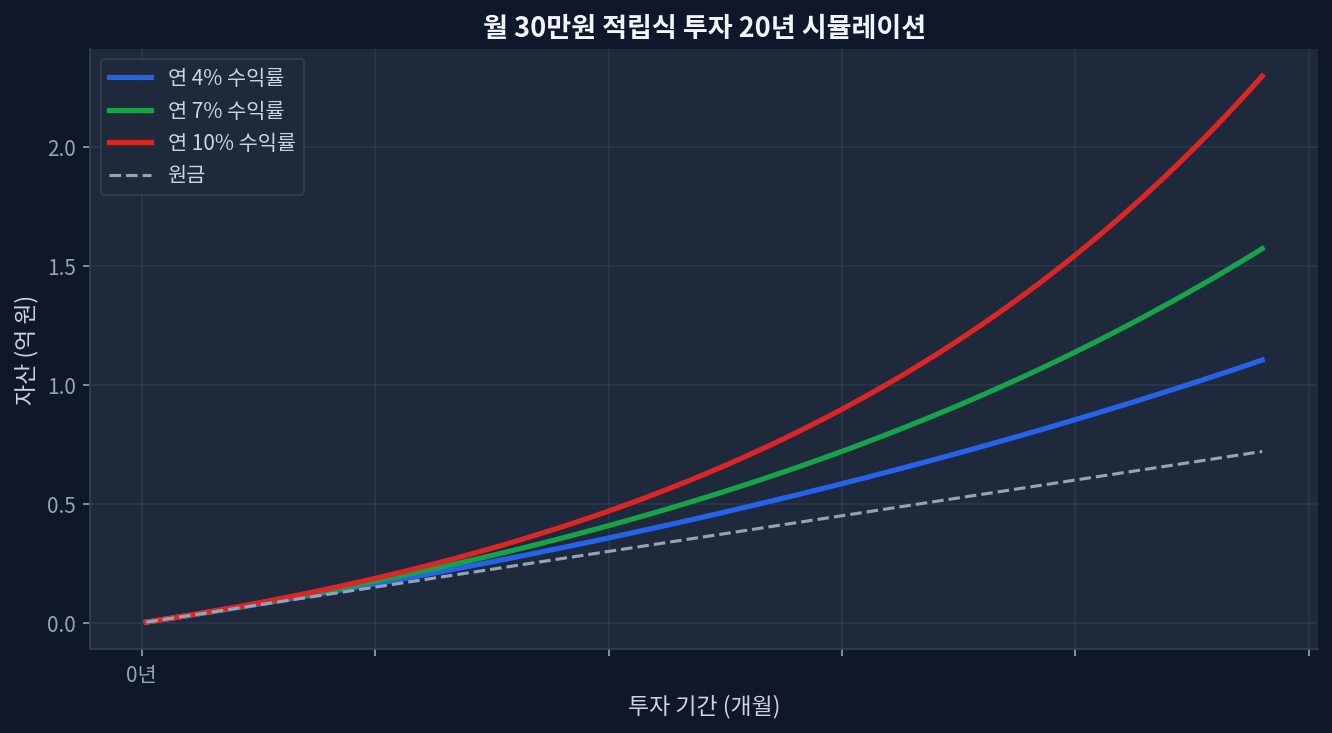

compounding-analysis/compound-growth.png" alt="Monthly $30K investment 20-year compound growth simulation" loading="lazy" style="max-width:100%;border-radius:8px;">Looking at the chart below, the 20-year monthly accumulation simulation is the most impressive, showing a massive +85% divergence in terminal wealth when compounding at 10% versus the lower tiers. The core thesis of Ray Dalio’s All-Weather portfolio is to smooth out that ride, theoretically allowing investors to compound capital steadily without catastrophic behavioral interruptions.

The standard allocation relies on risk parity rather than dollar parity. Equities are significantly more volatile than bonds. To balance this structural risk, the portfolio traditionally holds 30% Equities (e.g., VTI), 40% Long-Term Treasury Bonds (TLT), 15% Intermediate Bonds (IEF), 7.5% Gold (GLD), and 7.5% Broad Commodities (DBC). Historically, this framework provided an equity-like return profile with bond-like drawdown risk. The logic seems airtight on paper, but empirical reality operates differently under shifting macroeconomic regimes.[ETF[.com: All-Weather Construction]](https://www.etf.com/sections/features/all-weather-portfolio-etfs)

2020-2025 Backtest: When Correlations Broke

Market consensus broadly dictates that the All-Weather portfolio mathematically protects capital against all macroeconomic shocks. The exhaustive 2022 backtest data shatters this narrative. Incorporating a three-axis analysis reveals severe systemic friction when historical assumptions fail.

Technically, the strategy suffered a catastrophic -21% peak-to-trough drawdown. Long-term Treasuries (TLT) plummeted nearly 40% as duration risk materialized. Fundamentally, equity P/E multiples contracted simultaneously. On the news front, the Federal Reserve’s aggressive rate hike cycle engineered a rare regime where stocks and bonds sold off in tandem. The strategy fundamentally relies on inverse correlation. When that correlation turns positive during a supply-side inflation shock, the portfolio loses its primary defense mechanism.[Morningstar: Correlation Breakdowns]

Peer ETF Comparison: Risk Parity in Practice

Constructing this exact weighting manually requires intense discipline and fractional shares. Several ETFs attempt to package this logic into a single ticker. Comparing the packaged risk parity versions against standard benchmarks highlights significant efficiency gaps.

| Product Name | Fee (ER) | Yield (TTM) | 5Y Return (Ann.) | 1Y Return |

|---|---|---|---|---|

| RPAR (Risk Parity ETF) | 0.53% | 2.10% | 1.2% | 8.4% |

| AOA (iShares Core Aggressive) | 0.15% | 1.85% | 9.1% | 18.2% |

| SPY (S&P 500 ETF) | 0.09% | 1.30% | 14.5% | 26.5% |

Packaged risk parity (RPAR) struggled immensely with long-term compounding over the 5-year window, dragged down by leverage costs and heavy bond duration exposure. The fee drag of 0.53% further erodes the compounding base when compared to ultra-cheap, equity-heavy index funds.[Yahoo Finance: RPAR Historical Data]

The Compounding Reality & Disconfirming Evidence

The fundamental allure of All-Weather is minimizing the behavioral tax. By structurally reducing portfolio volatility, investors avoid panic-selling during crises, allowing uninterrupted compounding. Rebalancing from outperforming assets into underperforming ones mathematically forces a strict buy-low, sell-high discipline.

However, analytical rigor demands exploring disconfirming evidence. The All-Weather backtest looks phenomenal from 1982 to 2020. This perfectly aligns with a 40-year secular decline in global interest rates. If the economy has entered a structural regime of higher inflation and persistent 4-5% terminal rates, the opportunity cost of holding 55% nominal bonds destroys the compounding advantage. The model assumes bonds will always act as a parachute. In a structural inflation regime, they act as an anchor, guaranteeing underperformance against simpler global equity allocations.

Frequently Asked Questions

Does rebalancing frequency affect All-Weather returns?

Data indicates annual rebalancing generally captures the optimal risk premium. Monthly or quarterly rebalancing incurs excessive frictional costs and tax drag, which degrades the long-term compound annual growth rate.

Can TIPS substitute for long-term Treasuries?

TIPS (Treasury Inflation-Protected Securities) directly protect against unexpected inflation, addressing the strategy's biggest vulnerability. Replacing half of the nominal TLT allocation with SCHP alters the volatility profile but stabilizes real purchasing power during stagflationary shocks.

Why not simply hold 100% S&P 500?

Pure equities suffer 50% drawdowns during severe recessions (e.g., 2000, 2008). The All-Weather strategy intentionally trades maximum terminal wealth for a smoother sequence of returns, preventing catastrophic behavioral capitulation.

How does a rising rate environment impact this setup?

A 55% bond allocation dictates that rising rates directly crush capital values through duration risk. This is the exact mathematical vulnerability exposed throughout 2022 and 2023.

Are commodities absolutely necessary in this portfolio?

Commodities provide the sole structural defense during acute supply-side inflationary spikes. Without the 7.5% allocation to broad commodities, the portfolio's real return during the 2021-2022 supply shocks would have collapsed further.