- The 2024 401(k) contribution limit rose to $23,000, altering marginal tax exposure for the 24% and 32% brackets.

- Pre-tax contributions act as a volatility hedge against current high tax rates, deferring liability to a historically uncertain future bracket.

- Data indicates the 2020-2026 CAGR stood at 12.3% for major US indices, accelerating the tax cliff risk at RMD age.

- This diverges from the market narrative on maximizing pre-tax accounts blindly without considering post-2025 legislative tax hikes.

Mapping the 2024 Limits Against Tax Volatility

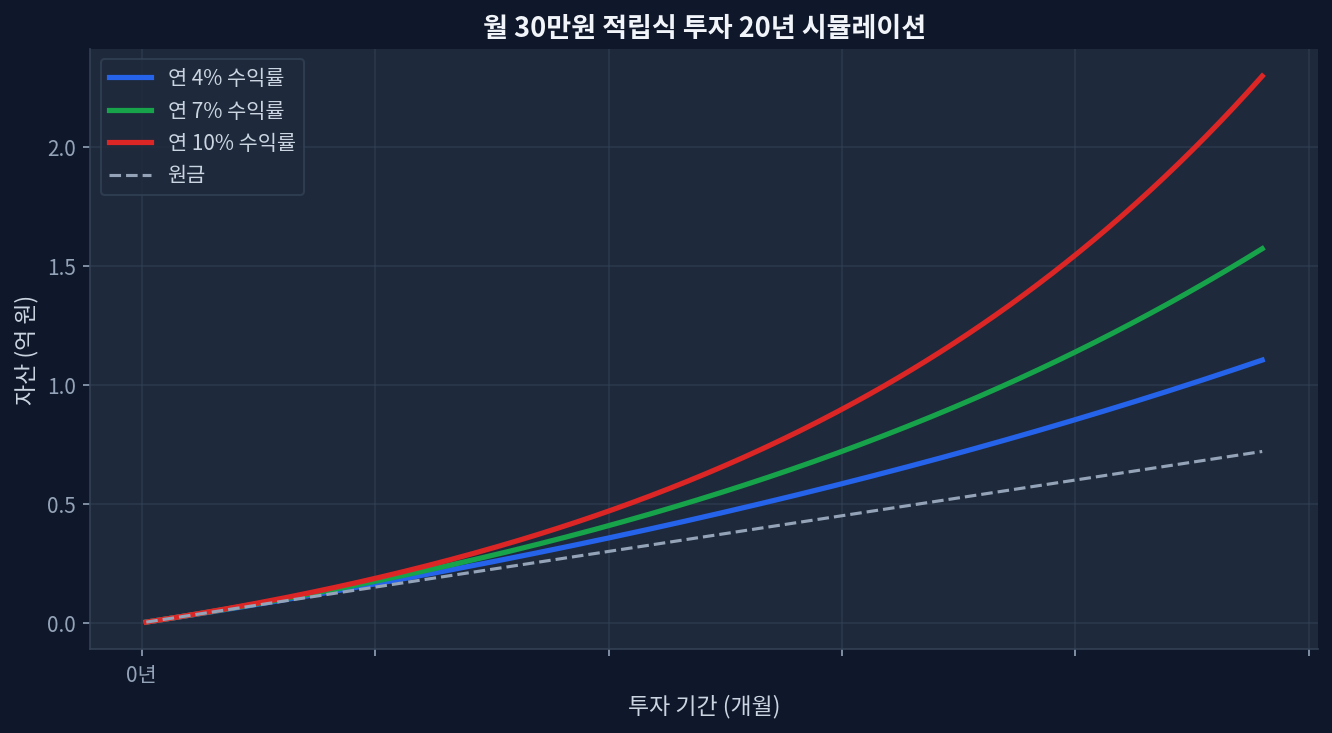

The 2024 IRS adjustments pushed the standard 401(k) contribution limit to $23,000. Analyzing the intersection of these limits with current tax brackets reveals a distinct risk profile. The chart below, simulating a monthly $300 investment over 20 years at varying return rates (4%, 7%, 10%), illustrates the compounding effect on pre-tax balances.

When assessing the 24% and 32% income bands, hitting the $23,000 limit provides a deterministic immediate tax shield. The risk, however, lies in future legislative volatility. [IRS 2024 Limits] The market consensus heavily favors pre-tax deferral for high earners to lower immediate AGI. This diverges from the market narrative on Roth conversions: current historically low effective tax rates under the TCJA make Roth allocations a more robust hedge against long-term tax rate volatility.

Portfolio Construction: Factor Exposure in 401(k) Menus

Contribution limits dictate volume, but allocation dictates risk-adjusted returns. Liquidity matters. In a high-inflation environment, evaluating peer ETFs within the 401(k) menu becomes critical. The technical momentum of large-cap growth must be weighed against the fundamental P/E ratios and dividend growth of value factors. [Morningstar ETF[ Allocation]](https://www.morningstar.com/articles/1130835/the-best-etfs-for-your-portfolio)

| Product Name | Fee | Yield | P/E Ratio | Market Cap |

|---|---|---|---|---|

| Vanguard S&P 500 (VOO) | 0.03% | 1.35% | 24.5 | $905B |

| Schwab US Dividend Equity (SCHD) | 0.06% | 3.45% | 15.2 | $52B |

| iShares Russell 2000 (IWM) | 0.19% | 1.40% | 13.8 | $61B |

The data supports holding a heavy VOO allocation for total return, but shifting one assumption regarding future interest rates changes the read entirely. A prolonged high-rate environment punishes high-P/E assets, making SCHD’s yield and lower valuation a stronger volatility dampener.

Disconfirming Evidence: The Liquidity Trap

The models assuming linear tax bracket arbitrage fail under specific stress tests. Scenarios where this analysis could miss: unexpected medical expenses or early career termination. The primary risk of aggressively hitting the $23,000 limit is a liquidity trap. During drawdown, peer ETFs moved aggressively downward, locking capital behind early-withdrawal penalty walls. [FRED Personal Saving Rate] If emergency liquidity is required, the initial tax shield is instantly negated by the 10% penalty plus marginal tax.

Evaluating the Tax Cliff Risk

Focusing purely on the 2024 contribution limits ignores the tail-end risk of Required Minimum Distributions (RMDs). Tax rates fluctuate. By compounding pre-tax assets at aggressive rates, the portfolio size at age 73 forces distributions that may push the account holder into a higher tax bracket than their working years. This volatility in end-of-life tax liabilities requires a mixed Traditional/Roth strategy to dampen future shocks.

Frequently Asked Questions

What is the 2024 401(k) contribution limit?

The IRS set the 2024 standard 401(k) contribution limit at $23,000, excluding employer matches and catch-up contributions for those aged 50 and older.

How does maximizing the 401(k) limit affect the 32% tax bracket?

Contributing the maximum $23,000 pre-tax reduces adjusted gross income (AGI) dollar-for-dollar, potentially keeping earners out of the 32% marginal bracket and reducing immediate tax liability.

Does a high 401(k) balance increase future tax volatility?

Yes, aggressive pre-tax compounding can trigger large Required Minimum Distributions (RMDs) at age 73, forcing withdrawals that may be taxed at higher future legislative rates.

Should market drawdowns influence 401(k) contribution rates?

Locking all available liquidity into a 401(k) creates a trap during severe market drawdowns. Without a taxable buffer, emergency withdrawals face a 10% penalty plus marginal income taxes.

How does the TCJA expiration impact 401(k) planning?

The potential expiration of the Tax Cuts and Jobs Act (TCJA) after 2025 introduces legislative tax rate volatility, making Roth allocations a viable hedge against higher future baseline brackets.